- More

- Download

Missed Final Property Payment Due to Withdrawal Failure? Comparison of Large Withdrawal Times and Promised Arrival Cycles Across Compliant Channels

Image Source: unsplash

When paying the final property payment, timely arrival of funds is critical. If a withdrawal failure prevents the final payment from being made on schedule, you may miss your ideal property or even face breach of contract liability. Many homebuyers have had their transactions delayed because they did not choose compliant channels or fully understand promised arrival cycles. You need to attach great importance to every large-amount withdrawal and arrival process, ensuring each step is compliant and transparent, to effectively avoid risks caused by fund delays.

Key Takeaways

- Ensure account information is accurate to avoid withdrawal failures due to errors. Double-check name, account number, and bank details; update identification documents promptly.

- Prepare proof of fund sources in advance to enable smooth bank processing of large withdrawals. Have valid identification and documents proving legitimate needs ready.

- Understand the bank’s compliance review standards and prepare complete supporting documents to reduce withdrawal failure risk and ensure timely fund arrival.

- Choose appropriate withdrawal channels considering speed and compliance. Bank transfers suit large payments; third-party platforms suit fast arrivals.

- Plan withdrawal timing in advance and withdraw in batches to lower risk, ensuring the final property payment is made on time and avoiding breach liability.

Causes and Risks of Withdrawal Failure

Image Source: unsplash

When paying the final property payment, smooth withdrawal and timely arrival of funds are key to transaction success. Withdrawal failure not only affects transaction progress but may also bring legal and financial risks. You need to understand common causes of withdrawal failure and prepare relevant materials in advance to effectively mitigate risks.

Account Information Errors

Account information errors are a common cause of withdrawal failure. If the recipient name, account number, or bank details are incorrect when filling in the receiving account, the bank will reject the withdrawal request. To reduce such errors, you can take the following measures:

- Complete all personal profile sections to ensure information is accurate.

- Verify email and phone immediately after account creation to keep contact methods active.

- Perform withdrawals from the same device to build a trust record.

- Set a reminder 30 days before ID expiration to update documents promptly.

These steps help maintain account health and reduce the probability of withdrawal failure.

Unclear Source of Funds

When processing large withdrawals, banks require proof of fund sources. If you cannot provide clear and legitimate proof, the bank will suspend or reject the withdrawal. You need to prepare the following documents:

- Valid personal identification documents.

- Documents proving legitimate needs, such as tuition proof, medical certificates, etc.

Preparing these materials in advance can speed up the review process and avoid withdrawal failure due to unclear fund sources.

Compliance Review Not Passed

Mainland China and Hong Kong licensed banks must conduct strict compliance reviews when handling large withdrawals. You need to understand the main review standards of banks:

- Financial institutions must monitor, record, and report significant cash transactions.

- Banks verify the purpose of large withdrawals to prevent financial crime and fraud.

- Banks inquire about withdrawal reasons to protect customers from exploitation or coercion.

- Banks must maintain transparent documentation to meet internal risk management and external audit requirements.

