- More

- Download

How to Prevent AI Fraud in Cross-Border Large-Value Fund Transfers? Choose Institutions with Compliance Licenses and Bank-Level Risk Controls

Image Source: pexels

When conducting cross-border large-value fund transfers, you must prioritize financial institutions that hold compliance licenses and maintain bank-level risk control systems. AI fraud techniques are becoming increasingly sophisticated, making it difficult to identify risks relying solely on personal experience. Professional institutions, through compliant frameworks and stringent risk control measures, can effectively detect and intercept complex fraudulent activities. You can see that the global cross-border payment volume continues to expand, projected to reach $194.6 trillion in 2024 and potentially grow to $320 trillion by 2032:

| Year | Total Cross-Border Payments (Trillion USD) |

|---|---|

| 2024 | 194.6 |

| 2032 | 320 |

The surge in cross-border fund flows means the risks you face are increasing simultaneously. Only by relying on compliance and robust risk control systems can you better safeguard your funds.

Key Points

- Choose financial institutions with valid compliance licenses to ensure fund safety and legality.

- Stay alert to AI fraud techniques such as deepfakes and voice cloning to protect your personal information.

- Pay attention to whether the institution has bank-level risk control systems, including real-time monitoring and multi-factor authentication.

- Regularly verify the institution’s compliance information using official databases to confirm legitimacy.

- Enhance your own fraud prevention awareness and strictly follow payment verification processes to avoid information leakage.

AI Fraud Risks in Cross-Border Large-Value Transfers

Image Source: pexels

Common AI Fraud Techniques

During cross-border large-value transfers, you must be vigilant against various AI-powered fraud techniques. Currently, deepfakes, voice cloning, and synthetic identity fraud have become mainstream methods:

- Deepfake technology can generate fake executive appearances in real-time during video conferences, tricking employees into making transfers.

- Voice cloning allows fraudsters to imitate familiar leaders or clients, significantly increasing success rates. In 2024, nearly 28% of adults in the UK have encountered such fraud, yet nearly half remain unprepared.

- Synthetic identity fraud is surging, with AI forging documents and biometric data to bypass traditional KYC and AML checks.

- Traditional methods like money laundering and triangular fraud have become harder to detect due to AI empowerment.

You should also note that AI-generated videos and audio can precisely mimic business leaders, colleagues, or clients, exploiting trust in familiar faces and greatly elevating risks in cross-border large transfers.

Risk Points in Fund Flows

Cross-border large-value transfers involve multiple stages, and any oversight can be exploited by AI fraudsters. The table below summarizes the main risk points and related data:

| Risk Point | Related Data or Cases |

|---|---|

| Money laundering cost | Estimated annually between USD 800 billion and USD 2 trillion, accounting for 2%-5% of global GDP |

| Non-compliance fines | Global AML fines reached USD 460 million in 2024 |

| Major compliance cases | TD Bank fined USD 3.09 billion for negligence involving USD 670 million in laundering cases |

In practice, you may also encounter complex processes, payment delays, and lack of transparency—issues that provide opportunities for AI fraud. Many institutions rely on traditional one-time KYC checks at account opening with low follow-up update frequency, allowing risks to accumulate over time.

