Massive Data Storage Demand Driven by AI Agents: List of US Stock Tickers in Cloud Storage & Data Centers

Image Source: pexels

The widespread adoption of AI agents is driving continuous growth in global data storage demand. The North American data center market is expanding rapidly at 17.6%, with a current vacancy rate of only 1.6%, demonstrating extremely strong market absorption capacity. Approximately 74.3% of under-construction capacity has already been pre-leased by cloud computing and AI companies. According to forecasts, the global data center market capacity is expected to reach approximately 200 GW by 2030, with AI workloads accounting for nearly 50%. The table below further illustrates changes in market capacity and AI workload share:

| Forecast Year | Market Capacity (GW) | AI Workload Share |

|---|---|---|

| 2030 | ~200 | ~50% |

The global data center market size is projected to reach $347.3 billion in 2026 and grow to $801.5 billion by 2033, with a compound annual growth rate of 12.7%. Cloud storage and data centers, as core segments of the industry chain, have become a key focus for US stock market investors.

Core Key Points

- The proliferation of AI agents is driving rapid growth in global data storage demand, with global data center market capacity expected to reach approximately 200 GW by 2030.

- Enterprises need efficient and reliable storage solutions to cope with the data generation pressure brought by AI agents, ensuring data security and access efficiency.

- The combination of cloud computing and edge computing improves data processing efficiency, meeting the needs for real-time response and low latency, and promoting collaborative development across the industry chain.

- Data center operators enhance operational efficiency through automation and intelligent management, ensuring continuity of AI and cloud computing businesses.

- Investors should focus on the long-term growth potential of the data center and cloud storage sectors, making rational allocations based on technological progress and market changes.

Data Storage Demand Driven by AI Agents

Image Source: unsplash

Data Generation and Storage Pressure

The expanding application of AI agents across industries is significantly accelerating data generation speed. Enterprises deploy AI agents in scenarios such as automated office work, intelligent customer service, and manufacturing, producing vast amounts of structured and unstructured data. This data includes text, images, audio, video, and sensor information, forming enormous data flows. Data storage demand is growing rapidly as a result, and enterprises require efficient and reliable storage solutions to ensure data security and access efficiency.

The scale of data generation far exceeds that of traditional IT systems. AI agents not only process real-time data but also need to retain historical data long-term for model training and business analysis. Data centers and cloud storage platforms have become the core infrastructure supporting this demand. Related companies in the US stock market continue to optimize storage architectures, improving capacity and performance to meet the storage pressure caused by AI agents. Data storage demand has become a key driver of sustained expansion in the data center and cloud storage industries.

Cloud and Edge Computing Power Demand

The demand for computing power from AI agents shows a diversified trend. Cloud computing power provides strong support for large-scale data processing and model training, while edge computing power meets real-time response and low-latency scenarios. The global edge AI market reached $20 billion in 2024 and is expected to grow to $269 billion by 2032. The widespread adoption of 5G networks, the surge in IoT devices, and the demand for real-time data processing across industries are collectively driving rapid expansion of the edge computing market.

Cloud and edge computing architectures continue to evolve to meet the data processing needs of AI agents.

- Hybrid cloud-edge models combine the high computing power of cloud resources with the low-latency characteristics of edge computing, improving overall efficiency.

- Event-driven architectures enable real-time coordination between edge devices and cloud resources, optimizing data flow and processing.

- Agent-centric computing models emphasize dynamic resource allocation based on agent needs, enabling flexible scheduling.

Data center operators and cloud storage service providers are actively deploying hybrid cloud and edge computing power, promoting collaborative development across the industry chain. Related companies in the US stock market continue to meet the computing and data storage demands brought by AI agents through innovative architectures and technological upgrades.

