- More

- Download

International Students Returning Home After Graduation: How to Most Conveniently and Cost-Effectively Bring Back the Few Thousand USD Left in Your US Bank Card?

Image Source: unsplash

When international students graduate and return home, your most worry-free and cost-effective option is to use digital remittance apps (such as Wise) or ACH bank transfer to directly send the remaining balance from your US bank card to a mainland China account. These platforms typically offer exchange rates close to the mid-market USD to CNY rate, with low fees and a convenient process. You only need to operate online without visiting a bank branch, and the funds are secure. Note that although some platforms advertise zero fees, there may actually be a hidden 1–2% markup in the exchange rate.

Core Key Points

- Choose digital remittance apps like Wise or BiyaPay for transparent fees and near mid-market rates — suitable for most international students’ fund transfer needs.

- When using US bank international wire transfers, pay attention to fees and arrival time; plan ahead to avoid delays.

- Carrying cash back to China carries high risk; it is recommended to avoid large amounts of cash to ensure safety and compliance.

- Before transferring, check each platform’s real-time exchange rates and fees in advance, plan the transfer timing reasonably, and ensure funds arrive smoothly.

- Before closing your US bank account, make sure all transactions are complete and the balance is transferred to avoid process interruptions due to incomplete information.

Comparison of Fund Transfer Methods for International Students Returning Home

Pros & Cons of International Wire Transfers

You can choose to use your US bank’s international wire transfer service to send the account balance directly to a mainland China bank account. This method offers high security and clear fund traceability, making it suitable for larger transfer amounts. You only need to initiate the transfer via online banking or mobile banking and fill in the recipient’s mainland China account details.

However, international wire transfers usually come with high fees and uncertain arrival times. Fees vary significantly between banks, and some include intermediary bank charges. The table below shows the average fee ranges for international wires from major US banks:

| Bank | International Wire Fee |

|---|---|

| Average | 5 USD to 75 USD |

You also need to note that some banks charge separate fees for outgoing and incoming international transfers, with average outgoing fees around 29 USD and incoming fees around 13 USD.

Arrival time is generally 1–5 business days, depending on the bank’s processing speed and intermediary routing. If you are short on time during the graduation season, international wires carry the risk of delayed arrival.

Pros & Cons of Third-Party Platforms (Wise, PayPal)

You can also choose third-party digital remittance platforms such as Wise or PayPal. These platforms are convenient to use, support online transfers, and require no branch visits. You only need to link your US bank card, enter the mainland China recipient account details, and the system will automatically handle the currency exchange and fund settlement.

Wise usually offers near mid-market USD to CNY rates with relatively low transfer fees and fast arrival. PayPal is suitable for small transfers with a simple process, but fees and exchange rate costs are comparatively higher. The table below compares the main fees, speed, and exchange rates of Wise and PayPal:

| Service | Wise | PayPal |

|---|---|---|

| Transfer Fees | Usually low, varies by currency & method | 2.7%–2.9% + 0.3 USD per transaction |

| Transfer Speed | 0–2 days | 0–3 days |

| Exchange Rate | Mid-market rate | Usually adds 3–4% markup on mid-market rate |

When choosing a platform, focus on the actual amount received and total cost. Wise is ideal for users seeking low costs and high exchange rate transparency. PayPal suits quick small transfers, but long-term costs are higher. Emerging platforms like BiyaPay also offer multi-currency settlement and digital currency exchange services for Chinese-speaking users, providing more flexible fund management in some scenarios.

If your priority is operational certainty before closing the account, you can first use BiyaPay’s exchange rate comparison tool to check the USD cost range at different times, then review its remittance service page for transfer path, fee disclosure, and documentation requirements, so you do not discover process or cost gaps right before account closure.

In this context, BiyaPay is better understood as a multi-asset wallet that can assist with organizing and transferring cross-border funds. If you also want to verify publicly disclosed business scope or compliance information, you can check its official website, keeping rate comparison, transfer planning, and record retention within one consistent workflow.

