2026 World Cup Prediction Markets: How to Safely Withdraw Millions in USDT Without Getting Summoned for Tea?

Image Source: unsplash

When you earn millions in USDT from World Cup prediction markets, you must follow safe withdrawal principles. You should withdraw in batches, reasonably diversify funds, and choose reputable platforms for operations. Prioritize compliant channels such as Binance C2C to ensure transparent fund flows. You need to be vigilant about high-risk behaviors, especially the legal and regulatory risks inherent in prediction markets themselves, and avoid investigations due to improper operations. Safe withdrawal concerns not only fund security but also personal compliance and risk prevention.

Key Takeaways

- Withdraw in batches and avoid large one-time cash-outs. Keep each withdrawal below 10,000 USD to reduce the risk of account freezing.

- Choose reputable and compliant channels such as Binance C2C to ensure transparent fund flows and minimize legal risks.

- Maintain detailed records of fund movements and preserve complete transaction information for subsequent compliance declarations and risk prevention.

- Beware of high-risk behaviors; avoid transacting with blacklisted addresses and ensure every fund source is traceable to lower the probability of investigation.

- Complete KYC verification to prove the legitimacy of fund sources, improving the compliance and safety of withdrawals.

Withdrawal Safety Principles

Image Source: unsplash

Batch Withdrawals and Fund Diversification

When you earn a large amount of USDT from World Cup prediction markets, batch withdrawals and fund diversification must be your top priority. A single large withdrawal can easily attract attention from banks, exchanges, or regulators, increasing the risk of account freezing and investigation. You can spread funds across multiple wallets or accounts, leveraging USDT’s transfer advantages to flexibly design fund flow paths. This not only reduces single-account risk but also effectively avoids triggering controls on sensitive amounts.

It is recommended to keep each withdrawal amount within a reasonable range and avoid consecutive large operations. You can refer to international practices and control single withdrawals below 10,000 USD with reasonable time intervals. After diversification, the path design should also be clear to ensure every fund source and destination is recorded for subsequent compliance declarations and risk prevention.

Compliant Channel Selection

When selecting withdrawal channels, you must prioritize compliance and platform reputation. Compliant channels usually rely on formal financial systems, and regulated licensed exchanges have clear advantages. You can refer to the table below to understand the risks and characteristics of different channels:

| Withdrawal Method | Description |

|---|---|

| Compliance & Sustainability | Reflects long-term stability of the channel; institutional channels rely on formal financial systems and regulated licensed exchanges have obvious advantages in this regard. |

| Platform/Counterparty Risk | Personal OTC and USDT card platforms carry higher risk due to lack of strong regulation, while licensed institutions are relatively reliable. |

| Small & Flexible Withdrawals | C2C can be used, but you must fully understand the structural risks of P2P paths and mentally prepare for potential card freezes. |

| Medium to Large / High-Frequency Withdrawals | Prioritize institutional channels; although KYC is required, changing fund paths can reduce the most common card freeze risks and provide a more stable experience. |

When withdrawing from World Cup prediction markets, it is recommended to prioritize regulated platforms such as Binance C2C, especially in mainland China environments where compliant channels can maximize fund safety. You can use Hong Kong licensed bank accounts for fund landing to ensure every step complies with local laws and regulatory requirements. You should avoid unregulated personal OTC or USDT card platforms, as these channels carry high risk and can easily lead to fund freezes or investigations.

