How to Directly Convert USDT to USD and Transfer to a US Local Bank Account?

Image Source: unsplash

When choosing to convert USDT to USD and transfer it to a US local bank account, you should focus on three core elements: direct, safe, and compliant. Compliant platforms provide higher fund safety and transparency. You can refer to the following key factors:

- Transaction fees should be transparent and competitive, avoiding hidden costs.

- The platform must strictly enforce KYC and AML policies to protect your identity and fund safety.

- Market volatility may affect the exchange rate; choosing a reliable platform helps reduce risks.

- The platform’s security directly impacts fund safety.

In practice, it is useful to estimate conversion costs and final settlement amounts before executing a transaction. Tools like the BiyaPay exchange rate calculator allow you to check real-time USDT-to-USD pricing and compare fee-adjusted outcomes across different methods. This is especially helpful when market conditions are volatile.

For users seeking a more streamlined process, some prefer platforms that combine conversion and payout in one flow. For example, BiyaPay’s remittance service enables users to convert digital assets and transfer funds directly to overseas bank accounts. As a multi-asset wallet, it integrates cross-border payments, asset exchange, and fund management, and operates under relevant financial registrations in jurisdictions such as the U.S. and New Zealand, which helps standardize compliance and operational reliability.

Key Takeaways

- Choose compliant platforms to ensure fund safety and transparency while reducing transaction risks.

- Understand the advantages and disadvantages of different conversion methods and select the one that fits your needs, such as exchanges, OTC, or peer-to-peer platforms.

- Pay attention to transaction fees and exchange rates; choose transparent and competitive fee structures to avoid hidden costs.

- Complete KYC identity verification to ensure account security and improve convenience for subsequent transactions.

- Be mindful of tax compliance, record every transaction, and ensure adherence to US tax law requirements.

USDT to USD Conversion Methods

Image Source: pexels

Exchange Conversion

You can choose mainstream cryptocurrency exchanges to convert USDT to USD. Taking Binance, Coinbase, and Kraken as examples, these platforms support direct conversion of USDT to USD and allow you to withdraw USD to a US local bank account. You need to first register and complete identity verification, then deposit USDT into the exchange account. After completing the conversion, submit a USD withdrawal request, and the platform will transfer the funds to your US bank account via SWIFT or local bank transfer. The exchange method offers high liquidity and convenient operation, suitable for most users.

Exchanges typically require strict KYC verification to ensure fund safety and compliance. When choosing a platform, pay attention to its compliance credentials and user reviews.

OTC Over-the-Counter Trading

OTC over-the-counter trading is suitable for large-amount USDT to USD conversion needs. You can conduct one-on-one transactions with professional market makers or institutions through platforms such as Binance OTC and Genesis Trading. The process includes account registration, identity verification, negotiating the exchange rate and amount, and finally completing fund settlement. OTC trading usually has lower handling fees and better rates, but it requires higher trust between the parties and platform transparency.

Advantages: Suitable for large amounts, flexible rates. Disadvantages: Some platforms have limited information disclosure; compliance must be verified.

Peer-to-Peer Platform Trading

Peer-to-peer platforms such as Binance P2P, Paxful, and LocalBitcoins provide channels for direct trading with other users. You can post a USDT-to-USD sell order and select counterparties with good reputation. The platform ensures transaction safety through escrow, dual identity verification, and other measures. Peer-to-peer platforms have low fees and flexible payment methods, but you need to be cautious of fraud risks and prioritize users with good reviews.

| Platform Name | Supported Currencies | Security Measures | Other Features |

|---|---|---|---|

| Binance P2P | USDT, USDC | Smart contracts, reputation system | Low fees, fast trading |

| Paxful | USDT, USDC | Escrow, dual verification | Multiple payment methods |

| LocalBitcoins | USDT, BTC | Escrow, dual verification | User reputation ratings |

Digital Currency Payment Providers

Digital currency payment providers such as Biyapay, Juno, and Paytrie offer convenient solutions for converting USDT to USD and directly transferring to a US bank account. You only need to register an account, complete identity verification, deposit USDT to the platform, and select withdrawal to a US local bank account. Some providers support SEPA, SWIFT, local ACH, and other transfer methods with fast arrival, suitable for cross-border and daily payment needs.

*Biyapay and similar platforms provide multilingual support and localized services for Chinese-speaking users, improving the operation experience. When choosing, pay attention to the platform’s compliance credentials and service coverage.*

USDT to USD Operation Process

Exchange Conversion and Withdrawal

You can complete the full process of converting USDT to USD through mainstream cryptocurrency exchanges. First, create an account on compliant exchanges such as Binance, Coinbase, or Kraken and complete KYC identity verification. Usually, the platform requires you to upload government-issued ID documents and proof of address. After verification, deposit USDT from your personal crypto wallet to the exchange account.