Risks of Carrying Cash Back to China

You can also choose to carry cash back to China. This method has no fees and is simple to operate, but it carries high security risks. Both the US and mainland China have strict cash declaration requirements for inbound and outbound travel — carrying more than 10,000 USD requires customs declaration; failure to do so may result in seizure and penalties.

During travel, you also face risks of loss or theft. Cash exchange rates for CNY are usually less favorable than bank or third-party platforms. For international students returning home after graduation, carrying cash is not recommended, especially for larger amounts.

Recommended First-Choice Method

When returning home after graduation, it is recommended to prioritize third-party digital remittance platforms such as Wise or BiyaPay. These platforms offer transparent fees, near mid-market rates, fast arrival, and a simple process. You only need to submit the transfer request online without complicated procedures, making them suitable for most international students’ fund transfer needs after graduation.

If you need to transfer a large amount or have extremely high security requirements, consider using US bank international wire transfer, but reserve sufficient time for arrival and pay attention to fees and intermediary charges.

Carrying cash is only suitable for very small amounts with special needs. Avoid carrying large amounts of cash to ensure fund safety and compliance.

Quick Tip: Before transferring funds, it is recommended to check each platform’s real-time exchange rates and fees in advance, plan the transfer timing reasonably, and ensure funds arrive smoothly to avoid impacting the US bank account closure process due to insufficient balance or operational errors.

International Wire Transfer Operation Process

Image Source: unsplash

Log In to US Online Banking to Initiate Wire Transfer

When preparing for an international wire transfer, you first need to log in to your US bank’s online banking system. Most major banks support initiating international wires online. The specific steps are as follows:

- Log in to your online banking account.

- Go to the “My Accounts” page and select the “International Wire” or “International Transfer” function.

- Choose the account you want to send from and set the transfer date.

- Follow the system prompts to enter the recipient information page.

During the process, it is recommended to prepare all recipient information in advance to avoid interruptions due to incomplete details.

Fill in Mainland China Recipient Information

You need to accurately fill in the recipient’s mainland China account details. The table below lists the main information commonly required by banks:

| Required Information | Description |

|---|---|

| Sender Account Details | Your US bank account information |

| Recipient Full Name | Full name of the recipient in mainland China |

| Recipient Address | Recipient’s residential address |

| Recipient Bank Code | Recipient bank’s code |

| Recipient IBAN or Account Number | Recipient’s bank account number or IBAN |

| Recipient Bank Country | Usually fill in “China” |

| Transfer Amount | The USD amount you wish to send |

| Reference Information | Optional — e.g., tuition, living expenses, etc. |

| Purpose of Remittance | e.g., “International student returning home fund transfer” |

Be sure to double-check all information, especially the recipient’s name, bank code, and account number — any error may cause the transfer to fail or be delayed.

