- More

- Download

Argentine Peso Crash During the World Cup? How to Quickly Convert High-Inflation Currency to Stable USD Using a Digital Wallet

Image Source: pexels

You may have already noticed the sharp drop in the Argentine peso, with asset values rapidly shrinking in a high-inflation environment. According to the latest data, Argentina's inflation rate has risen from 31.50% to 32.40%. Under such economic pressure, many people choose to use digital wallets to convert local currency to USD, in order to preserve asset value. Digital wallets are not only easy to operate but also provide security for your funds.

| Time | Inflation Rate (%) |

|---|---|

| January 2026 | 32.40 |

| Before January 2026 | 31.50 |

Key Takeaways

- The Argentine peso has depreciated severely, with an inflation rate as high as 211%. Using a digital wallet allows you to quickly convert pesos to USD and protect asset value.

- Digital wallets are convenient to operate, with fast transaction speeds—usually completing conversions in just a few minutes, far quicker than traditional bank processing times.

- Choosing a compliant digital wallet platform is crucial. Ensure the platform is registered with the National Securities Commission and complies with relevant regulations to safeguard your funds.

- During the conversion process, pay attention to exchange rate fluctuations and fees, and select the right timing for transactions to reduce the risk of asset depreciation.

- Regularly check account security, properly store transaction receipts, guard against fraud and fund losses, and ensure asset safety.

Background on the Argentine Peso Crash

Image Source: pexels

High Inflation and Currency Depreciation

You can see that the Argentine peso crash has become a global economic phenomenon of concern. Argentina's inflation rate is far higher than that of other South American countries, reaching 211% in 2023. This extreme inflation directly leads to currency depreciation. After the economic crisis in 2001, Argentina experienced a brief recovery, but policy mistakes and rising debt caused the economy to deteriorate again. After the Milei government took office, it implemented deep austerity policies, cutting federal spending, freezing wages and pensions, and relying on IMF loans to stabilize the currency. Investor confidence declined, leading to a sharp depreciation of the peso.

| Event/Policy | Description |

|---|---|

| Currency Depreciation | The Milei government initially devalued the peso by nearly 55%. |

| Austerity Policy | Implemented deep austerity plans, cutting federal spending and freezing wages and pensions. |

| External Support | Relied on loans from the International Monetary Fund to stabilize the currency. |

| Decline in Investor Confidence | After losses in provincial elections in Buenos Aires, investors began selling stocks and pesos. |