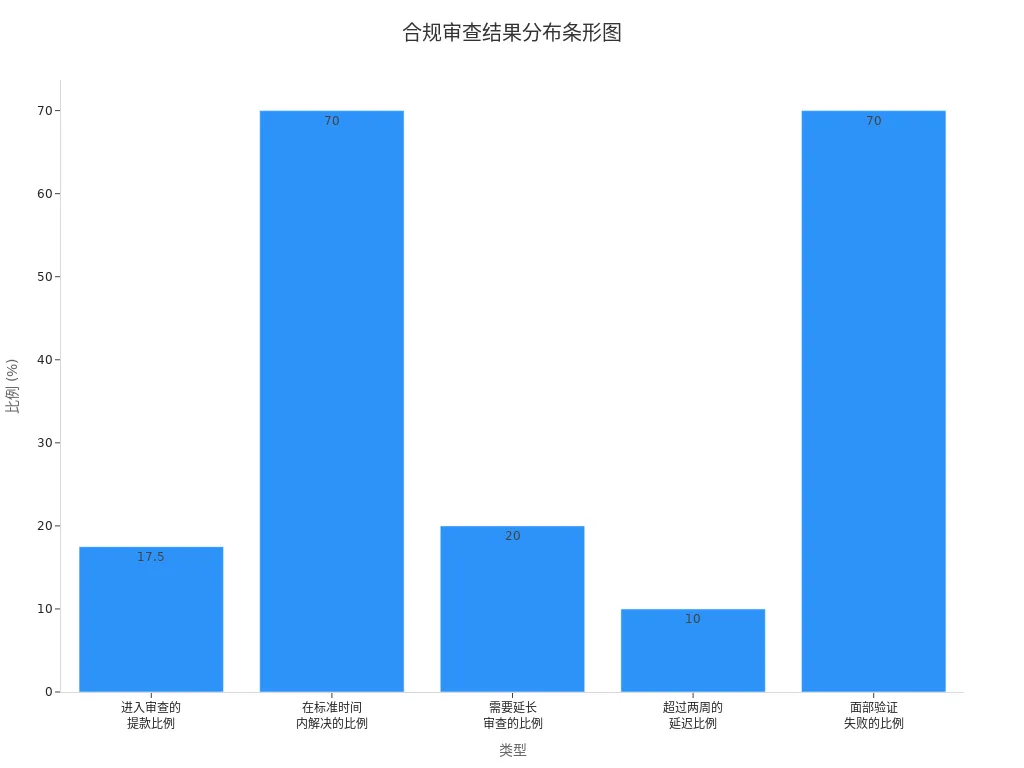

Compliance reviews may cause some withdrawals to enter extended review processes. The table below shows the proportion of different compliance review outcomes:

| Type | Percentage |

|---|---|

| Proportion of withdrawals entering review | 15-20% |

| Proportion resolved within standard time | 70% |

| Proportion requiring extended review | 20% |

| Proportion delayed over two weeks | 10% |

| Proportion of facial verification failures | 70% |

When preparing large withdrawals, you need to understand the bank’s compliance requirements in advance, prepare complete supporting documents, and reduce the risk of withdrawal failure.

System Failures and Operational Errors

System failures and operational errors can also lead to withdrawal failure. If you encounter unstable networks, system maintenance, or non-standard operations during the process, funds may not arrive on time. You can adopt the following best practices:

- Optimize UTXO transactions, using input selection strategies and batch processing to reduce fees.

- Use multiple withdrawal wallets to distribute transactions and increase throughput.

- Implement automated withdrawal processes using batch smart contracts on Ethereum and EVM networks.

- Ensure automated, highly available signing components run continuously.

- Define strict security controls, manage multiple withdrawal wallets, and separate duties of initiators, signers, and authorizers.

These measures can reduce risks from operational errors and system failures, safeguarding fund security.

Impact on Final Property Payment

Withdrawal failure directly affects the payment of the final property amount. You may miss the closing date due to fund delays, resulting in breach of contract. Common legal and financial consequences include:

- Buyers may seek monetary damages for breach, including temporary housing, extra moving costs, and the difference if the buyer must purchase a similar property at a higher price.

- Buyers can claim compensation from the seller for losses caused by breach, such as home inspection, appraisal, survey, and title check fees.

- If the contract includes a penalty clause, the buyer can claim compensation according to that clause.

- Before taking legal action, it is recommended to negotiate or mediate a new closing date through civil means to avoid prolonged legal disputes.

In property transactions, you must plan withdrawal timing in advance, prepare complete compliance materials, and choose reliable channels to effectively avoid risks from withdrawal failure and fund delays.

Tip: Preparing relevant documents and materials in advance and choosing compliant channels can significantly reduce withdrawal failure risk and ensure smooth property transactions.

Compliant Channel Methods

When handling large-amount withdrawals, you can choose from multiple compliant channels. Different channels suit different scenarios, with varying processes and arrival speeds. Understanding these methods helps you make the optimal choice based on actual needs.

Bank Counter and Online Banking

You can handle large withdrawals through bank counters or online banking. Bank counters are suitable for users needing face-to-face service or having special requirements. You need to bring valid identification and relevant supporting documents, fill out a withdrawal application form, and bank staff will assist you in completing the process. Online banking provides a more convenient online operation experience, suitable for daily transfers and fund allocation.