Avoiding High-Risk Behaviors

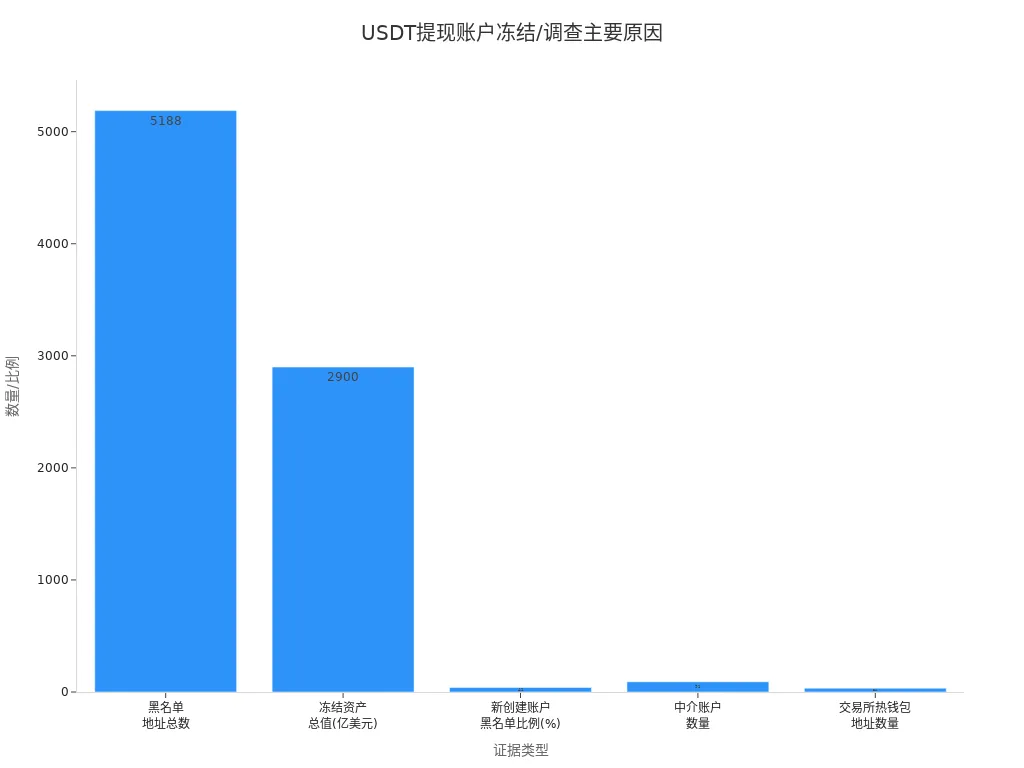

You must be vigilant about high-risk behaviors, especially during fund flows from World Cup prediction markets. High-risk behaviors include frequent large withdrawals, using blacklisted addresses, and transacting with suspicious accounts. Data shows that the main reasons for USDT-related account freezes and investigations include blacklisted addresses, asset freezes, and high proportions of newly created blacklisted accounts. The chart below displays the primary risk factors:

You should avoid transacting with blacklisted addresses or intermediary accounts and ensure every fund flow is traceable. You can transfer funds through exchange hot wallets or regulated institutions to reduce the probability of investigation. You must maintain transparent fund flows, promptly record every transaction, and avoid being summoned for tea due to improper operations.

Friendly reminder: Stay alert during operations, promptly follow policy changes and platform announcements, and rationally plan fund flow paths to ensure every step meets compliance requirements.

World Cup Prediction Market Risk Analysis

Image Source: pexels

Market Volatility and Fund Safety

When participating in World Cup prediction markets, you must pay attention to market volatility and fund safety. Historical data shows that football prediction markets experience extreme volatility during major events. For example, in December 2025, the football market showed significant volatility, with major leagues having an upset rate exceeding 50%, and the 2025/26 season reaching as high as 65.6%. The table below presents relevant data:

| Event | Result |

|---|---|

| December 2025 football market | Showed significant volatility |

| Prediction accuracy | Below expectations |

| Upset rate in major leagues | Over 50% unexpected results |

| Most volatile league | 2025/26 season (65.6% unexpected) |

You need to recognize that market volatility not only affects returns but also brings fund safety hazards. Prediction markets lack regulation, and platform reliability is lower than traditional sports betting platforms. You may face risks such as manipulated betting activity and spread of false information. Insider traders exploit VPNs and cryptocurrency anonymity, increasing the difficulty of fund tracing. You need to choose reputable platforms, diversify funds, avoid concentrated large operations, and safeguard fund security.

Tip: Regularly review fund flow paths, avoid transacting with suspicious accounts, and ensure every fund is traceable.

Gambling Characterization and Legal Risks

When participating in World Cup prediction markets in mainland China, you must understand the related legal risks. According to Chinese law, platforms like Polymarket are considered gambling, and promotional activities may constitute operating a gambling venue. The risk for ordinary players is relatively controllable, but the legal risk for promoting platforms is significantly higher. The 2010 judicial opinion clearly states that providing network services or advertising to gambling websites may be deemed complicity in operating a gambling venue.

You should avoid participating in high-risk activities such as platform promotion, advertising, or technical support. You should focus solely on personal fund management and legal channel operations to reduce legal risks. You need to monitor policy changes and adjust operational strategies promptly to ensure compliant and transparent fund flows.

- Prediction market platforms are considered gambling; promotional activities carry extremely high risk.

- Ordinary players face lower risk, but must avoid any behavior related to platform promotion.