Data Center & Cloud Storage Industry Chain

Image Source: unsplash

Upstream: Compute & Storage Hardware

The upstream segment of data centers covers compute chips, storage devices, and cooling systems. AI technology continues to penetrate data center and edge computing environments, driving automation and technological innovation. Hardware innovations significantly improve energy efficiency and operational maintenance efficiency.

| Innovation Area | Description |

|---|---|

| Data Center Cooling | Liquid cooling and geothermal energy reduce energy consumption; liquid cooling significantly lowers power demand. |

| Chip Power Transmission | Reconfiguring chip power transmission and using optical data transmission to reduce energy consumption. |

| Grid Transmission Technology | Solid-state transformers and advanced transmission technologies improve grid efficiency and support data center expansion. |

79% of data center operators expect rack density to continue increasing under the push of AI. Modern rack designs are being optimized to support high power density and cooling requirements. Larger fans, IoT sensors, and DC power supplies further improve power delivery efficiency for high-density racks.

Midstream: Networking & Connectivity

The midstream segment mainly includes network equipment and connectivity technologies. US-listed companies such as Cisco Systems, Extreme Networks, Arista Networks, and Broadcom dominate this field.

- Cisco Systems invests in data center networking products to meet AI demand and enhance market competitiveness.

- Extreme Networks serves global customers with comprehensive networking solutions.

- Arista Networks holds a position in the market with high-demand products.

- Broadcom stands out as a key supplier for AI computing needs.

Network technologies continue to innovate, with CLOS fabrics, RDMA, adaptive routing, and other architectures providing high bandwidth and low latency for large-scale AI data flows. New technologies such as pluggable optical modules, liquid cooling systems, 800G OSFP modules, and single-mode fiber further improve data transmission efficiency and energy efficiency.

Downstream: Data Center Operations

Data center operators are responsible for daily management and expansion of facilities, ensuring scalability and reliability of AI-driven workloads. High-density colocation configurations meet high-performance computing and AI requirements, with rack designs supporting higher power density and cooling needs. Cooling strategies directly impact uptime and hardware lifespan. AI-driven predictive maintenance maximizes uptime, while automated resource management improves hardware configuration and optimization capabilities. Data center operators effectively address growing data storage demand through these measures.

Support: Energy & Real Estate

Energy and real estate companies provide foundational support for data centers. Data center REITs own and manage data processing facilities, offering power, temperature control, and physical security services, and leasing space to multiple clients. Energy suppliers provide the necessary electricity for data centers to support their high energy consumption operations. Goldman Sachs research shows that US electricity demand will grow by 2.4% from 2022 to 2030, with 0.9 percentage points attributed to data centers. By 2030, data centers are expected to account for 8% of US electricity consumption. US-listed energy and real estate companies are focusing on building new energy infrastructure, integrating advanced technologies such as AI, improving efficiency, and exploring innovative financing and site selection strategies to meet the rapid expansion needs of the industry.

Sub-Sectors & US Stock Tickers

Compute & Storage Hardware Companies

The upstream segment of the US data center industry chain focuses on high-performance compute chips and secure storage hardware. As AI model complexity increases, enterprises have rising requirements for computing power and data security. The decentralized storage hardware market is growing rapidly, particularly in industries with extremely high requirements for sensitive data protection such as finance and healthcare.

- The decentralized cloud storage market is valued at $2.24 billion with a CAGR of 20.5%.

- Data privacy and security vulnerabilities are driving enterprises to adopt more secure storage solutions.

- Innovation in this field provides a solid foundation for continued growth in data storage demand.

Networking & Connectivity Equipment Companies

Networking and connectivity equipment provide assurance for efficient data center operations. US-listed companies such as Cisco Systems, Arista Networks, and Broadcom dominate the global market. These companies continuously launch high-bandwidth, low-latency network products to meet high-speed data transmission needs in AI and big data scenarios.

- Cisco Systems focuses on upgrading data center network architecture to improve overall connectivity efficiency.

- Arista Networks is renowned for high-performance switches and routers, widely used in hyperscale data centers.

- Broadcom continues to innovate in network chips and optical modules, supporting the expansion of AI compute clusters.

