- More

- Download

From Web3 to AI: How to Achieve Low-Friction Cross-Market Fund Transfers During Hotspot Shifts?

Image Source: unsplash

In the process of transferring funds from Web3 to AI, efficiency, cost, and security are always the most important considerations. Over the past year, capital flows in the AI system and AI agent markets have continued to grow, with specific data as follows:

| Funding Source | Capital Amount (Billion USD) | Growth Rate |

|---|---|---|

| AI Systems | 1.8 | 26% |

| AI Agents | 1.39 | 9.4% |

You can choose from various low-friction tools and platforms, such as MPChat simplifying the transfer process, QuickNode Streams providing real-time data streams, and Flipside Crypto supporting multi-chain analysis. Each solution applies to different scenarios; it is recommended that you flexibly select based on your own needs to ensure smooth and secure fund transfers.

Core Key Points

- Choosing the right multi-chain wallet can simplify asset management and improve fund flow efficiency.

- Using stablecoins and real-world assets (RWA) can reduce price volatility risks and achieve fast settlement.

- Cross-chain bridge mechanisms provide technical support for asset transfers; selecting secure bridging protocols is crucial.

- AI agents and automation tools can enhance the intelligence level of fund transfers and reduce manual intervention.

- Pay attention to compliance and security risks, and regularly review processes to ensure fund safety and legality.