- Providing network services, advertising, etc., may be deemed complicity in operating a gambling venue.

Recommendation: Save all fund flow records and consult professional legal counsel when necessary to ensure operations comply with mainland China legal requirements and avoid being summoned for tea.

Withdrawal Methods and Risks

Exchange Withdrawal Process

After earning large amounts of USDT from World Cup prediction markets, you will usually choose mainstream exchanges for withdrawal. Taking Binance as an example, the withdrawal process is clear and secure. You need to follow these steps:

- Select withdrawal platform. Log in to Binance or other exchanges that support USDT withdrawals and ensure your account has completed KYC verification.

- Verify withdrawal address. You must confirm the recipient’s wallet address is accurate and matches the selected blockchain network.

- Choose blockchain network. You can select TRC-20, ERC-20, or BEP-20 based on fees and transaction speed. TRC-20 is fast and low-cost, suitable for most scenarios.

- Confirm transaction. Carefully review all information, authorize the transfer, and wait for exchange processing.

During withdrawal, pay attention to the speed and fees of different networks. The table below shows typical performance of mainstream networks:

| Network Standard | Average Transaction Speed | Typical Transfer Fee (USD) |

|---|---|---|

| TRC-20 | 3–5 seconds | $1 – $2 |

| ERC-20 | 15–30 seconds (longer during congestion) | $5 – $30+ |

Choosing the TRC-20 network saves costs and is suitable for frequent batch withdrawals. ERC-20 suits high-security needs but comes with higher fees. You should select the network reasonably based on fund size and risk preference to ensure safe fund landing.

Pros and Cons of OTC Off-Exchange Trading

In actual operations, you may consider OTC off-exchange trading as a supplementary method. OTC trading includes exchange C2C and personal OTC. You need to understand the pros and cons of each:

| Method | Advantages | Disadvantages |

|---|---|---|

| Exchange C2C withdrawal | Traditional and widely used with broad coverage | P2P structural risk; funds may be frozen |

| Personal OTC trading | Flexible; prices usually negotiable and potentially better than exchange rates | Fraud and security risks; difficult to hold accountable; fund source issues |

When choosing exchange C2C, fund flows are transparent, platform regulation is strict, and it is suitable for large and high-frequency operations. You should be aware of P2P structural risks, avoid frequent large transactions with strangers, and prevent account freezes. Personal OTC trading is flexible and prices are negotiable, but security risks are high, with potential issues such as refusal to pay or forged transfer vouchers. You should prioritize reputable counterparties and avoid large nighttime transactions to reduce the probability of triggering bank risk controls.

The table below summarizes common OTC trading risks:

| Risk Type | Description |

|---|---|

| P2P transfer structural risk | Receiving funds from strangers via P2P may cause the fund chain to be traced, leading to related account freezes. |

| Personal merchant risk | Personal OTC relies on counterparty credibility and may face refusal to pay, forged transfer vouchers, etc. |

| Account risk control | Large transfers and nighttime transactions may trigger bank risk control alerts. |

| Platform risk | Centralized exchanges may suffer asset loss due to security vulnerabilities or mismanagement. |

In Chinese-speaking regions, you can consider professional service platforms like Biyapay. Biyapay provides diversified withdrawal paths for Chinese users, supports compliance audits and real-time reserve verification, and improves fund security. You should combine your own needs, rationally select withdrawal methods, diversify funds, and reduce single-channel risks.

Third-Party Service Compliance

When withdrawing USDT from World Cup prediction markets, you may encounter third-party USDT withdrawal services. You should focus on compliance measures and legal risks. Compliant services typically adopt the following measures:

| Compliance Measure | Description |

|---|---|

| Third-party audit | Recommend independent third-party audits to ensure transparency. |

| Real-time reserve verification | Enhance trust through real-time reserve verification. |

| Smart contract code embedding | Embed compliance constraints in smart contracts to follow regulations. |

When choosing platforms like Biyapay, you can obtain higher transparency and security guarantees. Biyapay provides real-time reserve verification and third-party audits for Chinese users, ensuring compliant fund flows. You should avoid unregulated third-party services to prevent fund loss and legal risks. Common legal risks include:

- Using unregulated third-party USDT withdrawal services may lead to fraud risk.

- Increased possibility of fund loss.

- Handling “dirty funds” may result in legal consequences.

You should ensure service providers do not accept mainland China ID documents to avoid concealment behavior. You should choose compliant services, save all fund flow records, and consult professional legal counsel when necessary to ensure operations comply with Chinese legal requirements.