Server & Storage Equipment Companies

Servers and storage devices are core assets of data centers. In the US stock market, companies such as IBM, Intel, Supermicro, HPE, and Lenovo provide diverse products and solutions for global data centers. The table below shows major vendors and their core businesses:

| Company Name | Main Products & Services |

|---|---|

| IBM | Cloud data centers, IBM Cloud Object Storage service |

| Intel | Xeon processors, Gaudi AI accelerators |

| Supermicro | Servers, storage arrays, networking products |

| HPE | Secure data centers, HPE Private Cloud AI |

| Lenovo | Servers, supercomputers, data storage systems |

These companies continuously optimize server architectures and storage systems to improve data processing capabilities and energy efficiency, helping data centers address the high-intensity data storage demands brought by AI agents.

Data Center Operators

Data center operators are responsible for daily management, capacity expansion, and maintenance of facilities, ensuring continuity of AI and cloud computing businesses. In the US market, companies such as Equinix and Digital Realty Trust are renowned for their global presence and high-standard services.

- Equinix operates more than 200 data centers across five continents with extensive service coverage.

- Digital Realty Trust focuses on high-density, high-reliability data center facilities to meet the stringent demands of AI and big data enterprises.

These operators improve data center operational efficiency and sustainability through automated operations, intelligent cooling, and energy management.

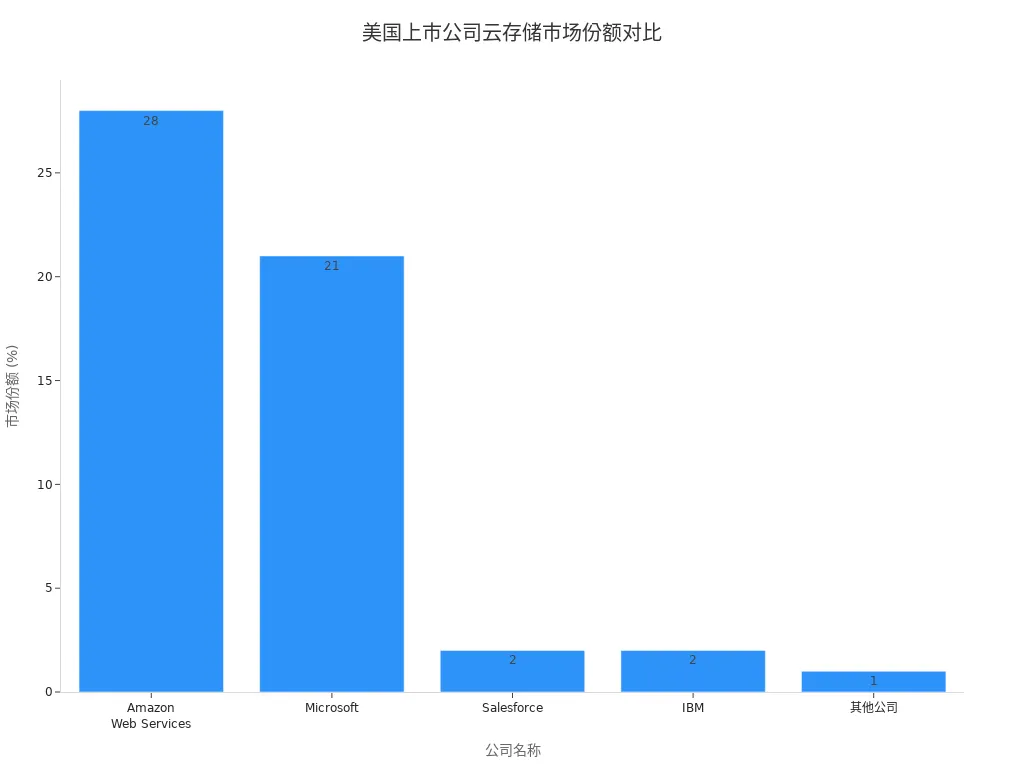

Cloud Storage Service Providers

Cloud storage service providers offer elastic and scalable data storage solutions for enterprises and individual users. The US market is dominated by giants such as Amazon Web Services, Microsoft, Salesforce, and IBM. The table below lists major cloud storage service providers and their market shares:

| Company Name | Market Share | Notes |

|---|---|---|

| Amazon Web Services | 28% | Leading cloud computing provider |

| Microsoft | 21% | Second place, stable market share |

| Salesforce | 2% | One of the major US tech giants |

| IBM | 2% | One of the major US tech giants |

| Huawei | 2% | One of the major Chinese IT giants |

| Tencent | 2% | One of the major Chinese IT giants |

| Other companies | ~1% | Including Akamai, Snowflake, etc. |

Amazon Web Services and Microsoft continue to lead the cloud storage market with strong infrastructure and technological innovation. Enterprises achieve elastic data scaling and high availability through cloud storage services, meeting diverse needs in AI agent and big data scenarios.

Data Center REITs

Data center REITs (Real Estate Investment Trusts) provide investors with channels to participate in data center assets. In the US market, Digital Realty Trust (DLR) and Equinix (EQIX) are representative companies. The table below shows major data center REITs with market cap and dividend yield:

| Name & Ticker | Market Cap (USD) | Dividend Yield | Sector |

|---|---|---|---|

| Digital Realty Trust (DLR) | $62.1B | 2.70% | Specialized REIT |

| Equinix (EQIX) | $95.6B | 1.98% | Specialized REIT |

These REITs provide infrastructure support for AI and cloud computing enterprises through acquisition, development, and operation of high-standard data centers, while delivering stable cash flow and asset appreciation potential for investors.

Energy Suppliers

Energy suppliers play a critical role in the sustainable development of data centers. Major US technology companies are actively signing power purchase agreements to finance renewable energy projects and accelerate the application of carbon-free energy in data centers.

- The industry is accelerating the transition to sustainable and carbon-free energy, promoting the construction of green data centers.

- Some companies are collaborating with nuclear energy startups to plan the reactivation of decommissioned nuclear plants to meet future energy needs.

- Natural gas will remain the primary energy source for data centers until 2030, but nuclear energy is expected to play a larger role in the future.

Innovative initiatives by energy suppliers provide a solid guarantee for the green transformation and long-term development of the data center industry.

Sector Role & Investment Logic

Sector Synergy & Growth Potential

The various segments of the US data center and cloud storage industry chain are closely synergistic, forming strong collective momentum. Upstream hardware innovation drives computing power improvement, midstream network equipment ensures efficient data flow, and downstream operators and REITs provide stable infrastructure. Widespread adoption of cloud storage solutions has become a key support for enterprise digital transformation. The table below presents interpretations of sector synergy and growth potential based on market trend analysis:

| Source | Type | Content |

|---|---|---|

| Data Center Storage Market Growth & Trends 2035 | Market Trend Analysis | The cloud storage segment is expected to expand over the forecast period, primarily driven by increasing adoption of cloud storage solutions in data centers for cost-effectiveness and scalability. As more enterprises continue to prioritize digital transformation, reliance on cloud storage solutions is expected to intensify, solidifying its role in data center architecture. |

| Data Center Market to Reach US$ 801.5 Billion by 2033 | Market Trend Analysis | A strong driver of the data center market is the global shift toward cloud computing and hybrid IT environments. Enterprises across industries are migrating workloads to cloud platforms to improve scalability, operational flexibility, and cost efficiency. This transformation requires robust data center infrastructure capable of supporting distributed computing and real-time analytics. |

The widespread application of AI agents continues to pull demand for data storage, driving synergistic growth across the entire industry chain.

For a theme built around industry-chain analysis, the actual investment step usually comes down to checking tickers, reviewing companies, and only then deciding whether to allocate. You can first use stock information lookup to review basic data and market moves for data center operators, cloud storage names, or related REITs, and then enter the trading portal only after your sector view is clear.

If cross-market fund movement is also part of the process, it is often easier to keep that workflow in one connected path. BiyaPay works as a multi-asset wallet covering cross-border payments, investing, trading, and fund management scenarios, and it operates with relevant compliance registrations in jurisdictions including the United States and New Zealand. For users following the AI infrastructure theme, it is better understood as an execution and fund-connectivity tool after the research step.

