- More

- Download

A Bank Card Freeze Caused by Withdrawal Nearly Ruined My US Visa: A Painful Lesson in Cross-Border Fund Safety

Image Source: pexels

You may not imagine how passive a situation a bank card freeze can put you in during cross-border life. A simple withdrawal operation directly caused your account to be frozen, and your originally smooth US visa application nearly fell through because of it. Fund safety not only concerns daily convenience but also determines whether you can realize your dreams of studying abroad, working, or immigrating. This sudden crisis made you deeply realize that risks and lessons are hidden behind every fund transfer.

Key Takeaways

- A bank card freeze may affect your fund flows and visa application, so stay vigilant and understand the risks.

- When making large withdrawals, notify the bank in advance and provide proof of fund sources to reduce the risk of being frozen.

- Keep your account active and regularly update personal information to avoid freezes due to dormant accounts.

- When encountering a bank card freeze, contact the bank immediately, prepare relevant documents, and actively cooperate with the review process.

- Comply with international financial regulations, ensure transparent fund flows, and build greater trust from the bank.

The Full Process of Bank Card Freeze

Image Source: pexels

The Trigger: Withdrawal Operation

You may need to transfer funds from a mainland China account to a US account for tuition, living expenses, or investment purposes. You hope to complete this withdrawal through compliant channels to ensure the funds arrive safely in the US. You chose a licensed Hong Kong bank as an intermediary, planning to first remit USD to the Hong Kong account and then transfer it to the US. You believe this can reduce risks and improve fund transfer efficiency.

However, the bank's risk control system strictly monitors all withdrawal operations. You may not realize that the following situations can easily trigger a bank card freeze:

- Bank suspects fraud: If you suddenly make a large withdrawal or your account has recently shown frequent transactions in different cities, the bank will consider your account abnormal and automatically trigger risk control measures.

- Unpaid debts: If you have unsettled bills or debts, creditors may apply for an account freeze through judicial procedures.

- Suspected illegal activity: If your account has ever been associated with suspicious fund flows, the bank will immediately freeze it to prevent further risks.

You thought that as long as the documents were complete and the process compliant, the funds would arrive safely. In reality, the bank's risk control system is far more sensitive than you imagine. A seemingly ordinary withdrawal operation may trigger risk controls due to details such as amount, frequency, or payee information, resulting in a bank card freeze.

The Freezing Process

After completing the withdrawal, you suddenly found that your account could no longer be used normally. You tried logging into online banking, and the system prompted “Account has been frozen.” You could not transfer money, withdraw cash, or even check your balance. Feeling anxious, you immediately called the bank’s customer service hotline.

The customer service informed you that due to recent abnormal large withdrawals on the account, the system automatically triggered risk controls and froze your bank card. You need to visit a bank branch in person, bring identification, proof of fund sources, and other materials to cooperate with the investigation. Only then did you realize that a bank card freeze is not just a locked account—it means your funds are temporarily “seized,” and all financial activities are suspended.

You queued at the bank counter, waiting for staff to review your materials. You had to explain in detail the source, purpose, and transaction background of the funds. The bank required a series of supporting documents such as pay stubs, contracts, and remittance vouchers. You felt unprecedented pressure because every document was directly related to whether the account could be successfully unfrozen.

While waiting for the bank’s internal review results, your account remained unusable. You discovered that a bank card freeze not only affects daily spending but also leaves you passive at critical moments.

Visa Application Obstructed

You originally planned to submit bank statements and proof of deposit during your US visa interview to prove you had sufficient funds to support your study and life in the US. Now, with your bank card frozen, you could not obtain valid proof of funds. You anxiously contacted the bank, hoping to unfreeze the account as soon as possible, but the bank’s review process was strict and difficult to resolve quickly.

You had to explain the situation to the visa center and supplement other materials. You worried that the visa officer might doubt your fund sources or even affect the visa outcome. You felt the chain reaction caused by the bank card freeze—not only impacting fund flows but also directly threatening your US visa application.

You understood that fund safety and compliant account management are the foundation of cross-border life. One bank card freeze is enough to make you pay a heavy price in time and opportunities. You began reflecting on how to avoid similar risks in the future and protect your fund safety and smooth visa process.