Tip: When selecting withdrawal methods, prioritize exchange C2C and compliant third-party services, combine fund diversification principles, rationally plan fund paths, and safeguard fund security and compliance.

Compliance and Risk Prevention

Identity Verification and KYC

When withdrawing USDT, you must complete identity verification and KYC processes. Compliant identity verification is not only a platform requirement but also a safeguard for fund security. Through KYC, you can prove the legitimacy of fund sources and reduce the risk of account freezing. The table below shows the specific role of identity verification in fund safety:

| Evidence Point | Description |

|---|---|

| KYC process | Ensures fund sources are legal and traceable, reducing account freeze risk. |

| Institutional payment channels | Fund transfers through compliant financial institutions reduce risks from unclear fund sources. |

| Fund flows | Institutional channels make fund flows clearer and reduce freeze risks due to unclear counterparty sources. |

You should prioritize exchanges and Hong Kong licensed banks that have completed KYC to ensure every fund is traceable, improving withdrawal compliance and safety.

Tax Declaration and Fund Records

When withdrawing USDT in mainland China, you must prioritize tax declaration and fund flow records. Although mainland China has not yet joined CARF, tax authorities will not obtain your crypto transaction data through this mechanism. However, once you exchange crypto for fiat and deposit it into a bank account, the information enters the CRS monitoring network. You need to pay attention to the following points:

- Mainland China has not joined CARF; tax authorities currently cannot directly obtain crypto transaction data.

- Mainland China participates in CRS; fiat deposits or holding financial assets are monitored.

- The era of Hong Kong as a “safe haven” has ended; historical fund flow records are retained, and on-demand exchange channels are open.

You should proactively save all fund flow records and declare taxes reasonably to avoid compliance risks due to information opacity.

Avoiding Money Laundering Suspicion

During USDT withdrawals, you must avoid money laundering suspicion. Regulators focus on the following behaviors:

- Sender and receiver anomalies, such as creating multiple accounts to circumvent restrictions.

- Large transactions in newly created accounts in a short period.

- Unclear fund sources involving illegal activities.

- Transactions involving high-risk jurisdictions.

- Use of high-anonymity cryptocurrencies.

You should avoid frequent account changes, concentrated large operations, and transactions with high-risk regional accounts. You must keep fund paths clear and ensure every fund is traceable to reduce the risk of investigation and account freezing.

Operation Process

Fund Path Design

When designing USDT withdrawal paths, prioritize safety and compliance. You can adopt multiple monitoring and detection mechanisms to block abnormal transactions in real time. You can spread funds across multiple trusted wallets or accounts to reduce single-account exposure risk. You should set whitelists to ensure funds only flow to verified safe addresses. You can also set limits for each transaction and dynamically adjust withdrawal strategies using real-time risk scoring systems. You can flexibly control fund flows through mobile, web, or Telegram interfaces, improving operational convenience and security. You should also adopt policy-based security measures, such as two-factor authentication, especially during high-risk operations, to further protect fund safety.

Withdrawal Step Arrangement

In actual operations, you should break the withdrawal process into multiple steps. First, transfer USDT from the prediction market platform to your personal main wallet. Then, batch transfer funds to different exchanges or regulated third-party services. You should prioritize platforms that have completed KYC and ensure every fund flow is fully recorded. You can arrange withdrawal times reasonably based on actual needs and avoid concentrated large operations in short periods. You should regularly check fund flows to ensure every step meets compliance requirements. You can refer to the following process table:

| Step | Description |

|---|---|

| Fund diversification | Transfer to multiple wallets or accounts |

| Platform selection | Prioritize compliant exchanges or third-party services |

| Gradual withdrawal | Batch and time-segmented withdrawals |

| Record keeping | Retain detailed records of every fund flow |

Avoiding Sensitive Amounts

During withdrawals, you should proactively avoid sensitive amounts and abnormal behaviors. You can control single withdrawal amounts below 10,000 USD to avoid triggering controls on large consecutive operations. You should reasonably space out withdrawal times to prevent concentrated large fund flows in short periods. You should also avoid transacting with high-risk accounts or blacklisted addresses and ensure every fund source and destination is clear and traceable. You can combine platform risk scoring mechanisms to dynamically adjust withdrawal amounts and frequency. You should monitor policy changes and adjust operational strategies promptly to keep fund flows always safe and compliant.