Real Cases and Impact

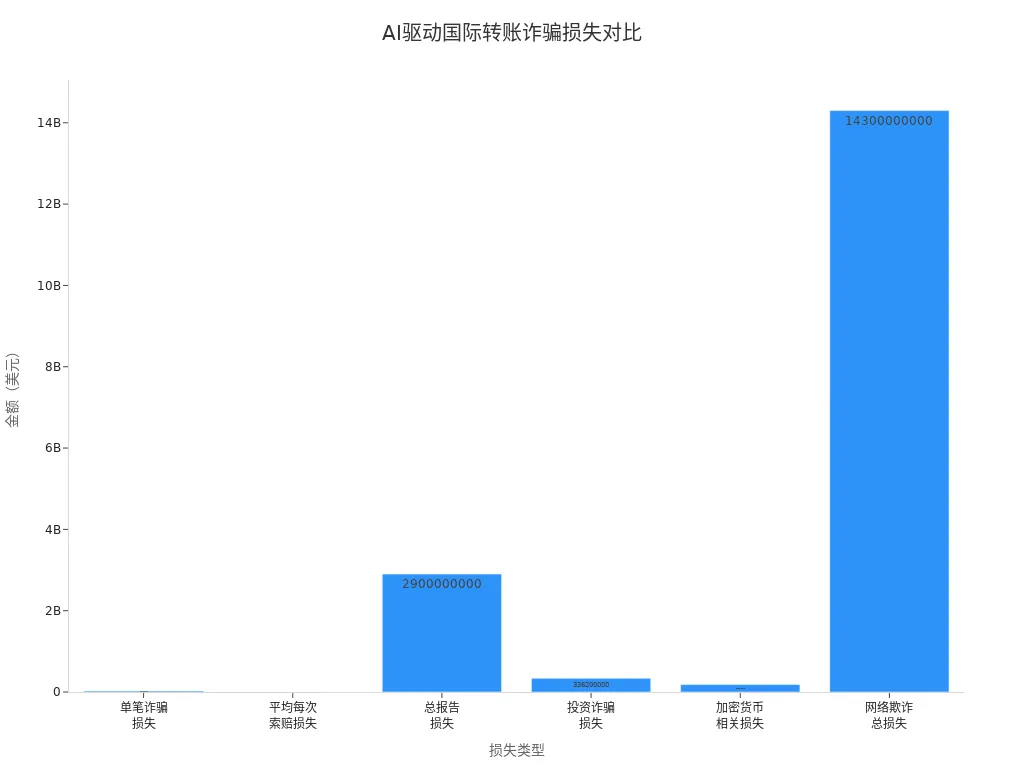

In 2024, a senior executive at a Hong Kong company fell victim to deepfake technology during a video conference, mistakenly transferring USD 25 million to a fraudulent account. This incident highlights the extreme stealth and destructive power of AI-driven cross-border large-transfer fraud. Data shows that in 2023, funds transfer fraud and business email compromise accounted for 56% of all cyber claims, with investment fraud losses reaching USD 336 million. The chart below illustrates loss amounts from different types of AI-driven international funds transfer fraud:

You must recognize that every step in cross-border large transfers can become a target for AI fraud. Only by relying on compliance frameworks and bank-level risk controls can you minimize potential losses.

Significance of Compliance Licenses

Compliance Protects Fund Safety

When performing cross-border large-value transfers, you must check whether the financial institution holds a compliance license. A compliance license not only signifies legitimate operations but directly relates to fund safety. Licensed institutions strictly implement KYC procedures to verify client identity authenticity and reduce financial crime risks. You can see that compliance frameworks include Customer Due Diligence (CDD) and Enhanced Due Diligence (EDD), helping institutions identify and assess potential risks. Compliant institutions also adopt advanced technologies to handle multi-jurisdictional legal requirements, ensuring fund flows meet international standards. When selecting services, prioritize institutions that maintain detailed records and continuously monitor regulatory updates—this enables effective risk management and fund protection.

A compliance license is the foundation of legitimate financial operations and your first line of defense for fund safety. Only through rigorous identity verification and risk assessment can you maximally defend against sophisticated AI-driven fraud.

- KYC procedures ensure client identity verification

- Customer Due Diligence (CDD) and Enhanced Due Diligence (EDD) identify risks

- Adoption of advanced technology supports multi-jurisdictional compliance

- Maintain detailed records and monitor regulatory updates

Regulatory Framework and Information Disclosure

In cross-border financial services, you must understand the importance of regulatory frameworks and information disclosure. Compliance requires institutions to follow Anti-Money Laundering (AML) and Know Your Customer (KYC) regulations to protect your rights. Data privacy and security are core to cross-border rules— institutions must obtain your explicit consent before international data transfers. Regulatory authorities supervise financial service providers’ activities to ensure compliance with local laws and safeguard your interests. You can assess compliance level and transparency by reviewing the institution’s information disclosures.

- Compliance ensures adherence to AML and KYC regulations

- Data privacy and security protect user rights

- Regulatory authorities oversee financial service activities

- Information disclosure enhances transparency and trust

During cross-border large transfers, only licensed and regulated institutions can provide higher fund safety and user rights protection.