Core Methods for Fund Transfers from Web3 to AI

Image Source: unsplash

Multi-Chain Wallets and Asset Management

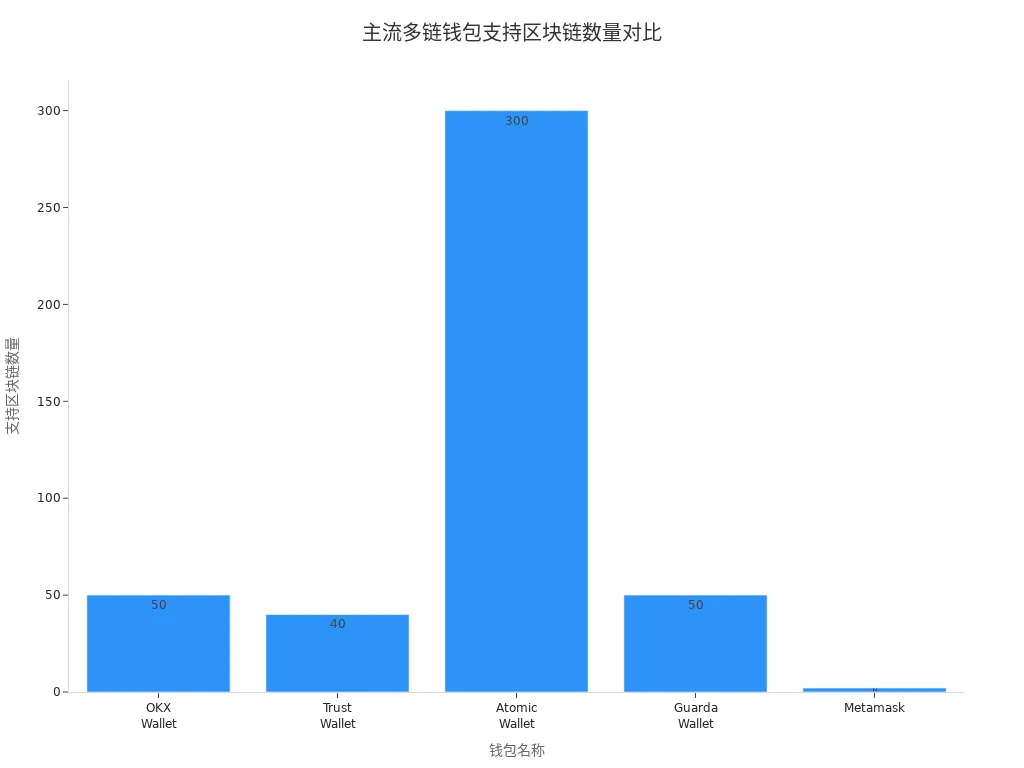

In the process of transferring funds from Web3 to AI, you first need to address the multi-chain compatibility issue in asset management. Multi-chain wallets provide you with a unified asset view and operation entry, greatly simplifying cross-chain asset management processes. You can manage and transfer various blockchain assets through mainstream multi-chain wallets such as BiyaPay, OKX Wallet, Trust Wallet, Atomic Wallet, Guarda Wallet, and Metamask. BiyaPay supports multi-chain asset storage, transfers, and exchanges, making it suitable for Chinese-speaking users who need efficient multi-chain asset management. You do not need to frequently switch wallet applications and can complete asset viewing, transfers, exchanges, and other operations within a single interface, improving fund flow efficiency.

| Wallet Name | Number of Supported Blockchains | Main Features |

|---|---|---|

| BiyaPay | 20+ | Supports mainstream public chains and stablecoins, integrates various asset management and transfer functions, suitable for cross-market fund flow needs. |

| OKX Wallet | 50 | Supports 1,200 BRC-20 tokens, single transaction up to 30 BTC transfers, suitable for Ordinals users. |

| Trust Wallet | 40+ | Compatible with 160,000+ assets, supports ERC20, BEP2, and ERC721 tokens. |

| Atomic Wallet | 300+ | Provides a variety of cryptocurrencies, suitable for users seeking diversified investments. |

| Guarda Wallet | 50+ | Highly adaptable, regularly adds new assets, supports thousands of tokens. |

| Metamask | Multiple | Designed for Ethereum and other Ethereum-compatible networks, supports various ERC-20 tokens. |

When choosing a multi-chain wallet, you need to weigh its advantages and disadvantages:

| Advantages | Disadvantages |

|---|---|

| Simplified asset management | Higher transaction fees |

| Convenience and efficiency | Limited availability |

| Enhanced security measures | Management complexity |

| Cost-effective transactions | Increased security risks |

| User-friendly interface | OTA update risks |

| Access to a wide range of assets | N/A |

| Integration with other services | N/A |

You can further lower the operational threshold through account abstraction (smart contract wallets) and embedded wallets (Wallet-as-a-Service). For example, BiyaPay supports password verification without seed phrases and social recovery, improving security and usability. In Web3 to AI fund flows, you can achieve instant payments, reducing fees and latency, meeting the needs of high-frequency trading and rapid asset switching.

Stablecoins and RWA Settlement Layer

When transferring funds from Web3 to AI, stablecoins and the RWA (Real World Asset) settlement layer play a key hub role. Stablecoins are not only the connecting link for all other trends but also the foundation for cross-chain and cross-system settlement. You can use mainstream stablecoins such as USDT and USDC for asset transfers, avoiding cryptocurrency price volatility risks and achieving efficient settlement. BiyaPay supports the deposit, withdrawal, and transfer of mainstream stablecoins, helping you flexibly allocate funds between different markets.

In scenarios such as AI agent payment services, prediction market settlement, and lending market collateral, stablecoins have become an indispensable monetary foundation. You can directly settle AI service fees with stablecoins through platforms like BiyaPay, improving fund flow efficiency and reducing the high fees and latency of traditional payment systems.

The RWA settlement layer represents a new trend in Web3 to AI fund flows. You can achieve seamless docking with real-world assets through tokenized assets such as XAU₮ (Tether Gold), BUIDL (BlackRock), USYC (Circle & Hashnote), and RLUSD (Ripple). For example, BlackRock's BUIDL Fund is based on Ethereum, managing over $2.5 billion in tokenized money market funds, supporting 24/7 on-chain share transfers and redemptions. When allocating funds in the U.S. market, you can achieve compliant and efficient cross-market settlement through these RWA products.