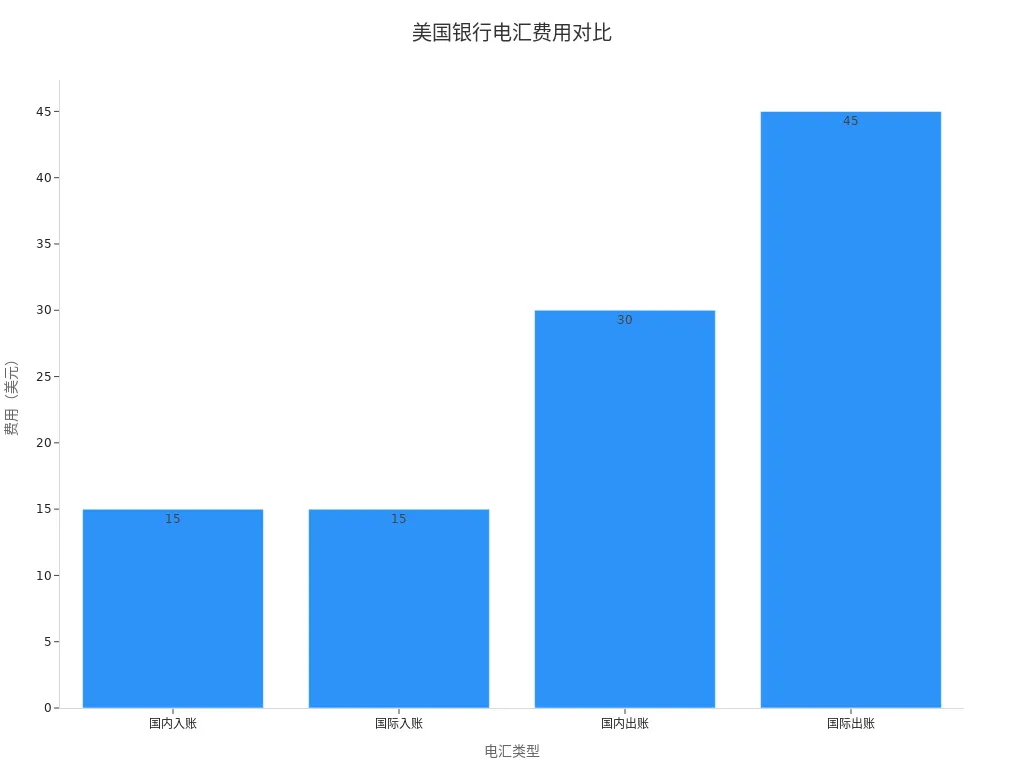

Fees & Arrival Time

US bank international wire transfers usually incur certain fees. You can refer to the table below for common fee ranges:

| Type | Average Wire Fee (USD) |

|---|---|

| Outgoing International | 45 |

| Incoming International | 15 |

After initiating an international wire, funds generally arrive within 1–5 business days. Arrival time depends on the bank’s processing speed and intermediary routing. If you are operating during the peak graduation season, it is recommended to reserve ample time to avoid delays impacting account closure.

Quick Tip: If you encounter delays, incorrect information, or frozen funds, contact US bank customer service immediately, provide proof of transfer and recipient details, and assist with tracking progress or supplying additional materials.

Third-Party Platform Transfer Process

Wise Transfer Process

You can use Wise to transfer funds directly from your US bank account to a mainland China bank account. The specific steps are as follows:

- Create a Wise account online or via mobile device and complete identity verification (Wise account creation & verification).

- Visit the Wise website or app homepage.

- Select the currency you wish to hold and click Add Currency.

- Add funds and re-verify identity to ensure account security.

- Enter mainland China recipient information and input the transfer amount.

- Confirm the exchange rate and fees, then submit the transfer request.

- Wait for processing — usually arrives within 1–2 business days.

Wise’s advantage lies in transparent fees, near mid-market rates, and suitability for international students returning home who seek high cost-performance transfers.

PayPal Transfer Process

You can also choose PayPal for cross-border transfers. The main process includes:

- Both sender and recipient need PayPal accounts (Sending money to China via PayPal).

- You need to set up a separate China PayPal account for the mainland recipient — cannot directly add a CNY account to an existing one.

- Use PayPal’s Xoom service to transfer funds to a mainland China bank account.

- You can add funds to your PayPal virtual wallet and send to the recipient via email or phone number.

- Understand PayPal’s cross-border fees, typically ranging from 0.5% to 7.4%, depending on the payment method.

PayPal suits small, flexible payment scenarios with a simple process, but fees and exchange rate costs are relatively higher.

Applicable Scenarios & Notes

When choosing between Wise and PayPal, refer to the table below:

| Scenario | Wise Advantage | PayPal Advantage |

|---|---|---|

| Transaction Fees | Transparent & low, uses mid-market rate + small fixed fee | Varies by country & currency; includes conversion fee |

| Payment Flexibility | Mainly focused on bank transfers; lower acceptance | Widely accepted; supports multiple payment methods |

| Fund Management | Supports multi-currency management; suitable for frequent multi-currency handling | Provides seamless withdrawal experience |

| Use Case | Ideal for international remittances; transparent fees & competitive rates | Suitable for online payments & e-commerce; versatile features |

In actual operation, choose the platform based on amount, arrival speed, and total cost. It is recommended to verify recipient account details in advance to ensure smooth arrival.