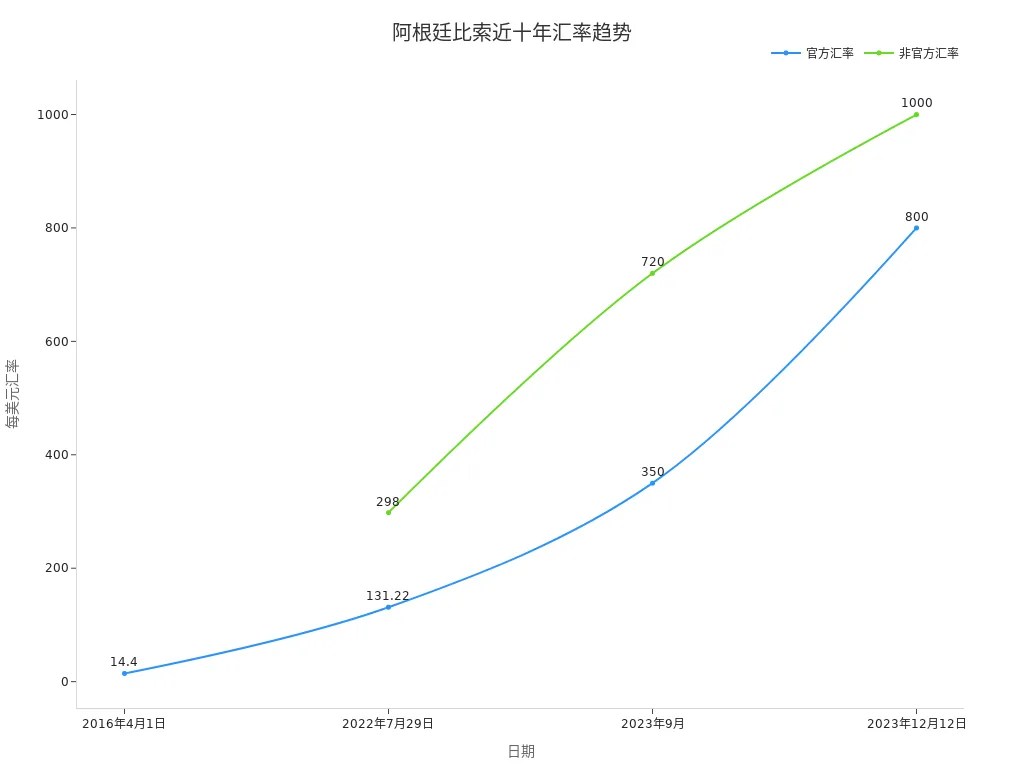

You can intuitively understand the trend of the Argentine peso crash through historical exchange rate data:

| Date | Official Rate (per USD) | Unofficial Rate (per USD) |

|---|---|---|

| April 1, 2016 | 14.4 | N/A |

| July 29, 2022 | 131.22 | 298 |

| September 2023 | 350 | 720 |

| December 12, 2023 | 800 | 1000 |

You will notice that the gap between the official and unofficial exchange rates continues to widen, reflecting market concerns about the Argentine peso crash.

Economic Pressure and Demand for Asset Preservation

When living in Argentina, you may feel the pressure of declining income, rising household debt, and a poverty rate exceeding 50%. High inflation causes the peso's purchasing power to shrink continuously, making asset preservation a real need for everyone. Many Argentines choose USD, cryptocurrencies, or durable goods as hedging tools. Data shows that over 50% of residents buy cryptocurrencies to combat inflation, 27% purchase cryptocurrencies regularly, 46% want to avoid government control, and 60% trust cryptocurrencies.

| Statistic | Percentage |

|---|---|

| Argentines who regularly buy cryptocurrencies | 27% |

| Argentines who trust cryptocurrencies | 60% |

| Argentines who buy cryptocurrencies to avoid government control | 46% |

| Argentines who buy cryptocurrencies as an inflation hedge | Over 50% |

You can hedge the risks brought by the Argentine peso crash in the following ways:

- Hold USD assets, which is especially common in high-inflation countries.

- Wealthy individuals deposit funds in U.S. banks or hold shares in U.S. companies.

- Ordinary residents usually hold USD cash.

- Many people choose durable goods such as houses, gold, or rice as stores of wealth.

- The Argentine government is preparing to relax restrictions on USD cash transactions to promote economic remonetization.

You need to pay attention to asset preservation channels and reasonably choose tools such as digital wallets to effectively cope with the challenges posed by the Argentine peso crash and high inflation.

Advantages of Digital Wallets

Image Source: pexels

Fast Conversion

In a high-inflation environment, the timeliness of asset preservation is crucial. Digital wallets provide you with an almost real-time currency conversion experience. Compared with traditional banks, digital wallets have significantly faster transaction speeds. You can refer to the table below to intuitively understand the processing times of different payment methods:

| Payment Method | Transaction Time |

|---|---|

| Bank wire transfer | 1 to 5 business days |

| Digital wallet (e.g., PayPal) | A few minutes to a few hours |

When you use a digital wallet, you can usually complete the conversion from pesos to USD in just a few minutes. Bank wire transfers may require waiting several days, easily missing the best exchange rate timing. The efficient processing capability of digital wallets helps you lock in asset value in a timely manner during sharp exchange rate fluctuations.

Convenient Operation

Digital wallets are not only fast but also extremely convenient to operate. You can integrate multiple bank accounts within one app without frequently switching platforms. Daily asset management becomes simple and efficient. The table below shows the main differences in user experience between digital wallets and traditional banks:

| Advantage | Digital Wallet (e.g., MODO) | Traditional Bank |

|---|---|---|

| Transaction Speed | Real-time payments, quick completion | Longer processing time |

| Multi-Account Integration | Can integrate multiple bank accounts | Need to manage each account separately |

| Promotions and Offers | Cashback, discounts, flexible response to inflation | Fewer promotional activities |

| User Adaptability | High usage rate, meets efficiency needs | Lower user usage rate |

| Economic Environment Adaptation | Quick response to economic changes | Slower reaction |

During the conversion process, you can check exchange rates at any time, manage fund flows, and enjoy promotions and cashback activities provided by the platform. These advantages allow you to more flexibly address asset management challenges in a high-inflation environment.