In China, ATM networks are widely covered, making withdrawals relatively easy. You can refer to the following suggestions:

- Carry several cards from different networks (e.g., Visa, Mastercard) in case some ATMs do not support certain cards.

- ATMs can be found at airports, major hotels, department stores, and bank branches.

- Single ATM withdrawal limits are usually low; consider multiple withdrawals.

- Your home bank may charge foreign exchange transaction fees and ATM withdrawal fees — confirm in advance before travel.

Bank counters and online banking are suitable for scenarios requiring high security and compliance, especially common in large transactions such as final property payments.

International Wire Transfer

International wire transfers are suitable for cross-border large-amount fund transfers. You need to provide detailed recipient information, including name, account number, receiving bank SWIFT code, etc. During processing, the bank conducts compliance review to ensure legitimate source and use of funds. International wire transfers generally arrive within 1-3 business days, though in some cases transit banks or compliance reviews may extend the time. Before initiating, confirm all information with the recipient in advance to avoid delays due to incorrect details.

Third-Party Payment Platforms

Third-party payment platforms offer flexible withdrawal options, suitable for scenarios needing fast arrival or multi-currency settlement. Common platforms such as PayPal, Revolut, Payoneer, etc., support global fund transfers. Refer to the table below to understand the arrival speed and fees of different platforms:

| Method | Speed | Fee |

|---|---|---|

| PayPal | Processed within one day | 2.5% |

| Revolut | Up to one business day | N/A |

| Deel Card | Instant withdrawal | N/A |

| Instant Card Transfer | Instant payment | 2.5% |

| Payoneer | Fast and secure transactions | 1% |

Third-party payment platforms are suitable for users needing high efficiency, low barriers, and multi-currency support, and are widely used in global payments, remittances, and digital asset conversions.

Other Common Compliant Methods

You can also choose compliant channels such as global payment and remittance services, fiat-to-crypto conversions, USDT-to-USD/HKD exchanges, etc. These methods usually rely on licensed financial institutions or compliant platforms and are suitable for users with special fund needs or requiring diversified asset allocation. When choosing, focus on the platform’s compliance qualifications, fund security measures, and promised arrival cycles to ensure smooth fund arrival and meet large payment needs such as final property payments.

If the funds involve cross-border transfer, or a sequence of conversion first and property payment later, it is worth checking whether a platform places remittance services and fund transfer within the same workflow. This can reduce delays caused by repeated confirmation across multiple intermediaries. A multi-asset wallet such as the BiyaPay website typically handles cross-border payments, asset conversion, and account management within one system, which makes it easier to review the transfer path and expected arrival timing in advance.

At the same time, compliance background and record retention should also be part of the evaluation. BiyaPay operates under frameworks such as U.S. MSB and New Zealand FSP, which makes it a reasonable reference when large transfers involve both remittance and asset conversion; if you need an extra timing buffer, you can also review its event center for any process-related notices that may affect fund planning.

Arrival Cycle Comparison

Image Source: pexels

When selecting large-amount withdrawal channels, the arrival cycle directly affects fund security and transaction timeliness. Different channels have varying arrival speeds and promises. Understanding this information helps you plan fund arrangements rationally and reduce risks from withdrawal failure.

Bank Transfer Arrival Time

Bank transfers are the preferred method for many Chinese-speaking users when paying final property amounts. When handling large transfers through Hong Kong licensed banks, you usually need to submit complete identity and fund proof materials. After compliance review passes, the bank arranges the fund transfer.

Data shows that the average processing time for SWIFT payments is 27 hours, 6 minutes, and 5 seconds. You have a 64.3% chance of receiving funds within 24 hours. This indicates that bank transfer arrival is faster than many people imagine, but you should still reserve at least 1-2 business days to account for possible delays.

In actual operations, pay attention to the following points:

- Conduct transfers on business days, avoiding holidays and weekends.

- Confirm recipient account information is correct to reduce withdrawal failure due to errors.

- Communicate with the bank promptly to track transfer progress.

International Wire Transfer Arrival Cycle

International wire transfers are suitable for cross-border large-amount fund transfers. When using international wire transfers, banks settle funds through the SWIFT system. Generally, international wire transfers arrive within 1-3 business days. In some cases, transit banks or compliance reviews may extend the time to 5 business days.