When choosing stablecoin and RWA products, you should focus on their compliance, liquidity, and settlement efficiency. Platforms like BiyaPay have integrated various stablecoins and RWA assets, suitable for professional users who need high-frequency settlement and multi-market fund allocation.

Cross-Chain Bridge Mechanisms

In the process of transferring funds from Web3 to AI, cross-chain bridge mechanisms provide the technical foundation for asset cross-chain transfers. Mainstream cross-chain bridges adopt mechanisms such as lock-and-mint, burn-and-mint, liquidity pools, and atomic swaps. You can lock the original asset (such as ETH) in the source chain smart contract, mint an equivalent wrapped asset (such as wETH) on the target chain, or directly withdraw equivalent assets on the target chain through liquidity pools, achieving seamless cross-chain asset transfers.

When choosing a cross-chain bridge, you need to focus on its security and cost. Mainstream cross-chain bridges face security risks such as smart contract vulnerabilities, validator collusion, key management issues, oracle manipulation, and economic attacks. You should prioritize bridging protocols that have been audited and feature multiple security mechanisms. You also need to consider protocol fees (typically 0.05%-0.15%), gas fees, slippage, and other transaction costs, and reasonably plan the fund transfer path.

BiyaPay has integrated cross-chain bridge services for multiple mainstream public chains, supporting one-click cross-chain transfers, suitable for users who need high-frequency, low-friction fund flows. You can achieve rapid switching of multi-chain assets through BiyaPay, improving fund utilization efficiency and reducing operational complexity.

AI Agents and Automation Tools

In Web3 to AI fund transfers, AI agents and automation tools are becoming new engines for improving efficiency and reducing friction. AI agents can automate trading, liquidity management, compliance checks, and data analysis, reducing manual intervention and enhancing the intelligence level of fund flows. You can deploy AI agents through platforms such as Fetch.ai and BiyaPay to automatically execute tasks like cross-chain transfers, asset rebalancing, and risk monitoring.

| Source of Evidence | Evidence Content |

|---|---|

| Fetch.ai | Allows cryptocurrency companies to simplify operations, automate trading, optimize blockchain transactions, and reduce manual intervention. Its agents can self-manage liquidity pools, execute decentralized finance techniques, and securely share data. |

| IDC MarketScape | AI-driven financial systems are no longer just automation tools; they are becoming central command centers for liquidity, risk, and cash forecasting, driving real-time visibility into global banking relationships. |

| Ledger Academy | AI agents can automatically execute trades based on real-time market data, analyze vast amounts of data from blockchains and social media, adjust portfolios to keep up with market trends, and interact with other blockchain services. |

In asset management, you can use AI automation tools to replace tedious manual operations, achieving 24/7 portfolio management and risk control. AI algorithms can automate trade reconciliation, compliance checks, and data processing, reducing operational workload and human errors, and accelerating reporting and auditing processes. You can combine AI agents and automation tools through platforms like BiyaPay to build dynamic risk management and forward-looking investment decision systems, enhancing the intelligence and security of Web3 to AI fund flows.

Main Barriers to Cross-Market Fund Transfers

Web3 Friction and User Experience

In the process of transferring funds from Web3 to AI, you often encounter complex operational processes and user experience barriers. You need to install browser extensions, create wallets, save seed phrases, purchase or transfer cryptocurrency to fund the wallet. You also need to understand the differences between various chains, tokens, smart contracts, and fees. When approving transactions, multiple windows pop up, easily causing confusion. For new users, these steps are overly cumbersome, and any error in any step may cause you to abandon the attempt. When transferring assets on mainstream blockchains like Ethereum, you also need to find suitable bridging tools, connect wallets, approve tokens, pay fees, wait for confirmation, switch networks, reconnect, and check asset status. Each network switch may lead to additional fees and time waste, increasing operational difficulty. Web3 products operating in multi-chain environments are prone to chain switching errors or transaction failures, lacking clear instructions and visual cues, making it difficult for new users to understand the reasons for failure.

