Exchanges on Blacklist? How to Use Licensed Platforms as an 'Intermediate Layer' to Isolate Suspicious Crypto Asset Transfers

Image Source: pexels

When you discover that an exchange on the blacklist is involved in suspicious fund flows, direct transfers expose your assets to extremely high risk. You should choose licensed platforms as an intermediate layer to effectively isolate assets and reduce compliance concerns. You also need to be vigilant about legal liabilities arising from money laundering, terrorist financing, and other illegal activities, ensuring fund safety and compliance.

Key Takeaways

- Choosing licensed platforms as an intermediate layer effectively isolates risks from blacklisted exchanges and protects asset safety.

- Direct transfers with blacklisted exchanges may lead to fund freezes and legal liabilities; such operations must be avoided.

- Licensed platforms provide compliance guarantees, ensuring all transactions meet international standards and reducing compliance risks.

- Regularly review assets and personal information to detect abnormal flows in time and prevent asset theft or involvement in illegal activities.

- Use official channels for asset management, avoiding unofficial apps and links to reduce phishing risks.

Risks of Exchanges on the Blacklist

Image Source: pexels

Fund Freeze Risk

When you operate assets on exchanges listed on the blacklist, you face an extremely high probability of fund freezes. Many blacklisted exchanges are involved in illegal activities such as money laundering and terrorist financing; global regulators closely monitor these platforms. Once funds interact with these platforms, wallet addresses are likely to be flagged, leading to asset freezes or investigations.

The table below shows recent asset freeze statistics for blacklisted addresses:

| Time Period | Number of Blacklisted Addresses | Total Frozen Asset Value |

|---|---|---|

| January 1, 2016 – present | 5,188 | Over $2.9 billion |

| June 13–30, 2025 | 151 | $86.34 million |

| Highest single-day blacklisting | 63 | N/A |

| Proportion of newly created accounts | 41% | N/A |

| Pre-freeze transfer-out proportion | 54% | N/A |

If your assets are flagged on the blacklist, you may lose access rights and even be unable to participate in innovative services such as decentralized finance (DeFi).

Compliance and Legal Liability

Direct transfers with blacklisted exchanges easily trigger compliance investigations. Many countries and regions have strict regulations on crypto asset flows; blacklisted exchanges are often accused of conspiring in money laundering, operating unlicensed money transmission businesses, violating the International Emergency Economic Powers Act (IEEPA), and more.

The table below lists common legal accusation types:

| Accusation Type | Specific Content |

|---|---|

| Conspiracy to commit money laundering | Defendant knew Tornado Cash protocol was used for money laundering activities. |

| Conspiracy to operate unlicensed money transmission business | Involved in unlicensed money transmission. |

| Conspiracy to violate IEEPA | Involved in violations of the International Emergency Economic Powers Act. |

Once involved in related cases, you may face asset seizure, account freezes, or even criminal liability.

Information Leakage Risks

When operating assets on blacklisted exchanges, your personal information and transaction data face leakage risks. Some blacklisted platforms lack effective risk controls and data protection measures; hackers and threat actors may steal your account information, leading to asset theft or use in criminal activities. You may also be denied service by other compliant platforms due to information leakage, affecting subsequent asset flows.

- Blacklisted wallets are often blocked from sending or receiving funds.

- Accounts may be suspended, causing delays in fund recovery.

- You may unintentionally participate in fraud chains, increasing legal risk.

Risks of Direct Transfers

If you directly transfer assets from a blacklisted exchange to a licensed platform, the operation is easily classified as high-risk. Many threat actors use decentralized exchanges (DEXs) and informal P2P channels to obscure fund flows, increasing regulatory difficulty. Transfers through these channels offer no fund safety guarantee and are easily traced by regulators.

- Direct asset transfers may lead to money laundering and fraud risks.

- Informal channels lack regulation, increasing fraud and regulatory evasion risks.

- Some DEXs have extremely low identity information requirements, with high transaction anonymity and significant compliance risk.

You should avoid direct asset transfers with blacklisted exchanges and prioritize licensed platforms as an intermediate layer to reduce compliance and safety risks.

Advantages of Licensed Platforms

Image Source: unsplash

Compliance License Assurance

When choosing licensed platforms, you first gain assurance from compliance licenses. Taking Biyapay as an example, the platform strictly complies with international standards, requiring identity information to accompany all cross-border virtual asset transfers in line with the FATF Travel Rule. The platform also sets higher capital thresholds based on regulatory requirements in different markets, especially for high-risk assets, further enhancing fund safety. When serving Chinese-speaking users, Biyapay applies a unified privacy policy that meets data protection regulations such as GDPR.