Transfer Important Notes

Amount Limits & Tax Declaration

When transferring funds from the US to mainland China, you must pay attention to annual limits and tax declaration requirements. Mainland China has clear regulations on individual annual foreign exchange settlement — usually up to 50,000 USD equivalent per person per year. If you need to pay tuition exceeding the limit, provide proof of enrollment and tuition invoices to the bank. US financial institutions automatically report international transfers exceeding 10,000 USD — no action required from you. The table below summarizes the main limits and requirements:

| Item | Details |

|---|---|

| Annual Transfer Limit | Up to 50,000 USD equivalent of foreign currency per person per year. |

| Education Expense Exemption | Tuition payments exceeding the limit require proof of enrollment and invoices. |

| US Reporting Requirement | Transactions over 10,000 USD are automatically reported — no sender action needed. |

Plan your transfer amount in advance to avoid delays or additional documentation due to exceeding limits.

Exchange Rate & Fee Optimization

When selecting a remittance service, focus on exchange rates and fees. Different platforms vary significantly in costs and rates. BiyaPay, Wise, Panda Remit, and similar platforms typically offer more competitive rates and lower fees. Refer to the table below to compare mainstream services:

| Remittance Service | Fee | Exchange Rate | Speed | Notes |

|---|---|---|---|---|

| Panda Remit | $5–$10 | Competitive rates | Within minutes | Direct deposit to Alipay & WeChat Wallet |

| Wise | Transparent pricing | Mid-market rate | May be slower | Depends on bank partners |

| Remitly | Tiered speed options | May be higher | Fast or economy | Offers different speed options |

Foreign exchange service platforms can usually help you reduce overall transfer costs and improve arrival efficiency. Compare multiple platforms before transferring and choose the optimal option.

Mainland China Recipient Account Requirements

You need to ensure the mainland China recipient account is eligible to receive international transfers. Generally, the following account types can smoothly receive US remittances:

- RMB accounts opened in the US support international transfers (Wise CNY account).

- Wise multi-currency card can be used for receiving and payments.

- Some banks require minimum balances and international fees for accounts receiving international wires.

- Personal accounts at Hong Kong licensed banks generally support international transfers.

- Personal checking accounts at banks such as CTBC can be opened online or in-branch and meet international transfer eligibility.

When filling in recipient information, be sure to verify account type and bank requirements to avoid transfer failure due to mismatch.

Preventing Fund Freezes

During cross-border transfers, pay attention to compliant operations to prevent funds from being frozen. It is recommended that you:

- Retain all transfer-related vouchers, including transfer records, purpose statements, tuition invoices, etc.

- Avoid frequent small-amount split transfers to prevent banks from flagging them as suspicious activity.

- Clearly state the purpose of the transfer, e.g., “tuition,” “living expenses,” etc., to increase transparency.

- If the bank requests additional materials, promptly cooperate and provide relevant proof.

Preparing relevant materials in advance can effectively reduce the risk of fund freezes and ensure smooth arrival.

US Bank Account Closure Process

Image Source: pexels

Closing a US bank account is an important step international students must complete after returning home. You need to ensure funds are safely transferred and avoid legacy issues. The following details online, phone, and mail closure methods, as well as key preparations and notes before and after closure.

Online Closure Steps

You can close your account through the US bank’s online banking system. The operation process is as follows:

- Log in to your US bank online or mobile banking.

- Check all outstanding checks and pending deposits/withdrawals, ensure all transactions are complete.

- Transfer or withdraw the account balance. You can wire to a mainland China bank account or request a mailed check.

- Cancel all automatic payments and direct deposits; update with new bank information.

- Download account statements and related documents for future retention and proof.

- Submit an account closure request through the online banking system or confirm closure via online customer service.

- Wait for bank processing and receive account closure confirmation.

During the process, it is recommended to prepare all recipient information and documents in advance to avoid interruptions due to incomplete details. Some banks may require identity proof or additional materials — cooperate promptly.

Phone or Mail Closure

If you cannot access US bank online banking, you can close the account via phone or mail. The specific steps are as follows:

- Confirm all pending transactions are complete, including deposits, withdrawals, and automatic payments.