Common Risks of Bank Card Freezes

Risk Control and Judicial Freezes

When moving funds cross-border, you often encounter strict monitoring by the bank’s risk control system. Banks assess risks based on multiple dimensions such as transaction amount, frequency, and geographic location. The following situations can easily trigger a bank card freeze:

- Increased risk of online fraud, especially during holidays, where even legitimate transactions may be misjudged as abnormal.

- Failure to comply with international financial regulations (such as anti-money laundering and customer identification laws) can lead to payment delays or even account freezes.

- Currency conversion errors or exchange rate fluctuations may cause your payment to be flagged by the system.

- Sudden surges in transaction volume can exceed the bank’s processing capacity, easily leading to payment errors or freezes.

- Merchants in high-risk industries receive extra scrutiny from banks, making fund flows more restricted.

Judicial freezes often result from lawsuits, debts, or involvement in investigations. Once you encounter a judicial freeze, the unfreezing process becomes complicated and usually requires waiting for legal proceedings to conclude. Stay alert, monitor your account activity in time, and avoid your own fund safety being affected due to others’ involvement.

Long Periods of Account Inactivity

If your account has no transactions for a long time, the bank will classify it as dormant. When you fail to update personal information or cannot be contacted, the bank will proactively freeze it. Refer to the table below to understand common scenarios of account dormancy:

| Account Status | Bank Measure | Unfreezing Process |

|---|---|---|

| Long-term inactivity | Freeze | Provide identification and activation application |

| Information not updated | Freeze | Complete the information |

| Unable to contact holder | Freeze | Visit branch to verify identity |

By keeping your account active and regularly updating information, you can effectively reduce the risk of dormancy freezes.

Fund Source Review

Banks scrutinize the sources of cross-border fund flows very strictly. During large transfers or frequent transactions, banks focus on the following aspects:

| Risk Factor | Description |

|---|---|

| Transaction volume and amount | The larger the number and amount of fund transfers, the higher the risk |

| Geographic location | The geographic locations of the fund source and beneficiary affect risk assessment |

| Customer identity | Whether the fund initiator or beneficiary is a bank customer affects the intensity of review |

If you cannot provide a clear explanation of fund sources, the bank will restrict your account operations. Without necessary payment information, the bank cannot monitor suspicious activities effectively, easily triggering a bank card freeze. You should proactively cooperate with the bank’s customer due diligence, prepare pay stubs, contracts, remittance vouchers, and other materials to enhance fund transparency.