In practice, you can think of an “intermediate layer” platform as a compliance buffer rather than just a transfer tool. Its real value lies in making your fund flow more explainable and traceable. You can start from the BiyaPay official website to understand how its multi-asset wallet is used for cross-border payments, USDT conversion, and fund routing, and then use its rate comparison tool to evaluate costs and settlement efficiency across different paths. When funds are first routed through a compliant platform before being transferred out, the overall transaction path becomes clearer and more defensible during risk reviews or compliance checks. BiyaPay also provides publicly disclosed registrations and licensing information in jurisdictions such as the United States and New Zealand, which is useful when selecting a reliable intermediate platform.

The table below shows compliance requirements of mainstream licensed platforms:

| Compliance Requirement | Description |

|---|---|

| International standards | Complies with FATF Travel Rule; cross-border transfers must include identity information |

| Capital requirements | Higher capital thresholds set for high-risk assets |

| Data privacy | Services for EU clients must comply with GDPR; unified privacy policy |

By operating through licensed platforms, you can effectively avoid compliance and legal risks from blacklisted exchanges.

Fund Segregation Mechanisms

Licensed platforms typically adopt multiple fund segregation mechanisms. After opening an account on platforms like Biyapay, the platform segregates client assets from its own funds and stores them separately to prevent the platform’s operational risks from affecting user asset safety. The platform also conducts real-time monitoring of fund flows to ensure every transfer is traceable. During asset deposits and withdrawals, the platform automatically identifies suspicious funds and blocks high-risk flow paths. This mechanism significantly reduces asset contamination risks from blacklisted exchanges.

Risk Control and Anti-Money Laundering Measures

When trading on licensed platforms, the platform implements multiple risk control and anti-money laundering measures. Biyapay uses on-chain analysis technology to identify suspicious transactions in real time, maintains a blacklist of tainted coins, and proactively blocks flows of coins related to known illegal activities. The platform also requires all users to complete identity verification to ensure authentic and compliant fund sources. Common anti-money laundering measures are shown in the table below:

| Anti-Money Laundering Measure | Description |

|---|---|

| On-chain analysis | Identifies suspicious or illegal transactions and enhances regulatory compliance |

| Tainted coin blacklist | Lists coins related to money laundering activities and blocks high-risk asset flows |

| Identity verification mechanism | Requires users to complete real-name authentication to reduce AML risks |

Through these measures, you can effectively isolate and prevent money laundering and fraud risks from blacklisted exchanges.

User Information Protection

When operating assets on licensed platforms, the platform adopts multiple security measures to protect your account and personal information. Biyapay enhances overall platform security through reserve proofs, regular security audits, and bug bounty programs. The platform also provides you with 2FA, MFA, and other account-level protections to prevent asset loss due to password leaks. You can further reduce theft risk through device and withdrawal control features. Compliant platforms typically feature the following security characteristics:

| Security Feature | Description |

|---|---|

| Verifiable security hygiene | Reserve proofs and regular security procedures reduce blind trust |

| Account-level protection | 2FA/MFA, anti-phishing protection, device/withdrawal controls |

| Operational maturity | Audits, bug bounties, strengthened custody practices reduce single-point-of-failure risks |

Choosing licensed platforms gives you higher information security and asset protection, far superior to blacklisted exchanges.

- Compliant platforms operate legally within their jurisdiction, offering better user protection.

- Regulated platforms undergo regular audits, maintaining transparency and reducing fraud risk.

- Overall security is higher when trading on compliant platforms.

Choosing Licensed Platforms

License and Regulatory Verification

When selecting licensed platforms, first verify whether the platform holds licenses issued by authoritative regulatory bodies. Biyapay, as a typical case, strictly complies with international regulatory standards, requiring users to complete “know your customer” identity verification, continuously monitoring transactions and proactively addressing risky activities. Major global regulatory bodies are shown in the table below:

| Country/Region | Regulatory Body / Legal Framework |

|---|---|

| European Union | Markets in Crypto-Assets Regulation (MiCA) |

| Singapore | Payment Services Act |

| United States | Currently lacks unified cryptocurrency regulation |

You should prioritize platforms regulated in regions such as the EU and Singapore. The Monetary Authority of Singapore (MAS) requires all crypto companies to obtain a DTSP license, with extremely high regulatory standards.