Bank-Level Risk Control Systems

Image Source: unsplash

Bank-level risk control systems provide solid security for cross-border large-value transfers. When choosing financial service providers, you must verify whether they maintain comprehensive risk controls. Modern bank-level risk systems typically include the following core elements:

- KYC (Know Your Customer) processes

- Enhanced Due Diligence (EDD)

- Transaction monitoring

- Compliance measures

Real-time monitoring powered by intelligent automation ensures rapid response to emerging threats, enabling proactive risk mitigation.

Multi-Factor Authentication

When conducting large cross-border transfers, financial institutions require multi-factor authentication (MFA) to prevent unauthorized access. MFA combines passwords with biometrics, identity document verification, and other methods, effectively defending against stolen credentials and fake identities. Many institutions require selfie checks and liveness detection before large transfers to further enhance security. Server-side biometric facial authentication has become a key measure to prevent account takeover, especially requiring full re-verification when changing credentials.

Transaction Monitoring and Alerts

Bank-level risk control systems use AI and big data to analyze every transaction in real time. You will find the system can automatically identify suspicious behavior, including small deposits across multiple accounts, sudden changes in transaction patterns, atypical geographic fund flows, etc. AI monitoring tools detect anomalies and fraud patterns faster and more accurately, reducing false positives. Each company establishes flags for suspicious behavior elements and notifies staff of suspicious transactions via technical means in a timely manner. Machine learning and behavioral analysis learn your typical transaction habits, quickly flag anomalies, enable real-time decisions, and instantly block suspicious activity.

As transaction data volumes continue to grow, traditional rule-based monitoring is no longer sufficient. Today, organizations need unsupervised machine learning and predictive analytics-driven anomaly detection platforms to discover unknown risk patterns in real time.

Anti-Money Laundering and Anti-Fraud

In cross-border large transfers, you must rely on AI-driven AML and anti-fraud measures. AI can analyze complex financial behaviors, identify hidden risks and layering techniques, and uncover transactions concealing illicit origins. Real-time fraud monitoring, machine learning, behavioral analysis, and data sharing have become mainstream technologies. The table below summarizes key technologies and their functions:

| Technology | Description |

|---|---|

| Real-time fraud monitoring | Instantly identifies and blocks suspicious transfers to prevent rapid fund loss. |

| Machine learning | Processes massive transaction streams, quickly identifies anomalies, and reduces false positives. |

| Behavioral analysis | Learns clients’ typical transaction patterns and promptly flags anomalies. |

| Data sharing | Banks share known threat data to build a comprehensive real-time risk picture. |

You should also understand that banks must comply with international AML regulations such as the U.S. Bank Secrecy Act (BSA), promptly file Currency Transaction Reports (CTR) and Suspicious Activity Reports (SAR), and designate responsible personnel to ensure compliance and fund safety.

How to Identify Compliant and High-Risk-Control Institutions

In cross-border large-value transfers, you need a systematic approach to identify compliant, high-risk-control institutions. Compliance and risk control capabilities directly determine fund safety and transaction smoothness. The following provides practical, scenario-based guidance to help you scientifically select partners.

Verify Compliance Licenses

You can verify a financial institution’s compliance license through official databases and authoritative websites. A compliance license is the foundation of legitimate operations and the primary standard for judging whether an institution is regulated. Different countries and regions have their own regulatory systems; some mainstream databases are listed below:

| Source | Description |

|---|---|

| Federal Reserve | Provides measurement and data analysis on cross-border securities positions. |

| U.S. Treasury | Through FinCEN, issues operations and data related to potential money laundering. |

| FinCEN | Publishes public and non-public advisories on money laundering or terrorist financing threats. |

When selecting an institution, prioritize checking whether it is registered with relevant regulators and holds valid licenses for payment, remittance, currency exchange, etc. For example, Hong Kong licensed banks and payment institutions must be registered with the Hong Kong Monetary Authority or relevant departments, with publicly transparent information.For users who frequently handle large cross-border fund movements, checking licenses is only the first step. It is also important to keep exchange, remittance, and account management within the same compliance framework whenever possible, so that unnecessary redirects and unofficial paths do not create extra fraud exposure or information distortion. A platform such as BiyaPay, positioned as a multi-asset trading wallet, covers cross-border remittance, fiat-to-digital conversion, and fund management, which fits scenarios where efficiency, compliance, and risk control all matter.