Asset Security

When choosing a digital wallet, asset security is one of the most important considerations. Mainstream digital wallets adopt multiple security measures to protect your funds. Common security features include:

| Security Feature | Description |

|---|---|

| Transaction Monitoring | Real-time monitoring of transactions, immediate notification to users upon detecting anomalies |

| Biometric Authentication | Supports fingerprint, facial recognition, etc., for login and transaction confirmation |

| Secure Communication Protocols | Uses HTTPS and other encryption protocols to protect data transmission security |

| Multi-Factor Authentication | Requires PIN, fingerprint, and other multi-verification to enhance account security |

| Data Encryption | Sensitive information is encrypted and stored to prevent unauthorized access |

| Tokenization | Replaces real card numbers with unique tokens to protect account information |

| Regular Security Audits | Regular security audits by independent experts to promptly identify and fix potential vulnerabilities |

When using a digital wallet, you can effectively prevent account theft risks through biometric and multi-factor authentication. Real-time transaction monitoring and secure communication protocols further enhance the level of fund security. You don't need to worry about unauthorized access or information leakage of assets during the conversion process.

Preparation Before Conversion

Before you start using a digital wallet to convert pesos and USD, you must complete a series of basic preparations. These steps not only ensure your account security but also make subsequent operations smooth.

Registration and Real-Name Verification

You need to first register an account on a legitimate digital wallet platform. According to the latest Argentine regulations, all Virtual Asset Service Providers (VASPs) must register with the National Securities Commission (CNV) and strictly comply with anti-money laundering and counter-terrorism financing requirements. The platform will require you to complete real-name verification, including uploading identity documents, performing facial recognition, etc. You also need to go through the Know Your Customer (KYC) process, where the platform assesses your identity and risks and continuously monitors suspicious activities. The table below summarizes the main compliance requirements:

| Requirement Type | Detailed Information |

|---|---|

| Registration Requirement | VASPs must register with the National Securities Commission (CNV) |

| Compliance Requirement | Comply with anti-money laundering/counter-terrorism financing standards, implement customer due diligence and transaction monitoring |

| Deadline | Individuals: July 1, 2025; Argentine legal entities: August 1, 2025; Foreign legal entities: September 1, 2025 |

Tip: You should prioritize platforms that are registered and compliant to avoid asset risks due to platform violations.

Binding Bank Card

After completing real-name verification, you need to bind a valid bank card. Mainstream digital wallets in Argentina generally support credit cards, debit cards, and prepaid cash cards. Visa holds more than 60% market share in Argentina, so using Visa credit or debit cards usually provides higher compatibility and transaction success rates. Some platforms also support direct carrier billing, but mainstream conversion operations still rely primarily on bank cards. When binding a bank card, you should ensure that the card information is true and valid to avoid recharge or withdrawal failures due to incorrect information.

- Supported bank card types include:

- Credit cards

- Debit cards

- Prepaid cash cards

After completing the above preparations, you can smoothly proceed to the recharge and conversion process. Choosing compliant platforms and standardized operations is the key to ensuring fund security and asset preservation.

Conversion Process

When preserving assets in a high-inflation environment, digital wallets provide you with efficient and secure conversion channels. The following takes BiyaPay as an example to introduce in detail the standard process of peso recharge, USD conversion, and withdrawal & storage, combined with industry common standards, to help you avoid common operational mistakes.

Recharging Pesos

You first need to recharge Argentine pesos to the digital wallet. BiyaPay supports multiple recharge methods, including local bank transfers, international remittances, and some digital currency recharges. You should choose the optimal channel based on your fund sources.

The recharge process usually includes the following steps:

- Log in to your BiyaPay account and go to the “Recharge” page.

- Select “Argentine Peso” as the recharge currency; the system will automatically display supported recharge methods and real-time exchange rates.