Fund Safety and Custody

Fund safety is your core consideration when selecting a platform. Biyapay adopts multiple security measures, including strong access controls, layered security mechanisms, third-party custody, cold storage, and multi-signature technology. Hong Kong licensed banks employ similar mechanisms to safeguard client asset safety. Insurance policies provide financial protection for the platform, covering external theft and internal fraud risks. You can effectively prevent asset loss or theft through these mechanisms.

- Strong access controls and layered security measures

- Third-party custody and cold storage

- Multi-signature technology and insurance policies

Risk Control System Evaluation

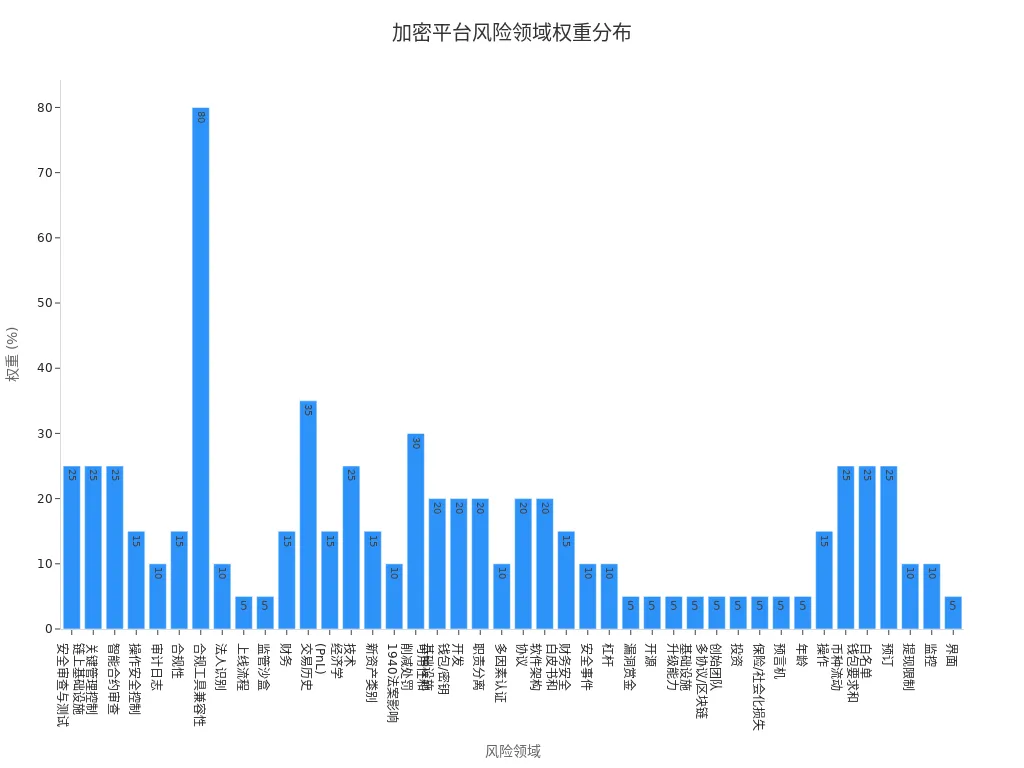

You need to evaluate the platform’s risk control system to ensure it can effectively identify and prevent risks. Biyapay enhances overall risk management capabilities through on-chain infrastructure security reviews, smart contract audits, operational security controls, and multi-factor authentication. The chart below shows the weight distribution across risk management areas for cryptocurrency platforms:

You can comprehensively assess the platform’s risk control level by referring to indicators such as audit logs, compliance tool compatibility, and wallet key infrastructure.

User Reputation Reference

When making the final platform choice, you should pay attention to user reputation and industry evaluations. Biyapay has gained wide recognition among Chinese-speaking users for its compliance transparency, fund safety, and efficient risk control. You can review professional communities, industry reports, and user feedback to understand real-world platform operations. Choosing platforms with good reputation helps improve withdrawal experience and reduce unnecessary disputes and delays.

Compliant Transfer Operation Process

When isolating and transferring assets through licensed platforms, you must strictly follow the compliance process. Every step relates to fund safety and legal liability. The following uses Biyapay as an example to detail the operation process and compliance measures.