Fees and Time Costs

When transferring funds between different markets, fees and time costs are barriers that cannot be ignored. The following table compares the fees and time costs of mainstream payment methods:

| Payment Method | Fees | Time Cost |

|---|---|---|

| Web3 Payments | Usually low fees, mainly depending on blockchain network transaction fees (gas fees) | Usually completed within a few minutes |

| Interbank Payments | Usually high fees, caused by multiple intermediaries | Processing time usually takes several days |

| Third-Party Payments | Fixed fees, usually including a percentage of the transaction amount | Usually completed within a few days or instantly |

In Web3 to AI fund flows, although blockchain payments have lower fees and faster speeds, gas fees may surge significantly during peak periods, affecting fund allocation efficiency. Interbank payments and third-party payments involve high fees and longer arrival cycles, making it difficult to meet high-frequency and agile fund transfer needs.

What often shapes the real cross-market experience is not whether one step is fast, but whether you can see conversion costs and transfer routes clearly before moving funds. You can first use the exchange rate comparison tool to estimate switching costs across currencies, then use the official remittance page to confirm the actual transfer path, so friction does not rise further when market themes rotate quickly.

This kind of process is easier when handled within one connected fund path. BiyaPay works as a multi-asset wallet covering cross-border payments, investing, trading, and fund management scenarios, and it operates with relevant compliance registrations in jurisdictions including the United States and New Zealand. For users moving capital between Web3 and AI themes, it is better understood as a settlement and routing tool rather than a substitute for investment judgment.

Compliance and Security Risks

When transferring funds across markets, you must face complex compliance and security risks. Anti-money laundering (AML) compliance is a basic requirement for financial services. When handling high-frequency cross-border transactions, you need to conduct real-time screening of clients and recipients to prevent criminals from using small amounts or multi-country transfers to conceal fund sources. You also need to comply with multi-country regulations, including anti-money laundering laws, counter-terrorism financing measures, and sanctions screening. Compliance failures may lead to huge fines and reputational damage, seriously affecting business operations. In actual operations, you also need to strengthen customer due diligence to ensure no transfers involving sanctioned parties are processed, reducing legal liability and reputational risks.

| Risk Type | Description |

|---|---|

| Anti-Money Laundering Compliance | Cross-border payments face high AML risks, requiring real-time screening of clients and recipients. |

| Regulatory Compliance Complexity | Need to comply with multi-country regulations, with constantly changing compliance requirements, increasing compliance burden. |

| Fines and Reputational Damage | Compliance failures may lead to huge fines and reputational damage, affecting business operations. |

| Customer Due Diligence | Need to strengthen real-time screening of clients and recipients to prevent processing transfers involving sanctioned parties. |

| Merchant Behavior Monitoring | Need to be vigilant about suspicious behavior of merchant clients to prevent money laundering through fake online stores. |

Asset Compatibility and Liquidity

When transferring funds from Web3 to AI, asset compatibility and liquidity issues are equally prominent. Regulatory requirements and asset compatibility issues introduce complexities such as collateral management, security procedures, and digital asset classification. These factors directly affect the speed, efficiency, and legality of asset transfers. For example, the U.S. CFTC stipulates that customer funds are not allowed to be invested in digital and tokenized assets, limiting the flexibility of cross-market transfers.

When using tokenized assets, you also need to pay attention to cybersecurity and smart contract risks, which may affect the safe transfer of assets. Insufficient asset compatibility will cause some assets to be unable to circulate in the target market, reducing fund utilization efficiency and increasing management difficulty.