Before initiating a large transfer, users can also review real-time pricing and costs through the official exchange rate comparison tool and then decide on the transfer path. In large-value scenarios, multi-jurisdiction compliance credentials, continuous monitoring, and abnormal transaction interception are often more important than a simple promise of speed, because they directly affect whether fund paths remain clear, information stays traceable, and losses can be limited quickly if something goes wrong. For institutions offering global payments, fiat-to-crypto exchange, USDT-to-USD/HKD conversion, and Hong Kong/US stock fund support, compliance is especially critical. Cross-verify through official websites, regulatory announcements, license numbers, and multiple channels to ensure authenticity.

A compliance license is not only a symbol of legitimate operations but also your first line of defense for fund safety. Any institution unable to provide clear license information should raise immediate concern.

Evaluate Risk Control Capabilities

You need to assess an institution’s risk control system from multiple dimensions. Institutions with strong risk controls can effectively detect and block sophisticated AI-driven fraud, safeguarding funds in cross-border large transfers. Evaluation criteria include but are not limited to:

| Evaluation Criterion | Description |

|---|---|

| Employee count | Staff size affects applicability of certain regulations; larger institutions may face more compliance requirements. |

| Geographic scope | Operational range influences required regulatory frameworks; cross-border operations increase compliance complexity. |

| Legal structure | Legal form determines applicable regulatory requirements (e.g., bank holding company vs. non-bank financial institution). |

| Market capitalization | Systemically important institutions face stricter supervision and capital requirements. |

| Risk profile | Risk profile affects regulatory intensity and specific rules, especially capital adequacy and liquidity. |

| Turnover/revenue | Certain regulations apply differently based on turnover or revenue levels. |

| Activity type | Nature of activities determines specific applicable regulations (e.g., high-frequency trading or consumer lending). |

You can check whether the institution has the following capabilities:

- Real-time monitoring of large cross-border transactions, ability to identify transaction spikes or operations nearing reporting thresholds.

- Automated alerts for high-risk behaviors such as dormant accounts, abnormal fund flows, failed identity verification, etc.

- Adoption of AI and machine learning to enhance anomaly detection and anti-fraud capabilities.

- Differentiated risk controls tailored to different business types (e.g., cryptocurrency, e-commerce, insurance).

For example, PayPal blocks $500 million in fraud quarterly, demonstrating significant ROI from high-level risk control systems. You can review publicly available risk control reports, technical whitepapers, and annual compliance disclosures to understand the maturity and effectiveness of their risk systems.

Leverage Third-Party Evaluations

You can use third-party evaluations and authoritative industry reports to assist in judging compliance and risk control capabilities. Third-party assessments are generally more objective and reveal real-world performance. Common third-party sources include:

- Financial security ratings from international rating agencies.

- Annual compliance rankings from industry associations or regulators.

- In-depth investigations and case analyses by professional media.

- Genuine user reviews and complaint records on authoritative platforms.

You can check whether the institution has received compliance awards, faced penalties, or had major complaints. For institutions involved in global payments, fiat-to-crypto exchange, and Hong Kong/US stock fund support, third-party evaluations are especially important. You can also reference industry best practices to understand their application of identity verification, AML, behavioral analysis, etc. Modern financial institutions commonly adopt multi-factor authentication, behavioral analysis, and AI-driven anomaly detection to elevate overall anti-fraud levels.

Through multi-channel cross-verification, you can gain a more comprehensive understanding of an institution’s true risk control capabilities and reduce decision risks from information asymmetry.

User Self-Protection Recommendations

While identifying compliant and high-risk-control institutions, you must also enhance your own fraud prevention awareness. AI-driven fraud techniques are increasingly complex; relying solely on institutional controls is not enough to fully mitigate risks. You can take the following measures:

- Recognize warning signs: Be wary of unusual requests, especially emails or texts demanding sensitive information.

- Verify identity: Before sharing sensitive information, confirm the other party’s identity through phone, video, and multiple channels.

- Upgrade technology: Use AI and machine learning tools to strengthen your own security defenses.

- Enhance email filtering: Employ AI to filter suspicious emails and reduce phishing risks.

- Implement strict payment verification: Require dual confirmation for every large payment to avoid single-point failures causing fund loss.

- Use dual authorization: Involve two employees in payments and user management to increase operational security.

- Continuous training: Regularly attend anti-fraud and information security training to improve fraud detection ability.