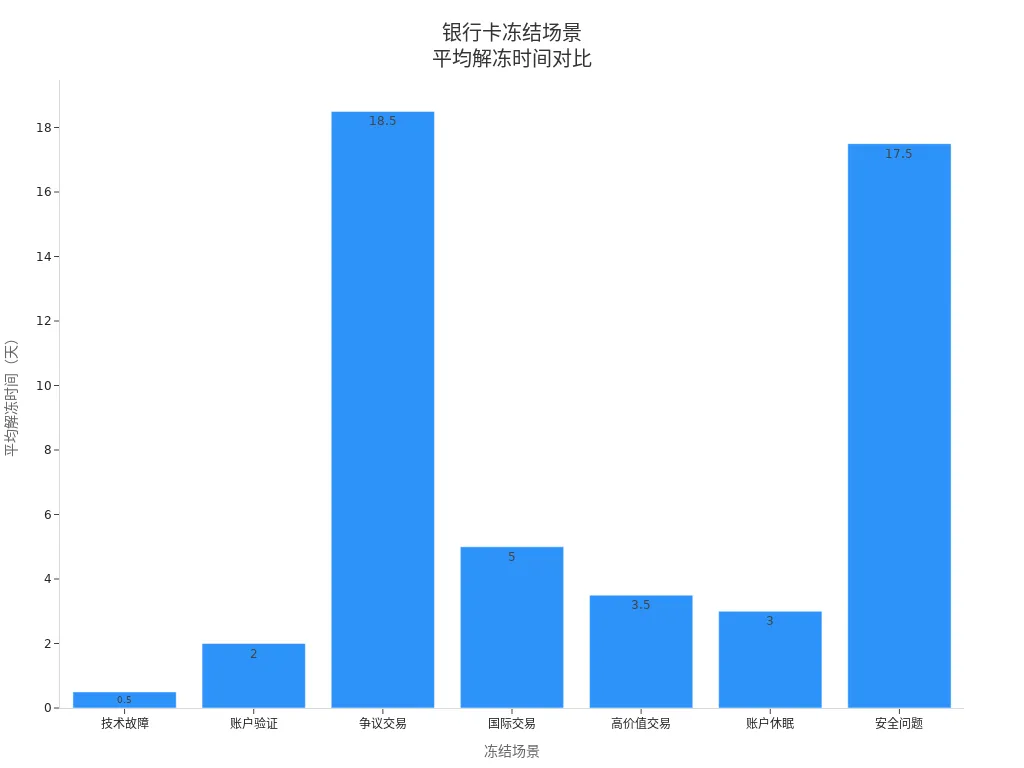

You may be concerned about the unfreezing duration for different types of freezes. The chart below shows the average unfreezing time in common scenarios:

By actively cooperating with the bank and promptly submitting materials, most technical or risk-control freezes can be resolved within a few days. Judicial or compliance reviews require patience and may take weeks or even months. Believe that as long as you operate compliantly, the bank card freeze will eventually be lifted, and fund safety remains controllable.

Measures to Handle Fund Freezes

Image Source: unsplash

Process for Contacting the Bank

When encountering a bank card freeze, stay calm and take action immediately. You can follow these steps to handle it efficiently:

- Immediately contact your bank or payment service provider, inquire about the reason for the freeze, and request a written explanation. This creates evidence for follow-up communication.

- Gather all compliance documents related to the funds, including proof of fund sources, contracts, invoices, etc. The more prepared you are, the faster the bank’s review will be.

- If you have regular incoming or outgoing payments, temporarily transfer these funds to a backup account to avoid affecting daily life.

- Pause all non-essential external transfers and focus on resolving the current issue.

- Proactively communicate with partners or clients, explain the situation, and ensure the safety of their funds.

When communicating with the bank, remain patient and courteous. Clearly state your needs, verify the freeze reason, collect all relevant documents, and follow the bank’s instructions. If you encounter difficulties, request intervention from senior bank management or the compliance department. Also save all communication records for future reference.

Proving Fund Sources

During bank review, you need to provide detailed proof of fund sources. Prepare the following materials:

- Detailed invoices

- Signed contracts

- Pay stubs

- Tax returns

- Government-issued valid ID

- Recent account statements

- Sales agreements

- Relevant correspondence records

The more clearly you demonstrate the flow of funds, the easier it is for the bank to determine the compliance of your transactions. Organize all materials in advance to ensure every fund transfer can be traced back to its source.

Supplementing Visa Materials

If the bank card freeze affects your visa application, proactively communicate with the visa center. Explain the reason for the temporary fund freeze and supplement other available proof of funds, such as statements from other bank accounts, asset certificates, or family sponsorship materials. Explain the situation clearly and sincerely so the visa officer believes your fund sources are genuine and reliable. You can also attach written records of communications with the bank to prove you are actively resolving the issue.

By actively responding and reasonably preparing materials, you can resolve the crisis caused by the bank card freeze. Every challenge is an opportunity to grow and improve your fund management skills.

Suggestions to Prevent Bank Card Freezes

Withdrawal Precautions

When making cross-border withdrawals, maintain high vigilance. Using a licensed Hong Kong bank as an intermediary can enhance the safety of fund flows. Plan withdrawal amounts reasonably and avoid sudden large transfers. Notify the bank in advance about the purpose and source of funds.

If your concern is not only whether the funds can move out, but whether the transfer path will later stand up to bank review and document checks, then channels with a clearer record trail matter more. A service such as the BiyaPay website, positioned as a multi-asset trading wallet covering cross-border payments, trading, and fund management scenarios, can first be used to review cost through its free exchange rate comparison tool, and then to check the related remittance route information. In practice, what reduces freeze risk is not speed alone, but whether the purpose of funds, transfer path, and supporting records can all remain consistent under bank or visa-related review.