Detailed Explanation of Low-Friction Transfer Solutions

Image Source: unsplash

Multi-Chain Wallet Solutions

You can achieve efficient management of assets across different blockchains through multi-chain wallets. BiyaPay provides Chinese-speaking users with asset management capabilities covering Bitcoin, Ethereum/EVM, Solana, and major L2s. You manage multi-chain assets on a single interface, reducing fragmentation. The intuitive network switching function ensures you always know the current active network before signing, avoiding common erroneous transfers. BiyaPay adopts a secure self-custody design, supporting robust seed phrase backup processes and readable transaction prompts to maximize asset security. You can also smoothly connect to DeFi, NFT, and other on-chain applications through the built-in dApp browser.

| Core Feature | Key Element | Impact |

|---|---|---|

| Correct Chain Coverage | Supports mainstream public chains and L2s | Multi-ecosystem availability |

| Clear Network Switching | Active network always visible | Prevents erroneous network transfers |

| Unified Portfolio View | Cross-chain aggregated balances and NFTs | Improves asset management efficiency |

| Secure Self-Custody | Strong seed phrase backup + readable transaction prompts | Minimizes user errors |

| Seamless dApp Connection | Built-in browser or adapter | Smooth interaction with on-chain applications |

Stablecoin and RWA Applications

When transferring funds from Web3 to AI, stablecoins and RWA assets greatly improve settlement efficiency and security. BiyaPay supports mainstream stablecoins such as USDT and USDC, helping you avoid price volatility risks and achieve second-level settlement. You can access RWA assets such as XAU₮ and BUIDL through BiyaPay, obtaining global 24/7 liquidity. Tokenized assets allow you to fractionalize ownership and expand the investment base. Traditional securities settlement requires T+2 days, while tokenized assets complete settlement in seconds, improving fund allocation flexibility.

| Mechanism | Description |

|---|---|

| Settlement Efficiency | Tokenized assets complete settlement in seconds |

| Global Access | Any compliant wallet user can access |

| Fractional Ownership | Private credit trades can be fractionalized, expanding investor base |

| 24/7 Liquidity | Blockchain markets are not limited by closing hours |

Cross-Chain Protocols and Bridges

You can use mainstream cross-chain protocols to achieve low-friction asset transfers between different chains. BiyaPay integrates protocols such as Across, Synapse, and Stargate, supporting intent-driven systems, liquidity pool models, and unified liquidity. Across Protocol completes transactions in only 2-4 seconds, with low fees and strong security. Synapse supports 20+ chains, with liquidity pools enabling instant swaps and fee structures saving up to 80%. Stargate Finance provides deep liquidity pools across 40+ chains, with transactions as low as 0.06% fixed fees. You need to pay attention to supported asset types and slippage risks, and choose protocols reasonably.

| Protocol Name | Advantages | Disadvantages |

|---|---|---|

| Across Protocol | Fast transactions, low fees, strong security | Limited chain support, relatively new technology |

| Synapse Protocol | Multi-chain support, instant swaps, fee savings | Slippage on large transfers, complex interface |

| Stargate Finance | Deep liquidity, unified liquidity, low fees | Higher fees for small transactions, complex routing |

AI Automation and UCP

You can enhance the intelligence level of fund transfers through AI automation tools and UCP systems. BiyaPay has integrated AI agents, supporting automatic management of financial transactions, risk monitoring, and compliance checks. Coinbase's Agentic Wallets allow AI agents to autonomously manage transactions, simplifying operations. The UCP system, based on the x402 protocol, has processed over 50 million transactions, supporting machine-to-machine payments and programmatic resource access. AI can also be used to monitor ERC-20 token transactions, ensuring fund security. In Web3 to AI fund flows, you can use AI automation and UCP to achieve 24/7, low-friction, high-security fund allocation.

| Type | Content |

|---|---|

| AI Tools | AI agents autonomously manage financial transactions, simplifying operations |

| UCP Applications | Supports machine-to-machine payments and programmatic resource access |

| Security Monitoring | AI monitors ERC-20 transactions, ensuring fund security |