Registration and Identity Verification

When registering an account on Biyapay, the platform requires you to complete identity verification. This process is not only a compliance requirement but also key to protecting fund safety. You need to prepare the following materials:

- Legal name

- Date of birth

- Address

- National ID number

- Government-issued identification documents (such as passport or driver’s license)

- Proof of address (such as utility bills)

- Email address

- Phone number

- Social Security number (if applicable)

Biyapay adopts a KYC process that clearly distinguishes legitimate users from potential fraudsters. After submitting materials, the platform conducts automated and manual reviews to ensure identity information is authentic and valid. Only after identity verification is passed can you perform asset operations. The KYC process not only prevents money laundering but also reduces transaction delays and improves overall compliance.

Tip: When registering, ensure all information is accurate. Any discrepancies may lead to account freezes or audit delays.

Asset Deposit and Isolation

After completing identity verification, you can transfer crypto assets to your Biyapay account. The platform segregates asset management to ensure your funds are stored separately from the platform’s own funds. Biyapay strictly follows anti-money laundering rules, maintains secure asset custody practices, and operates according to licensing requirements in different jurisdictions. During asset deposits, the platform automatically records fund sources and preserves transparent transaction records.

- Strengthens anti-money laundering rule compliance

- Maintains secure asset custody

- Conducts customer identity verification (KYC)

- Asset segregation and transparent record-keeping

Biyapay uses multi-signature and cold storage technology to safeguard asset safety. After asset deposit, the platform monitors fund flows in real time, identifies suspicious transactions, and blocks high-risk flow paths. The asset segregation mechanism effectively prevents asset contamination from blacklisted exchanges and improves overall compliance transparency.

Source of Funds Review

After asset deposit, Biyapay reviews the source of funds. The platform uses on-chain analysis tools to identify suspicious transactions and maintains a blacklist of tainted coins. You need to ensure fund sources are authentic and legal and avoid flows of coins related to known illegal activities. The platform may require you to provide proof of source of funds, such as transaction records, bank statements, or other supporting documents.

- Proof of legitimacy of fund sources

- On-chain analysis to identify suspicious transactions

- Management of tainted coin blacklist

If you conduct cross-border large or frequent transactions, the platform strengthens anti-money laundering review. Biyapay automatically triggers risk alerts based on international standards and requires additional materials. You need to understand relevant regulations in advance to avoid asset freezes or delays due to insufficient documentation.

Note: For large transfers (e.g., single transactions exceeding 10,000 USD) or frequent transactions, prepare complete proof of source of funds in advance. The platform dynamically adjusts review standards based on regulatory requirements.

Asset Withdrawal and Destination Selection

After completing fund review, you can withdraw assets to other platforms or wallets. Biyapay requires you to confirm the receiving address, blockchain network, and withdrawal amount to ensure safe asset transfer. Pay attention to the following elements:

- Receiving address: Enter the correct cryptocurrency receiving address; any character error may result in irrecoverable assets.

- Blockchain network: Select the same network as the recipient wallet; incorrect selection may cause permanent asset loss.

- Amount: Enter the accurate sending amount; the platform does not provide refunds.

Biyapay charges service fees based on different coins and networks, all denominated in USD. During asset withdrawal, the platform re-verifies fund flows to ensure no association with blacklisted addresses. You can choose to withdraw to Hong Kong licensed bank accounts, compliant US market platforms, or other secure wallets to enhance compliance and safety of asset flows.

Tip: Before asset withdrawal, verify recipient information and network selection. Any negligence may result in irrecoverable asset loss.

By completing the above process through licensed platforms, you can effectively isolate suspicious assets and reduce legal and compliance risks. Every step must strictly comply with platform requirements to ensure fund safety and compliant transparency.

Risk Control and Safety Recommendations

Segregated Account Management

When managing crypto assets, you should adopt a segregated account management strategy. Store assets for different purposes in separate accounts or wallets to isolate risks. For example, you can manage daily trading funds, long-term holdings, and high-risk investments separately. If one account experiences a security incident, it will not affect all assets. Licensed platforms like Biyapay support multi-account systems, facilitating flexible asset structure configuration. You can also combine cold wallets and hot wallets to enhance overall security.