Risks & Key Considerations

Investing in the data center and cloud storage sectors requires attention to multiple risks.

- Data center operations are highly dependent on water resources; water shortages or restrictions may impact operational capabilities.

- Unpredictability of water resources due to climate change may lead to new regulations and increased compliance costs.

- In water-stressed areas, conflicts may arise between communities and enterprises, affecting corporate reputation and business continuity.

Data center REITs have some cyclical resistance due to long-term leases, but investors still need to monitor changes in environmental policies and operational resilience.

Future Trend Outlook

The future US data center and cloud storage industry will show diversified development.

- Cloud storage expansion trend is evident; enterprises will continue to adopt cloud storage to improve cost-effectiveness and scalability.

- Demand for backup and recovery solutions is rising, with cybersecurity threats driving increased investment in data protection.

- Edge storage will accelerate deployment due to 5G and IoT development, with micro-modular data centers enhancing local processing capabilities.

- AI-driven autonomous ecosystems (such as autonomous driving and drones) will generate massive data volumes, driving surging demand for low-latency storage solutions.

- Sovereign cloud initiatives are promoting the construction of local data center infrastructure to meet data localization regulatory requirements.

The data center and cloud storage sectors have significant long-term growth potential driven by AI, cloud computing, and data security.

AI agents are driving continued expansion in the data storage industry. The US data center and cloud storage sectors attract diverse capital with significant investment value.

- As of 2024, financial investment in data centers has reached hundreds of billions of dollars, expected to grow to trillions by 2030.

- Funding sources include technology companies, investment funds, sovereign wealth funds, and financial institutions.

All segments of the industry chain develop synergistically, with huge future growth potential. Investors should focus on technological progress and market changes, making rational allocations in relevant sectors based on their own risk preferences.

FAQ

What is the difference between data center REITs and traditional REITs?

Data center REITs focus on data processing facilities serving technology and cloud computing enterprises. Traditional REITs mostly invest in residential, office, or retail properties. The two differ significantly in asset types and tenant structures.

What are the main risks to consider when investing in the data center sector?

Investors need to pay attention to risks such as energy supply, environmental policies, technological updates, and operating costs. Water resource shortages and regulatory changes may affect data center operations and profitability.

How do cloud storage service providers ensure data security?

Cloud storage service providers use multi-layer encryption, access controls, and backup mechanisms to prevent data breaches and loss. Some companies also enhance data security through compliance certifications.

What role do AI agents play in driving the data center industry?

AI agents bring explosive growth in data volume and computing power demand, driving data center capacity expansion and technological upgrades. Operators need to continuously optimize infrastructure to meet emerging business needs.

How do edge computing and cloud computing collaborate in data storage?

Edge computing handles local real-time data processing, while cloud computing provides large-scale storage and analysis capabilities. The two work together to improve data processing efficiency and business response speed.

*This article is provided for general information purposes and does not constitute legal, tax or other professional advice from BiyaPay or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or warranties, express or implied, as to the accuracy, completeness or timeliness of the contents of this publication.

Related Blogs of

How Should SSDs and HDDs Work Together in AI Data Centers? Performance, Capacity, Cost, and Hot vs. Cold Data Compared

What Is the Difference Between HBM3E and HBM4? What Do They Mean for Micron and AI Servers?

What Is the Difference Between DRAM Contract Price and Spot Price? Which Indicator Should Investors Watch?

Why Does AI Compute Growth Drive Storage Demand? The Difference Between Training, Inference, and Data Retention

Choose Country or Region to Read Local Blog

Contact Us

BIYA GLOBAL LLC is registered with the Financial Crimes Enforcement Network (FinCEN), an agency under the U.S. Department of the Treasury, as a Money Services Business (MSB), with registration number 31000218637349, and regulated by the Financial Crimes Enforcement Network (FinCEN).

BIYA GLOBAL LIMITED is a registered Financial Service Provider (FSP) in New Zealand, with registration number FSP1007221, and is also a registered member of the Financial Services Complaints Limited (FSCL), an independent dispute resolution scheme in New Zealand.