Practical Recommendations and Selection Guide

Key Points for Scheme Selection

When choosing cross-market fund transfer solutions, you should focus on asset type, liquidity, compliance, and operational convenience. Multi-chain wallets are suitable for users who need to manage multiple blockchain assets, while stablecoins and RWA products are suitable for high-frequency settlement and global liquidity needs. Cross-chain protocols and AI automation tools are suitable for scenarios pursuing efficiency and intelligent management. You can refer to the table below to quickly compare the applicable scenarios of different solutions:

| Scheme Type | Applicable Scenarios | Main Advantages |

|---|---|---|

| Multi-Chain Wallet | Multi-chain asset management, fragmented asset integration | Easy operation, unified asset view |

| Stablecoins and RWA | High-frequency settlement, global liquidity | Avoids volatility, high settlement efficiency |

| Cross-Chain Protocols | Asset cross-chain transfers, liquidity optimization | Low fees, fast speed |

| AI Automation Tools | Intelligent management, risk monitoring | Automation, reduces manual intervention |

You need to flexibly combine different tools based on your own fund size, transaction frequency, and compliance requirements to improve fund transfer efficiency and security.

Risk Control Recommendations

In the process of cross-market fund transfers, you must attach great importance to risk control. You can use integrated platforms to integrate KYC, sanctions, and PEP screening, improve data quality, and adopt the ISO 20022 standard. You should strengthen governance, documentation, and audit trails, conduct regular compliance reviews, and establish risk management systems. You need to continuously monitor cross-border risks, identify abnormal routing and high-risk regions, and apply risk-based segmented management. You should also strengthen legal awareness, understand relevant foreign exchange laws and regulations, and ensure all transactions are legal, reliable, and stable. You can use advanced analytics techniques to improve detection capabilities and proactively identify and address legal risks related to fund outflows.

In actual operations, it is recommended to regularly review compliance processes, promptly update risk management strategies, and ensure fund safety and legal compliance.

Common Pitfalls Reminder

When transferring funds between Web3 and AI markets, you are prone to operational errors and risk blind spots. Common pitfalls include: lack of control in decentralized finance allocations, inability to withdraw payments; smart contract configuration errors leading to severe undervaluation of asset value, causing significant financial losses; over-reliance on artificial intelligence without sufficient verification, leading to fund losses. Some users pay high fees due to operational errors or even suspect involvement in money laundering. NFT collectors lose funds due to inputting wrong prices. You also need to be vigilant about security risks from unreviewed AI-generated code.

- During operations, you should strengthen the review of smart contracts and AI tools, avoid over-reliance on automation, and ensure every transaction is fully verified.

- You need to carefully check transaction amounts and fees to prevent fund losses due to input errors.

- You should regularly review fund flow processes and promptly detect and correct potential risks.

Trend Outlook and Risk Alerts

PayFi and New Settlement Layers

When transferring funds across markets, PayFi and new settlement layers are reshaping the payment ecosystem. Regulation is gradually becoming clearer, with Europe's MiCA, Hong Kong's VASP regime, and the U.S. stablecoin bill providing clear frameworks for on-chain payments. Banks and payment service providers have higher requirements for instant settlement and deterministic finality, with platforms like Concordium achieving two-second block finality and integrating identity layers. Tokenization of real-world assets has become a new trend; you can process assets such as government bonds, carbon credits, and trade invoices through on-chain payment primitives, achieving micro-allocation and real-time yield streams. The table below summarizes the main trends:

| Trend | Description |

|---|---|

| Regulatory Clarity | Europe, Hong Kong, and the U.S. have introduced regulatory frameworks for on-chain payments |

| Institutional Integration | Banks and payment providers require instant settlement and identity authentication |

| Asset Tokenization | Government bonds, carbon credits, and other assets achieve on-chain micro-allocation and real-time yield streams |