Refer to the following suggestions:

- Plan withdrawal timing, conduct in batches, and reduce single-transaction amounts.

- Retain all transaction vouchers and be ready to explain fund flows to the bank at any time.

- Notify the bank in advance to avoid legitimate transactions being misjudged as abnormal.

- Use compliant channels such as BiyaPay, which provides global payment and remittance services for Chinese-speaking users, ensuring funds arrive smoothly in US accounts.

By proactively communicating, the bank will more easily understand your fund needs and reduce freeze risks.

Compliant Fund Flows

Comply with requirements for cross-border fund transfers. Banks strictly review fund sources under BSA/AML policies. Take the following measures:

- Conduct customer due diligence to ensure complete identity information.

- Provide detailed contracts, invoices, and remittance vouchers to enhance fund transparency.

- Monitor automated systems for fund transfers and promptly detect suspicious activities.

- For transfers involving special jurisdictions, proactively cooperate with enhanced bank reviews.

- Ensure complete payment information, without omitting or altering any transaction data.

Compliant operations not only protect your fund safety but also provide solid assurance for your US visa application. Make every fund flow transparent and traceable.

Account Security Management

Develop good account security habits. Regularly change strong passwords, monitor credit reports, and use secure communication channels to contact the bank. Pay attention to the following details:

| Security Measure | Practical Advice |

|---|---|

| Password management | Create strong passwords and change them regularly |

| Credit monitoring | Regularly check credit reports and scores |

| Communication security | Use secure channels to contact the bank |

| Network usage | Avoid public Wi-Fi for transactions |

| Information protection | Do not share personal information with strangers |

By actively managing account security, fund risks are greatly reduced. Every meticulous operation is an investment in your future cross-border life. With strong fund safety management skills, you will feel more confident and at ease with your US visa and international life.

Only after experiencing a bank card freeze will you truly understand the importance of fund safety in cross-border life. Plan fund flows in advance and operate compliantly to avoid account issues affecting your visa and future development. Every crisis is an opportunity for growth—protect your dreams with action.

FAQ

How long does it take to unfreeze a bank card after it is frozen?

As long as you actively cooperate with the bank, risk control reviews can usually be completed within a few days. Judicial freezes may take weeks. Prepare all proof materials and patiently wait for bank notification.

How can I prevent a bank card freeze in advance?

Regularly update account information and keep the account active. Withdraw funds in batches and notify the bank in advance about fund purposes. By proactively operating compliantly, the bank will have greater trust in your fund flows.

Will a fund freeze affect my US visa?

If you cannot provide proof of funds in time, the visa officer may question your financial capability. Prepare statements from backup accounts or asset proof, actively communicate with the visa center, and demonstrate your integrity and problem-solving ability.

What channels are safer for cross-border withdrawals?

You can choose licensed Hong Kong banks as intermediaries to improve fund safety. You can also use BiyaPay and other compliant services to meet the global payment and remittance needs of Chinese-speaking users, ensuring funds arrive smoothly in US accounts.

What proof of fund sources does the bank require?

You need to provide pay stubs, contracts, remittance vouchers, tax documents, and other materials. The more clearly you demonstrate fund flows, the easier it is for the bank to determine transaction compliance. Organize all documents in advance to improve review efficiency.

*This article is provided for general information purposes and does not constitute legal, tax or other professional advice from BiyaPay or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or warranties, express or implied, as to the accuracy, completeness or timeliness of the contents of this publication.

Related Blogs of

ASML Q2 2026 Earnings Analysis: What Signals Did Orders, EUV Demand, and Full-Year Guidance Release?

Where Will IBM Stock Go After Q2 Earnings? Three Scenarios Based on Revenue, Red Hat, and Free Cash Flow

JPM, BAC, GS, MS, and Citi: Which Bank Stock Is More Worth Buying? A Comparison of Valuation, Dividends, and Business Structure

Will PayPal Accept Stripe’s Offer? Three Major Obstacles: Board Approval, Financing, and Regulation

Choose Country or Region to Read Local Blog

Contact Us