- Update deposit and automatic payment information to ensure funds are transferred to the new account.

- Withdraw the account balance or request the bank to wire the remaining funds.

- Call US bank customer service (e.g., 800-USBANKS) and explain the account closure request.

- Alternatively, prepare a written request including full account number, closure request details, and signature, and mail it to the bank’s designated address.

- Request account closure and obtain written confirmation.

When communicating by phone or mail, it is recommended to clearly explain account details and fund destination to ensure accurate processing. Some banks may require passport, student ID, or other identity materials — prepare in advance to improve efficiency.

Friendly Tip: When closing via phone or mail, it is recommended to retain all communication records and bank replies as proof for future fund tracking.

Pre-Closure Preparation

Before initiating US bank account closure, complete the following preparations:

- Find a new bank account to hold funds. You can open a mainland China bank account in advance or use third-party platforms like BiyaPay or Wise for fund transfer.

- Check account balance. If the account is negative, banks usually will not allow closure. You must first settle the balance.

- Update all direct deposits and bill payments to ensure funds are transferred to the new account.

- Cancel all automatic deductions and subscription services to avoid failed charges due to account closure.

- Download all historical statements and transaction records for future retention and tax declaration.

Planning fund transfer and account closure timing in advance can effectively avoid leftover funds and operational errors.

Post-Closure Notes

After account closure, pay attention to the following:

- Common reasons for account closure include inactivity, suspected fraud, excessive overdraft, or failure to meet minimum balance requirements. Understand the specific reason your bank closed the account.

- If closed due to inactivity, you can contact the bank to reactivate.

- Immediately contact the bank to confirm funds safely arrived in the new account. Ask how to quickly and safely receive the balance.

- If the account has a negative balance, promptly ask the bank how to settle outstanding amounts to avoid impacting credit score.

- Retain all account closure confirmations and fund transfer vouchers for future tracking and proof.

Quick Tip: After returning home, it is recommended to regularly check the new account’s fund status to ensure all funds arrive safely and avoid legacy issues from account closure affecting personal credit and fund security.

| Closure Method | Brief Operation Process | Applicable Scenario |

|---|---|---|

| Online Closure | Submit request via online banking, download statements, transfer funds, close account | Users who can access online banking |

| Phone Closure | Phone communication, identity verification, fund transfer, close account | Users unable to access online banking |

| Mail Closure | Written request, mail materials, fund transfer, close account | Cases requiring additional identity verification |

Choose the most suitable closure method based on your situation, plan fund transfer and account closure timing in advance, and ensure smooth completion.

Options & Recommendations for Retaining a US Bank Card

Convenience of Keeping the Account

If you choose to retain your US bank card after returning to China, you can enjoy multiple conveniences. First, keeping the account helps simplify cross-border financial management. You can directly use the US bank card for international payments, avoiding high international transaction fees. US bank cards support global online consumption and subscription services, making daily payments convenient in Chinese-speaking regions or other countries. You can also use global payment platforms like BiyaPay to flexibly transfer US bank card funds into multi-currency accounts, enabling free management of USD, HKD, cryptocurrency, and other assets. Retaining a US bank card helps maintain a good US credit history, supporting future applications for credit cards, loans, or rentals. While residing in the US, you can continue strategic investments and savings to avoid future financial pitfalls.

After retaining your US bank card, you can log in to online banking anytime to manage account balance, transaction records, and automatic deductions. You can also use global remittance services to transfer funds to Hong Kong licensed bank accounts to meet diverse financial needs.

Applicable Scenarios & Risks

Retaining a US bank card brings significant advantages in the following scenarios:

- When planning future US travel, short-term study, or work, directly use the US bank card to pay for accommodation, transportation, and tuition, avoiding exchange and account opening processes.

- When needing to continue investing in the US market or participating in US stock trading, retaining a US bank card facilitates fund inflows/outflows and asset management.

- When using platforms like BiyaPay for global payments, cryptocurrency exchange, or US/Hong Kong stock fund management, retaining a US bank card improves liquidity and operational efficiency.