You should also check whether the institution adds extra verification steps during suspected attacks and emphasizes KYC/AML identity verification processes. Modern fraud often involves multi-step coordinated attacks—only when institutions and users jointly elevate protection levels can risks be minimized.

In cross-border large transfers, always remain vigilant, prioritize compliant institutions with strong risk controls and good third-party evaluations, and continuously improve your security awareness.

Regulation and Data Security

Role of Regulatory Authorities

When conducting cross-border large transfers, you must understand the central role of regulatory authorities in safeguarding fund safety and data compliance. Regulators require financial companies to strictly comply with Anti-Money Laundering (AML) and Know Your Customer (KYC) regulations and continuously supervise daily operations to ensure activities conform to local laws. You will find that regulators typically require regular reporting and audits to detect potential risks promptly and prevent violations.

- Regulatory authorities promote the establishment of sound internal control systems in financial enterprises, enhancing risk identification and response capabilities.

- When selecting service providers, prioritize those that proactively cooperate with regulators and maintain transparent information disclosure.

- Regulators also require strict data protection measures, especially during cross-border data transfers, to prevent misuse or leakage of user information.

You can review compliance announcements and penalty cases published by regulatory authorities to stay informed of the latest industry developments and enhance your risk prevention awareness.

Data Security and Information Protection

In cross-border fund flows, data security and information protection are equally critical. Financial institutions must use encrypted transmission, role-based access control, and other technical measures to prevent illegal acquisition of sensitive information during transmission and storage. Regulators set clear requirements for approved data protection standards; enterprises must conduct regular security assessments and vulnerability remediation to ensure system security.

- You should verify whether the institution obtains user consent before data transmission and maintains transparency in information disclosure.

- Many compliant institutions collaborate with third-party security firms for penetration testing and security certification to further elevate data protection.

- In practice, information protection is not only a technical issue but also the foundation of compliance and trust. The more importance a service provider places on data security, the stronger the protection for your funds and personal information.

In cross-border large transfers, only by choosing institutions that strictly comply with regulatory requirements and prioritize data security can you minimize the risks of information leakage and financial loss.

When conducting cross-border large-value transfers, selecting institutions with compliance licenses and bank-level risk control systems is the core strategy for preventing AI fraud. You should proactively verify licenses, scrutinize risk control measures, and remain wary of any suspicious information. Only by maintaining constant vigilance and prioritizing legitimate, secure service providers can you effectively protect fund safety and information privacy.

FAQ

How to determine whether a financial institution holds a compliance license?

You can visit the relevant regulatory authority’s official website and search by institution name and license number. Licensed institutions publicly display compliance information on their websites; Hong Kong licensed banks and payment institutions provide transparent public information.

What is the difference between bank-level risk control systems and ordinary risk controls?

Bank-level risk control systems employ multi-factor authentication, real-time transaction monitoring, and AI anti-fraud technology. You receive significantly higher fund safety protection, with risk detection capabilities far exceeding ordinary controls.

What are the latest trends in AI fraud?

You need to watch for emerging AI fraud techniques such as deepfakes, voice cloning, and synthetic identities. These technologies can impersonate executives and trick you into large fund transfers.

How is data security ensured when choosing cross-border payment institutions?

You should select institutions that use encrypted transmission and role-based access management. Compliant institutions undergo regular security assessments to ensure your sensitive information is not leaked or misused.

How can users improve their ability to prevent AI fraud?

You can verify identities through multiple channels, strictly follow payment verification processes, and regularly attend anti-fraud training. You should also pay attention to the institution’s risk control measures and proactively verify compliance information.

*This article is provided for general information purposes and does not constitute legal, tax or other professional advice from BiyaPay or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or warranties, express or implied, as to the accuracy, completeness or timeliness of the contents of this publication.

Related Blogs of

Under the IBM Shock, Which Has the Highest Enterprise IT Budget Exposure: NOW, CRM, ADBE, or ORCL? A Risk Ranking

Which AI Hardware Stocks Benefit More Under IBM’s Warning? Comparing the Sensitivity of NVDA, DELL, MU, and HPE

Where Will IBM Stock Go After Q2 Earnings? Three Scenarios Based on Revenue, Red Hat, and Free Cash Flow

ASML Q2 2026 Earnings Analysis: What Signals Did Orders, EUV Demand, and Full-Year Guidance Release?

Choose Country or Region to Read Local Blog

Contact Us