- Fill in the recharge amount, confirm the receiving account information, and submit the recharge application.

- Follow the page instructions to complete the bank transfer or digital currency transfer, and upload the transfer receipt.

- Wait for the platform to review and credit the funds, usually completed within 1-2 hours.

Tip: When recharging, ensure that the bank account information is accurate to avoid recharge failures or delays due to errors. Some banks may set limits on international remittances, so it is recommended to consult bank customer service in advance.

Converting to USD

After completing the peso recharge, you can directly convert pesos to USD within BiyaPay. The platform supports real-time conversion between fiat and digital currencies, with transparent exchange rates and convenient operations.

Before confirming the exchange, you can also use the BiyaPay official website and its exchange-rate comparison tool to check the current spread, estimated proceeds, and conversion cost first. When dealing with a high-inflation currency, the real issue is not only whether conversion is possible, but whether the rate, route, and fees are transparent enough to make a timely decision. BiyaPay is positioned as a multi-asset trading wallet covering cross-border payments, fund management, and multi-currency conversion, and it also operates with relevant financial registrations and compliance credentials in jurisdictions such as the United States and New Zealand, which helps users assess platform reliability more cautiously when moving funds.

The conversion process is as follows:

- On the BiyaPay homepage, select the “Currency Conversion” function.

- Set “Argentine Peso” to convert to “USD”, enter the conversion amount, and the system will automatically display the current exchange rate and estimated received amount.

- After verifying the information is correct, confirm the conversion; the platform will complete the matching and deduct the corresponding fees within seconds.

- After successful conversion, you can view the USD balance in real time on the “Assets” page.

During the conversion process, you should pay attention to exchange rate fluctuations and choose periods with better rates to effectively reduce conversion costs. BiyaPay supports USDT conversion to USD or HKD. If you hold digital currency assets, you can also flexibly switch to USD assets to achieve diversified asset allocation.

Note: Some platforms may temporarily adjust exchange rates or limits during high-volatility periods. It is recommended to check the platform announcements in advance and reasonably plan your conversion schedule.

Withdrawal and Storage

After completing the USD conversion, you can choose to withdraw to a licensed Hong Kong bank account, an international bank card, or directly store in the BiyaPay digital wallet. The withdrawal and storage stages require attention to fees, limits, and arrival times.

Withdrawal operation process:

- Go to the BiyaPay “Withdrawal” page and select “USD” as the withdrawal currency.

- Bind and verify the receiving bank account; Hong Kong licensed bank accounts are recommended first to ensure compliance and security.

- Enter the withdrawal amount; the system will automatically display the fees and estimated arrival time.

- Submit the withdrawal application; the platform will complete review and transfer within 1-2 business days.