Misconceptions and Case Warnings

Non-Compliant Operation Cases

If you ignore compliance requirements during USDT withdrawals, you can easily trigger regulatory risks. For example, one user transferred over 100,000 USD in USDT through personal OTC channels at once, resulting in a temporary bank account freeze due to abnormal large inflows. Some users frequently changed receiving accounts to evade controls, making the fund chain complex and ultimately leading to investigation due to inability to explain fund sources. Others chose platforms without completed KYC for large withdrawals, and when the platform cooperated with investigations, they could not provide valid identity information, resulting in long-term fund freezes. These cases show that non-compliant operations not only cause fund loss but may also bring legal risks.

Common Misconceptions Analysis

In actual operations, you can easily fall into the following misconceptions. You may believe that batch withdrawals alone can completely avoid risks while ignoring the compliance of fund paths. You may also mistakenly believe personal OTC channels are flexible and convenient while overlooking the legitimacy of counterparty fund sources. Some users think that as long as a platform is not named by regulators, it can be used safely, but in reality platform compliance and fund flows are equally important. You may also neglect saving fund flow records, making it impossible to prove innocence later.

Compliance Avoidance Recommendations

To safely withdraw funds, you must follow these compliance recommendations:

- Use regulated platforms for transactions; prioritize exchanges or Hong Kong licensed banks that have completed KYC.

- Understand the risks of different withdrawal methods, rationally diversify funds, and avoid concentrated large operations.

- Ensure proper documentation supports every fund source and retain complete transaction records.

- Keep suspicious funds separate from clean funds to avoid mixing and reduce investigation probability.

You should continuously monitor policy changes and adjust withdrawal strategies promptly. Only by strictly executing compliant processes can you maximize fund safety and avoid investigations due to improper operations.

When withdrawing from World Cup prediction markets, you must always adhere to compliance principles. Recent Chinese policies have made stablecoins a key regulatory focus, and the February 2026 Ban 2.0 explicitly prohibits unauthorized stablecoin issuance. You should rationally plan fund flows, operate in batches, and save complete records. Continuously monitor policy changes and choose compliant channels to effectively prevent risks and avoid investigations due to the special nature of prediction markets.

FAQ

How to choose safe USDT withdrawal channels?

You should prioritize regulated exchanges or Hong Kong licensed banks. Compliant channels safeguard fund security and reduce account freeze risks. Avoid unregulated personal OTC or third-party services.

What sensitive amounts should be avoided during withdrawals?

You should control single withdrawal amounts below 10,000 USD. Operate in batches with reasonable time intervals to avoid concentrated large fund flows in short periods and reduce the probability of triggering controls.

How to save fund flow records?

You need to save detailed records of every fund flow, including transaction time, amount, and counterparty information. Complete records help with subsequent tax declarations and compliance self-certification.

Is KYC verification mandatory?

You must complete KYC verification. Compliant platforms require identity authentication, which effectively proves the legitimacy of fund sources and reduces account freeze and investigation risks.

Will changes in mainland China policy affect withdrawals?

You need to continuously monitor mainland China policy. Stablecoin regulation is tightening, and policy changes may affect withdrawal channels and compliance requirements. Adjust operational strategies promptly to safeguard fund safety.

*This article is provided for general information purposes and does not constitute legal, tax or other professional advice from BiyaPay or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or warranties, express or implied, as to the accuracy, completeness or timeliness of the contents of this publication.

Related Blogs of

Shanghai Fudan 01385.HK vs ASMPT 0522.HK: How to Distinguish Memory Chip Design from Advanced Packaging Equipment

SanDisk SNDK vs Seagate STX: Who Benefits More from AI Data Growth, NAND Flash or HDD?

Is Micron a Cyclical Stock or an AI Growth Stock? Valuation Logic and Risk Breakdown

How Do Foundries Participate in the AI Storage Chain? Mature Nodes, Embedded Memory, and Industry Division of Labor

Choose Country or Region to Read Local Blog

Contact Us

BIYA GLOBAL LLC is registered with the Financial Crimes Enforcement Network (FinCEN), an agency under the U.S. Department of the Treasury, as a Money Services Business (MSB), with registration number 31000218637349, and regulated by the Financial Crimes Enforcement Network (FinCEN).

BIYA GLOBAL LIMITED is a registered Financial Service Provider (FSP) in New Zealand, with registration number FSP1007221, and is also a registered member of the Financial Services Complaints Limited (FSCL), an independent dispute resolution scheme in New Zealand.