Regular Asset Verification

You need to periodically verify held crypto assets to ensure safety and compliance. Virtual asset service providers are recommended to conduct at least one asset audit per year. If major transactions, token issuances, or other compliance-triggering events occur, audits should be performed more frequently. The table below shows common asset audit frequency recommendations:

| Audit Frequency | Description |

|---|---|

| Once per year | Virtual asset service providers are required to conduct at least one audit annually. |

| More frequent | More frequent audits required when major transactions or compliance events occur. |

By regularly verifying assets, you can detect abnormal flows in time and prevent asset theft or involvement in illegal activities.

Protecting Personal Information

When using licensed platforms, you must attach great importance to personal information protection. It is recommended to take the following measures:

- Store cryptocurrency offline to reduce theft risk.

- Enable two-factor authentication to enhance account security.

- Exercise caution when operating on mobile devices to prevent information interception.

- Encrypt sensitive data to protect digital assets.

- Beware of phishing attacks to ensure personal information security.

Through these methods, you can effectively prevent hacker attacks and information leakage, safeguarding account and asset safety.

Using Official Channels

When transferring and managing assets, always operate through official channels of licensed platforms. Avoid unofficial apps, third-party plugins, or unknown links to prevent phishing and scams. You should also regularly monitor blacklist updates and adjust asset flow strategies promptly. Blockchain analysis tools can trace fund flows, detect mixers and anonymization tools, and flag suspicious transactions for risk. These tools use complex technology to monitor on-chain transactions, identify suspicious activity, and improve compliance transparency. Choosing compliant platforms and cooperating with official risk control tools can significantly reduce the risk of assets being involved in illegal activities.

By using licensed platforms as an “intermediate layer,” you can effectively isolate risks from blacklisted exchanges and safeguard asset compliance and safety. You should continuously monitor compliance developments and remain vigilant about the following trends:

- Payment structuring and abnormal transaction speeds

- Multiple users making large transfers to unknown addresses

- Sudden changes in transaction behavior

You can also take the following measures to enhance risk prevention awareness:

- Choose hardware wallets and trusted platforms

- Regularly back up wallets and distribute asset storage

- Enable two-factor authentication and avoid operating on public Wi-Fi

Only by continuously improving compliance awareness and safe operations can you protect digital asset safety in complex environments.

FAQ

How do licensed platforms identify assets from blacklisted exchanges?

When you deposit assets through licensed platforms, the platform uses blockchain analysis tools to automatically detect fund sources, identify wallet addresses related to blacklists, and promptly block high-risk flows.

Can isolated assets still be directly transferred to personal wallets?

You can transfer isolated assets to personal wallets. The platform will re-verify receiving addresses to ensure no association with blacklisted addresses, safeguarding fund safety and compliance.

What compliance elements should be focused on when choosing licensed platforms?

You should focus on verifying platform licenses, regulatory bodies, fund custody, and risk control systems. Prioritize platforms regulated by authoritative bodies such as Singapore or the EU to enhance asset safety.

What compliance reviews are triggered by frequent large transfers?

When you perform frequent or large transfers, the platform initiates anti-money laundering review and requires additional proof of source of funds. Prepare relevant materials in advance to avoid asset freezes.

How does Biyapay protect user information security?

Biyapay adopts multiple security measures, including 2FA, cold storage, and regular security audits. All sensitive information is encrypted during platform operations to prevent data leakage.

*This article is provided for general information purposes and does not constitute legal, tax or other professional advice from BiyaPay or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or warranties, express or implied, as to the accuracy, completeness or timeliness of the contents of this publication.

Related Blogs of

What Is QLC NAND? Why Enterprise SSDs and AI Data Centers Are Paying Attention

Which Products Are Affected by NAND Price Increases? SSDs, Smartphones, Servers, and Consumer Electronics

Who Are the Leading HBM Companies? Business Differences Between Samsung, SK hynix, and Micron

What Is the Difference Between HBM Stocks and GPU Stocks?

Choose Country or Region to Read Local Blog

Contact Us

BIYA GLOBAL LLC is registered with the Financial Crimes Enforcement Network (FinCEN), an agency under the U.S. Department of the Treasury, as a Money Services Business (MSB), with registration number 31000218637349, and regulated by the Financial Crimes Enforcement Network (FinCEN).

BIYA GLOBAL LIMITED is a registered Financial Service Provider (FSP) in New Zealand, with registration number FSP1007221, and is also a registered member of the Financial Services Complaints Limited (FSCL), an independent dispute resolution scheme in New Zealand.