When initiating international wire transfers, prepare recipient information, SWIFT code, and purpose explanation in advance. Some banks may require additional proof of fund sources. You can improve arrival efficiency in the following ways:

- Confirm all information with the recipient in advance.

- Submit wire transfer applications during bank business hours.

- Pay attention to the bank’s real-time exchange rates and fee policies.

Although international wire transfers have a longer arrival cycle, they are suitable for cross-border large final property payment scenarios.

Third-Party Payment Arrival Speed

Third-party payment platforms provide more flexible withdrawal options. When using platforms such as PayPal, Revolut, Payoneer, etc., funds usually arrive within 1 business day, and some products support instant arrival.

When choosing third-party payments, pay attention to the platform’s compliance qualifications and fund security measures. Some platforms support multi-currency settlement, suitable for users needing fast fund allocation or multi-currency conversion.

The table below compares arrival speeds and fees of common third-party payment methods:

| Payment Method | Arrival Speed | Fee |

|---|---|---|

| PayPal | Within 1 day | 2.5% |

| Revolut | Up to 1 business day | Depends on currency |

| Deel Card | Instant | Depends on currency |

| Instant Card Transfer | Instant | 2.5% |

| Payoneer | Fast arrival | 1% |

When funds are urgently needed, you can prioritize platforms with fast arrival, but pay attention to fees and limits.

Pros and Cons Analysis

When choosing withdrawal channels, you should comprehensively consider arrival cycle, compliance, fees, and fund security. Below is a comparison of the main channels’ advantages and disadvantages:

- Bank Transfer

- Advantages: Strong compliance, suitable for large transactions, high fund security.

- Disadvantages: Arrival cycle affected by business days and compliance review; may be delayed in some cases; procedures are relatively cumbersome.

- International Wire Transfer

- Advantages: Suitable for cross-border large transfers, wide global coverage.

- Disadvantages: Longer arrival cycle, higher fees, requires detailed documents, strict compliance review.

- Third-Party Payment Platforms

- Advantages: Fast arrival, convenient operation, multi-currency support.

- Disadvantages: Some platforms have low limits, higher fees, and compliance may be lower than banks in certain scenarios.

When paying final property amounts, you need to choose the most suitable channel based on actual needs. If there are strict requirements for arrival cycle, reserve time in advance to avoid transaction delays due to withdrawal failure or postponement. You can also combine multiple channels and operate in batches to further reduce fund risks.

Tip: When selecting withdrawal channels, pay close attention to promised arrival cycles and compliance requirements, arrange funds rationally, and ensure smooth transaction completion.

Channel Selection Recommendations

Time Urgency and Amount Size

When choosing withdrawal channels, first consider time requirements and amount size. If you need to complete large fund payments in a short time, such as final property payments, it is recommended to prioritize counter or online banking services from Hong Kong licensed banks. These channels offer high compliance and are suitable for large USD fund transfers. If the amount is smaller and time is extremely urgent, consider third-party payment platforms — some support instant arrival but usually have per-transaction limits.

Tip: For large amounts, it is recommended to operate in batches and reserve 1-3 business days in advance to avoid impact on overall progress due to single-transaction limits or review delays.

Compliance and Security

When withdrawing funds, you must prioritize compliance and fund security. Bank channels, especially Hong Kong licensed banks, have strict compliance review processes that effectively prevent money laundering and fraud risks. You need to prepare complete identity and fund source proof to ensure every fund flow is traceable. Although third-party payment platforms are convenient, some have lower compliance standards than banks and are suitable for small, daily use.

The table below compares compliance and security across different channels:

| Channel Type | Compliance | Security | Applicable Scenarios |

|---|---|---|---|

| Hong Kong Licensed Banks | High | High | Large, important payments |

| International Wire Transfer | High | High | Cross-border large transfers |

| Third-Party Payment Platforms | Medium | Medium | Small, flexible payments |

Fund Purpose and Personal Needs

You also need to choose the most suitable channel based on fund purpose and personal needs. For large, high-compliance-requirement scenarios such as final property payments, tuition, or medical expenses, bank channels are recommended. If you need multi-currency settlement or frequent small transfers, third-party payment platforms are more flexible. You can flexibly combine multiple channels based on your fund flow frequency, arrival speed needs, and fee budget.