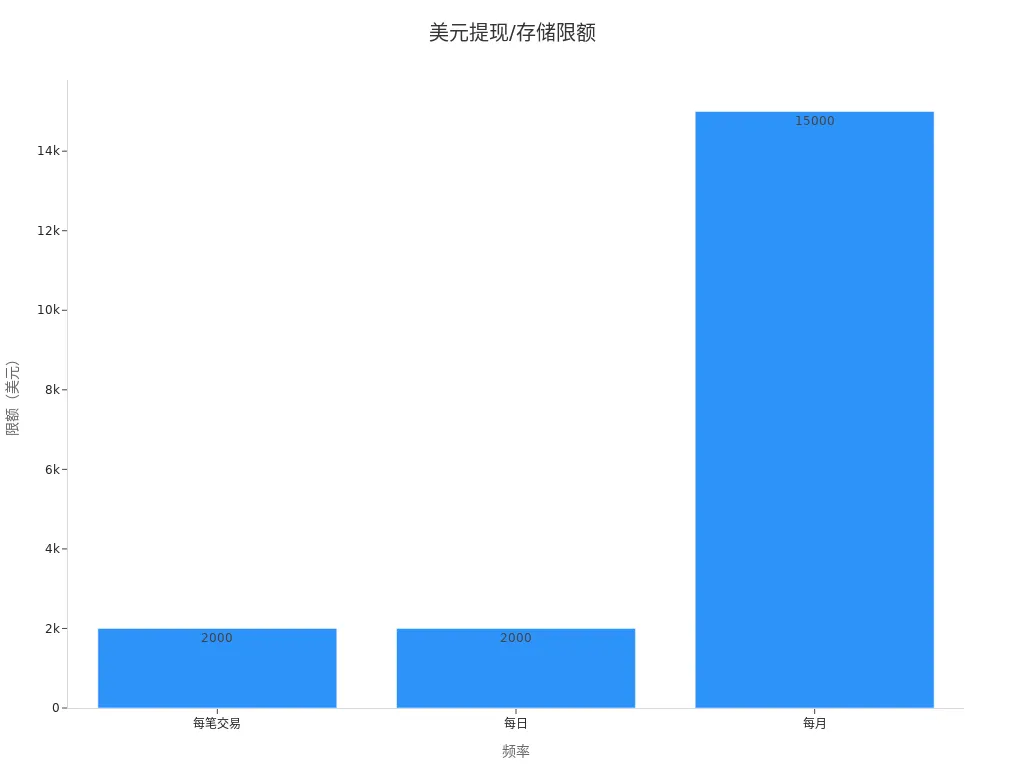

Withdrawal and storage limits & fees overview:

| Currency | Minimum Fee |

|---|---|

| USD | 0.50 USD |

| Frequency | Maximum per Transaction | Maximum Daily | Maximum Monthly |

|---|---|---|---|

| Withdrawal/Storage | 2,000.00 USD | 2,000.00 USD | 15,000.00 USD |

When withdrawing, you should reasonably plan the amount to avoid operation failures due to exceeding limits. For large fund transfers, you can operate in batches or apply to the platform in advance to increase limits.

Tip: When storing USD in the BiyaPay wallet, the platform uses multiple encryption and risk control measures to ensure fund security. It is recommended to regularly check account balances and adjust asset allocation in a timely manner.

Common Questions and Error Code Explanations:

During actual operations, you may encounter the following common issues. It is recommended to understand them in advance and handle them properly:

| Error Code | Description |

|---|---|

| Cancel Transaction Error | The request attempted to cancel a wallet transaction, but the transaction was not found. Request rejected. Corrective action: Provide a valid transaction ID. |

| Complete Transaction Error | The request attempted to complete a wallet transaction, but the transaction was not found. Request rejected. Corrective action: Provide a valid transaction ID. |

| Amount Exceeds Target Wallet Limit Error | The request attempted an operation, but the amount exceeded the target wallet's limit. Request rejected. Corrective action: Transfer an amount not exceeding the target wallet limit. |

| Card Authentication Failed Error | The requested card payment requires 3DS authentication, but authentication was not completed within the specified time. Payment canceled. Corrective action: None. Create another payment. |

When encountering the above issues, promptly verify transaction information to ensure the transaction ID and amount are entered accurately. If card authentication fails, try replacing the bank card or contact platform customer service for assistance.

Recommendation: Throughout the entire conversion process, be sure to save all transaction receipts and operation records for subsequent inquiries and risk tracing.

Through standardized operation processes and reasonable fund flow planning, you can efficiently and securely achieve the conversion of Argentine pesos to USD assets, minimizing the risk of asset depreciation in a high-inflation environment.

Mainstream Digital Wallets

When choosing a digital wallet, you need to focus on the platform's business scope, supported currencies, fund security, and fee structure. Mainstream wallets such as Binance, MercadoPago, and Wise each have their own characteristics and suit different asset preservation needs. You can intuitively understand the core functions of these wallets through the table below:

| Wallet Name | Number of Supported Currencies | Multi-Currency Accounts | Fund Storage & Conversion | Bank Card Function | Security Measures | Applicable Scenarios |

|---|---|---|---|---|---|---|

| Binance | Over 50 | Supported | Real-time conversion | Virtual/physical card | Dual identity verification, audits | Global asset allocation |

| MercadoPago | Mainly Latin American currencies | Supported | Fast transfers | Virtual card | Transaction monitoring, encryption | Local consumption, payments |

| Wise | 50+ | Supported | Instant conversion | Virtual/physical card | Multi-authentication, fund custody | International remittances, wealth management |

| BiyaPay | USD, HKD, etc. | Supported | Real-time conversion | Not supported | Multiple encryption, risk control | USD asset storage, withdrawals |

Binance

When using Binance, you can manage over 50 world currencies, suitable for global asset allocation. The platform supports multi-currency accounts with instant fund conversion. You can apply for physical or virtual cards linked to Google Pay or Apple Pay for easy international spending. Binance uses dual identity verification and regular audits to ensure fund security. In a high-inflation environment, you can flexibly switch assets to reduce exchange rate risks.