Integration of Traditional Financial Products

In the fund transfer process, the integration of traditional financial products with Web3 and AI solutions is accelerating. Hybrid payment services such as FujiPay support seamless payments between fiat and digital currencies, and Fuji Card connects Web3 wallets, accepted globally, suitable for cross-border fund allocation. Large financial institutions are exploring distributed ledger technology to promote the distribution of central bank digital currencies. You can refer to the table below to understand the main products:

| Product Name | Description | Type |

|---|---|---|

| FujiPay | Supports seamless payments between fiat and digital currencies | Hybrid service |

| Fuji Card | Globally accepted physical card, connects Web3 wallets, supports cross-border payments | Combination of traditional finance and Web3 |

| Hitachi and Spydra Collaboration | Promotes the application of distributed ledger technology in central bank digital currency distribution | Web3 financial application |

Market Regulatory Changes

When transferring funds in Web3 and AI markets, you need to pay attention to the latest regulatory changes. The U.S. requires all entities using AI for automated trading to register algorithmic systems with the SEC or CFTC, submitting training data, decision logic, backtest results, and risk assessments. AI trading systems must deploy real-time monitoring mechanisms, automatically pause abnormal behavior, and configure mandatory "circuit breakers" for human intervention. In actual operations, you need to focus on the following regulatory points:

- Algorithm registration system requires submission of detailed data and risk assessments

- Real-time monitoring mechanisms automatically pause abnormal transactions

- Mandatory "circuit breakers" ensure human intervention capability

- AI algorithms identify hidden patterns through anomaly detection, graph analysis, and behavior analysis

- With the popularity of DeFi and DEX, market manipulation detection has become a focus

In the fund transfer process, you need to continuously monitor regulatory developments, promptly adjust compliance strategies, and ensure fund safety and legality.

In the process of transferring funds from Web3 to AI, priority should be given to low-friction, high-efficiency tools and solutions. To ensure fund safety and compliance, it is recommended that you focus on the following risk management elements:

- Risk avoidance

- Risk transfer

- Risk mitigation

- Continuous monitoring

- Business continuity planning

- Agile risk management

Risk management is not a one-time task. You need to regularly evaluate and adjust strategies, promptly respond to market and technological changes, and ensure that fund flows remain safe and efficient at all times.

FAQ

How to choose the optimal tool when transferring funds from Web3 to the AI market?

You should prioritize multi-chain wallets, stablecoins, RWA products, or AI automation tools based on asset type, liquidity needs, and compliance requirements, and flexibly combine them according to actual scenarios.

Is cross-chain bridge transfer safe? How to reduce risks?

You need to choose mainstream cross-chain bridges that have undergone security audits and feature multiple verification mechanisms. It is recommended to transfer in batches, avoid large single transactions, and regularly follow protocol security announcements.

What are the advantages of stablecoin and RWA asset settlement?

You can achieve second-level settlement, global liquidity, and price stability through stablecoins and RWA assets, significantly improving fund allocation efficiency and reducing latency and costs of traditional financial systems.

What roles can AI agents play in fund transfers?

You can use AI agents to automatically execute cross-chain transfers, risk monitoring, and compliance checks, reducing manual intervention and improving the intelligence and security of fund flows.

How to address compliance challenges in cross-market fund transfers?

You should continuously monitor regulatory developments in major markets such as the U.S. and Hong Kong, adopt integrated KYC and anti-money laundering screening tools, regularly update compliance strategies, and ensure fund safety and legality.

*This article is provided for general information purposes and does not constitute legal, tax or other professional advice from BiyaPay or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or warranties, express or implied, as to the accuracy, completeness or timeliness of the contents of this publication.

Related Blogs of

Under the IBM Shock, Which Has the Highest Enterprise IT Budget Exposure: NOW, CRM, ADBE, or ORCL? A Risk Ranking

Which AI Hardware Stocks Benefit More Under IBM’s Warning? Comparing the Sensitivity of NVDA, DELL, MU, and HPE

JPM, BAC, GS, MS, and Citi: Which Bank Stock Is More Worth Buying? A Comparison of Valuation, Dividends, and Business Structure

Is ASML’s Valuation Overextended After Earnings? Backlog and 2026 Guidance Risks

Choose Country or Region to Read Local Blog

Contact Us