Recommendation: Communicate with the recipient in advance to confirm receipt method and expected arrival cycle, ensuring every fund arrives on time and safely, avoiding impact on important transactions due to improper channel selection.

Suggestions to Avoid Withdrawal Failure and Delays

Advance Planning and Time Reservation

When arranging large-amount withdrawals, advance planning and reserving sufficient time are crucial. Many withdrawal failure cases stem from last-minute operations or insufficient document preparation. You can take the following measures to improve fund scheduling flexibility and security:

- Act early to avoid excessive account balance accumulation and reduce pressure from last-minute large withdrawals.

- Make larger withdrawals during periods of lower tax rates, rationally allocating annual fund flows.

- Use age 60 to fund TFSA or non-registered accounts, reducing future large withdrawal risks.

- Spread savings across RRSP, TFSA, and non-registered accounts for flexible annual withdrawal limit allocation.

- Arrange withdrawals rationally according to government benefit programs to protect income and reduce unnecessary tax burden.

Through these methods, you can effectively reduce withdrawal failure risks caused by time pressure or incomplete documents.

Batch Withdrawals and Fund Diversification

When handling large amounts, it is recommended to adopt batch withdrawal and fund diversification strategies. Single large withdrawals easily trigger bank compliance reviews and extend arrival cycles. You can divide funds into several portions and withdraw through different channels or accounts. This not only reduces single-transaction review pressure but also improves overall arrival flexibility and security. You can also combine bank counters, online banking, and third-party payment platforms for flexible integration, ensuring every fund arrives on time.

Communication and Progress Follow-up

During the withdrawal process, actively communicating with banks or payment platforms is very important. You should promptly understand the review progress and arrival status of each fund. When delays occur, proactively contact the relevant institution, check whether documents are complete, and supplement required files in time. You can also keep the recipient informed of fund progress to avoid transaction delays due to miscommunication. Through full-process follow-up, you can significantly improve the controllability of fund arrival and reduce losses from withdrawal failure.

Tip: Preparing multiple withdrawal plans in advance and flexibly responding to unexpected situations is an effective way to ensure smooth final property payment.

When paying final property amounts, withdrawal failure directly affects transaction progress and fund security. You need to prioritize compliant channels and pay attention to promised arrival cycles. You can develop detailed withdrawal plans based on your needs, plan each step in advance, and reduce losses from fund delays. By scientifically selecting channels, you can ensure smooth completion of property transactions.

FAQ

How to avoid withdrawal failure caused by account information errors?

You need to carefully double-check the recipient account name, account number, and bank details. It is recommended to verify all materials in advance to ensure accuracy and reduce withdrawal failure risk.

What compliance documents are usually required by banks for large withdrawals?

You need to prepare valid identification, proof of fund sources, and purpose explanations. Hong Kong licensed banks require detailed documents to ensure funds are legal and compliant.

What is the difference in arrival cycles between bank transfers and third-party payment platforms?

Bank transfers usually take 1-2 business days; international wire transfers may take longer. Some third-party payment platforms support instant arrival but have amount and fee limits.

How to follow up promptly if funds arrive late?

You can proactively contact bank or payment platform customer service to inquire about review progress. Timely supplementation of required documents helps accelerate fund arrival.

How to choose the appropriate withdrawal channel for final property payment?

You should prioritize Hong Kong licensed banks based on amount size, time requirements, and compliance needs. For fast small payments, consider third-party payment platforms.

*This article is provided for general information purposes and does not constitute legal, tax or other professional advice from BiyaPay or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or warranties, express or implied, as to the accuracy, completeness or timeliness of the contents of this publication.

Related Blogs of

IBM Plunges While ASML Rises: Is Capital Rotating from Software to AI Hardware?

How Much Is Venmo Worth in the PayPal Acquisition Case? User Scale, Revenue, and Strategic Value

Understanding Net Interest Margin and Provision Changes Through JPM, BAC, and Citi

How Should ASML’s New Orders Be Read? Revenue Differences Between EUV, DUV, and High-NA EUV

Choose Country or Region to Read Local Blog

Contact Us