Binance is suitable if you have cross-border asset allocation needs, pursue diversified investment, and high liquidity.

MercadoPago

When using MercadoPago in Argentina and Latin America, you can conveniently manage local currencies. The platform supports fast transfers and local consumption, suitable for daily payment scenarios. You can apply for virtual cards to enjoy promotions and cashback activities. MercadoPago uses transaction monitoring and data encryption to ensure account security. In the local market, you can efficiently cope with inflation and currency depreciation.

MercadoPago is suitable if you focus on local consumption, daily payments, and asset circulation.

Wise

When choosing Wise, you can manage over 50 currencies, support multi-currency accounts, and instant fund conversion. The platform provides virtual and physical cards for easy international remittances and wealth management. Wise uses multi-authentication and fund custody measures to ensure fund security. You can enjoy low fees and favorable exchange rates for international remittances.

Wise is suitable if you have international fund flow needs, focus on exchange rate costs, and fund security.

For USD asset storage and withdrawals, you can prioritize BiyaPay. The platform supports currencies such as USD and HKD, uses multiple encryption and risk control measures, and is suitable for Chinese-speaking users to preserve USD assets and withdraw to Hong Kong licensed banks. You need to reasonably choose a digital wallet based on your own needs to optimize your asset allocation structure.

Risks and Precautions

Exchange Rate Fluctuations

When using a digital wallet to convert Argentine pesos to USD, you must pay close attention to exchange rate fluctuation risks. The Argentine peso value is extremely unstable, remaining in a state of high or even hyperinflation for a long time. The government implements strict capital controls, making it difficult for funds to enter and exit the country, with many transactions only possible through unofficial channels. There is a huge difference between the official exchange rate and the black market rate, which directly affects your conversion costs and asset security. When selecting conversion timing, closely monitor market conditions to avoid asset shrinkage due to short-term sharp fluctuations.

It is recommended to prioritize platforms with transparent exchange rates and real-time market support, lock in rates promptly, and reduce uncontrollable risks.

- Argentina's currency has long-term high inflation, with exchange rates prone to sharp fluctuations

- Capital controls lead to large gaps between official and black market rates

- Exchange rate fluctuations directly affect conversion costs and asset value

Fees

When performing currency conversions and withdrawals, be sure to pay attention to the various fee structures. Different digital wallets and payment methods charge varying fees, and some platforms also charge additional fees based on transaction amount, currency, and channel. The table below summarizes common fee types and rates in the Argentine market:

| Fee Type | Fee Description |

|---|---|

| Merchant Fees | Depends on payment method and processing service, usually lower |

| Interchange Fees | Average interchange fee for debit cards is 1.50% |

| Payment Gateway Fees | May be a percentage of transaction amount or fixed fee |

| Cross-Border Fees | Includes international processing fees and currency conversion fees |

| Merchant Discount Rate | Debit card service fee 1.2%, credit card 2.5% |

| 2021 New Rates | Debit card 0.6%, credit card 1.3% |

When choosing a platform, carefully understand the various fee standards, reasonably plan fund flows, and avoid excessive fees eroding asset returns. Some platforms may temporarily adjust rates during high-volatility periods, so it is recommended to check platform announcements in advance.