When retaining a US bank card, also pay attention to potential risks:

- There may be additional tax obligations between the US and China; you must comply with IRS reporting requirements, such as filing the Foreign Bank and Financial Accounts Report (FBAR).

- Funds in foreign accounts may not be protected by FDIC insurance, posing fund security risks.

- Foreign exchange fluctuations may cause losses; political or economic instability may also affect bank security.

| Advantages | Risks |

|---|---|

| Simplifies financial management | Must comply with US tax reporting requirements |

| Avoids high international transaction fees | Funds not protected by FDIC insurance |

| Maintains US credit history | Foreign exchange fluctuations & political/economic risks |

| Supports global payments and investment | Possible account freeze or regulatory changes |

When deciding whether to retain a US bank card, combine your future cross-border needs, fund security, and compliance requirements to reasonably plan account management strategy. If you plan to develop long-term in China with no cross-border needs, it is recommended to close the US bank account in a timely manner to avoid unnecessary risks and management costs.

When returning home after graduation, it is recommended to prioritize digital platforms such as Wise or Panda Remit for transfers due to their transparent fees, near mid-market rates, and suitability for transfers under $30,000 USD. The table below compares common methods:

| Method | Applicable Amount | Features |

|---|---|---|

| Panda Remit | Less than $30,000 USD | Fast processing, competitive rates, supports Alipay & WeChat Pay |

| Wise | Less than $30,000 USD | High transparency, uses mid-market rate |

| SWIFT Bank Transfer | Over $50,000 USD | Industry standard, suitable for large transfers, slower processing |

During operation, pay attention to compliance risks and fund transfer procedures to avoid fund freezes due to information errors or non-compliance. Refer to the table below:

| Key Risks & Considerations | Description |

|---|---|

| Compliance Risk | All US citizens and residents must comply with OFAC regulations; assets/accounts involving designated countries or entities must be blocked. |

| Suspicious Activity Vigilance | Financial service providers must watch for suspicious financial activity related to illegal immigration that may impact national security. |

| Fund Transfer Procedures | When funds involve OFAC-designated parties, transactions must be blocked and funds placed in blocked accounts. |

Plan fund transfer and account closure timing in advance to ensure all processes are completed smoothly. Choose reasonable channels and retain vouchers to effectively protect fund security.

FAQ

Can a US bank card be restored after closure?

After closing a US bank card, the account usually cannot be restored. If you need to use it again, you must apply for a new account. It is recommended to back up all transaction records before closure.

What materials are needed to transfer to a mainland China account?

You need to provide the mainland China recipient’s name, bank account number, bank code, recipient address, and purpose of remittance statement. Some banks may require additional identity proof.

Are there amount limits for transfers via BiyaPay and Wise?

When using BiyaPay or Wise, both single and annual transfer amounts are limited. Generally, single transfers do not exceed 50,000 USD, and annual totals must comply with mainland China foreign exchange settlement regulations.

How long does it take for funds to arrive after transfer?

Transfers via platforms like BiyaPay or Wise usually arrive within 1–2 business days. Bank international wires may take 1–5 business days, depending on the bank’s processing speed.

What to do if funds are frozen?

If funds are frozen, immediately contact the remittance platform or bank customer service, provide proof of transfer and purpose statement. Cooperate by supplying additional materials and wait for bank review and processing.

*This article is provided for general information purposes and does not constitute legal, tax or other professional advice from BiyaPay or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or warranties, express or implied, as to the accuracy, completeness or timeliness of the contents of this publication.

Related Blogs of

JPM, BAC, GS, MS, and Citi: Which Bank Stock Is More Worth Buying? A Comparison of Valuation, Dividends, and Business Structure

What Does ASML’s Guidance Upgrade Mean for TSMC, Nvidia, and U.S. Semiconductor Equipment Stocks?

Which Software Stocks Could IBM’s Selloff Drag Down? Comparing ServiceNow, Salesforce, Adobe, and Oracle

Is ASML’s Valuation Overextended After Earnings? Backlog and 2026 Guidance Risks

Choose Country or Region to Read Local Blog

Contact Us