Compliance and Security

When using a digital wallet for asset conversion, you must value the platform's compliance and fund security. Argentine regulatory authorities require all virtual asset service providers to register with the National Securities Commission and strictly comply with anti-money laundering and counter-terrorism financing regulations. Platforms must identify all customers and continuously monitor transactions, reporting anomalies promptly to the Financial Intelligence Unit. The table below lists the main regulatory requirements:

| Regulatory Requirement | Description |

|---|---|

| Registration | Must register as a virtual asset service provider with the National Securities Commission |

| Anti-Money Laundering and Counter-Terrorism Financing | Must comply with relevant regulations, implement customer due diligence and ongoing monitoring |

| Tax Obligations | Profits from digital currency sales are subject to income tax |

| Customer Due Diligence | Must identify and verify all customers and their ultimate beneficial owners |

| Ongoing Monitoring | Must continuously monitor customer transactions to detect anomalous or suspicious activities |

| Reporting to Financial Intelligence Unit | Report terrorism financing-related suspicious transactions within 48 hours, money laundering-related within 150 days |

You also need to be vigilant against various fraud risks. Current common scams include cryptocurrency Ponzi schemes, deepfake investment scams, stablecoin trading scams, women's empowerment pyramid schemes, and cross-border scams. Scammers often lure users to transfer money through social media, phishing sites, or fake platforms. The table below summarizes the main scam types and characteristics:

| Scam Type | Characteristic Description |

|---|---|

| Cryptocurrency Ponzi Schemes | Promise high returns, require recruiting new investors, common in Telegram and WhatsApp groups |

| Deepfake Investment Scams | Use celebrity deepfake videos, promise quick high returns, invite to join groups |

| Stablecoin Trading Scams | Fake exchanges offer better rates than legitimate platforms, phishing sites mimic well-known platforms |

| Women's Empowerment Pyramid Schemes | Under the guise of women's empowerment, require recruiting new members for promotion, common on WhatsApp |

| Cross-Border Scams | Romance scams targeting expatriates, fake remittance services, investment opportunity scams |

During operations, rationally judge platform qualifications, never lightly believe high-return promises, and avoid large transactions through unofficial channels. It is recommended to regularly check account security, properly store transaction receipts, and guard against various frauds and fund losses.

In the environment of the Argentine peso crash, choosing a digital wallet to convert to USD can efficiently cope with asset depreciation. Digital wallets are spreading rapidly, with e-commerce transaction volume reaching $33 billion in 2024, and security protocols and risk management measures continue to upgrade. You should pay attention to compliance requirements, operate rationally, and prioritize legitimate platforms. In the future, as market size continues to grow, digital wallets will become an important tool for asset preservation.

- Main process: Register real-name verification → Bind bank card → Recharge pesos → Convert to USD → Withdraw or store

- Precautions: Check exchange rates, pay attention to fees, beware of scams, save transaction receipts

FAQ

How to choose a compliant platform when converting to USD using a digital wallet?

You should prioritize platforms already registered with Argentina's National Securities Commission. The platform must have anti-money laundering and counter-terrorism financing compliance qualifications and publicly disclose relevant policies.

How to reduce losses when encountering exchange rate fluctuations during conversion?

You can monitor the platform's real-time exchange rates and choose to operate during periods of lower volatility. Some platforms support rate-locking features, which help reduce conversion costs.

How long does it take to withdraw to a Hong Kong licensed bank account?

You usually receive funds within 1-2 business days. The specific arrival time depends on the platform's review speed and the bank's processing efficiency.

Is it safe to store USD in a digital wallet?

When using mainstream digital wallets, the platform adopts multiple encryption and risk control measures. You need to regularly check your account to ensure fund security.

What are the main fees for conversion and withdrawal?

You need to pay attention to the fee standards publicly disclosed by the platform. Common fees include conversion fees, withdrawal fees, and cross-border processing fees, with specific amounts priced in USD.

*This article is provided for general information purposes and does not constitute legal, tax or other professional advice from BiyaPay or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or warranties, express or implied, as to the accuracy, completeness or timeliness of the contents of this publication.

Related Blogs of

IBM Plunges While ASML Rises: Is Capital Rotating from Software to AI Hardware?

How Much Is Venmo Worth in the PayPal Acquisition Case? User Scale, Revenue, and Strategic Value

Comparing the Beneficiaries of the AI Equipment Cycle: ASML, Applied Materials, Lam Research, and KLA

Understanding Net Interest Margin and Provision Changes Through JPM, BAC, and Citi

Choose Country or Region to Read Local Blog

Contact Us