Next, convert USDT to USD in the exchange’s spot market. After the trade is complete, go to the funds management page and select the withdrawal function. You need to bind a US local bank account that can receive USD transfers from cryptocurrency platforms. Most exchanges support SWIFT, local bank transfers (such as ACH), and some also support SEPA transfers. Enter the withdrawal amount, confirm it is correct, and submit the request. Funds usually arrive within 1–3 business days, depending on the selected withdrawal method and bank processing speed.

Tip: Some Hong Kong licensed banks have high compliance requirements for cryptocurrency-related funds; it is recommended to consult the bank’s policy in advance to ensure smooth receipt.

OTC Platform Operation Process

If you need to convert large amounts of USDT to USD, OTC over-the-counter platforms are an efficient choice. You first submit a trade request on the OTC platform or initiate the operation through designated communication channels (such as Telegram bots). The platform manager will contact you to confirm trade details, including exchange rate, amount, and receipt method.

You transfer USDT to the platform’s designated wallet address or choose offline cash delivery. After the platform receives the cryptocurrency, it transfers USD to your US local bank account via your specified method. OTC platforms typically support SWIFT, local bank transfers, and other methods with relatively fast arrival, suitable for users with high liquidity requirements.

| Method | Difficulty | Speed | Fees | Applicable Situation |

|---|---|---|---|---|

| Fiat provider | Easy | Fast | Medium | Direct withdrawal to bank account |

| Cryptocurrency exchange | Medium | Medium–fast | Low–medium | Spot trading to fiat |

| Peer-to-peer platform | Medium | Fast | Low | Limited offline service areas |

| Local exchanger/OTC | Easy–medium | Fast | Variable | Large transfers, flexible rates |

Note: OTC trading has high requirements for platform compliance and fund supervision; it is recommended to prioritize platforms with good reputation and regulatory qualifications.

Peer-to-Peer Platform Trading Process

Peer-to-peer platforms provide flexible paths for converting USDT to USD. You first select a reputable peer-to-peer platform, register, and complete KYC identity verification. Registration requires submitting an email, personal information, ID proof, and bank account details.

After account verification, you can post a USDT sell order, set competitive rates and payment methods, or directly select existing buyer orders. During the trade, transfer USDT to the platform’s escrow account; after the buyer receives USDT, they transfer USD to your US local bank account. The platform typically supports multiple payment methods, including local bank transfers and SWIFT.

If a dispute arises during the trade, you can protect your rights through the platform’s dispute resolution system. Peer-to-peer platforms have low fees and are suitable for users sensitive to flexibility and costs.

It is recommended to prioritize platforms with good history and user base to ensure transaction safety.

Payment Provider Withdrawal Process

Digital currency payment providers offer convenient solutions for converting USDT to USD. You need to register an account on the provider’s platform and complete the identity verification process. Some platforms provide multilingual support and localized services for Chinese-speaking users, improving the operation experience.

After depositing USDT to the payment provider’s account, select withdrawal to a US local bank account. The platform typically supports SWIFT, local bank transfers (such as ACH), and other methods. Enter the withdrawal amount, confirm the receiving bank information, and submit the request. Funds generally arrive within 1–2 business days, depending on the bank’s processing efficiency.

When choosing a payment provider, pay attention to its compliance credentials, service coverage, and user reviews to ensure fund safety and compliance.

Platform Selection and Identity Verification

Compliant Platform Selection

When selecting a platform to convert USDT to USD and transfer to a US local bank account, you must prioritize the platform’s compliance and security. Compliant platforms not only protect your fund safety but also effectively reduce transaction risks. You can refer to the following core standards:

- Choose peer-to-peer platforms with good reputation that have a long credible history in the industry; such platforms are generally more trustworthy.

- Check the platform’s user base—the larger the number of users, the better the liquidity and higher the trade matching efficiency.

- Confirm that the platform strictly complies with relevant regulations and can provide compliant fund channels to protect consumer rights.

- Prioritize platforms with strong security measures, especially those supporting dual-factor authentication (2FA) and cold storage options, which can effectively prevent account theft and asset loss.

In actual operations, you can further judge the platform’s compliance and security by reviewing its regulatory information, user reviews, and security policies. Compliant platforms such as Binance, Kraken, and Coinbase hold relevant financial licenses in the United States or other major jurisdictions, providing higher fund protection.

KYC Verification Process

When using mainstream exchanges, OTC platforms, or digital currency payment providers, you usually need to complete the KYC (Know Your Customer) identity verification process. KYC verification is not only a compliance requirement but also an important measure to protect fund safety. The standard process includes:

- You need a cryptocurrency wallet holding USDT.

- You need a verified account on a cryptocurrency exchange or payment processor.

- You need a US local bank account that can receive payments from the crypto service provider.

- You must complete KYC verification by submitting identity proof and address proof materials.

The specific steps for KYC verification are as follows:

- Depending on the amount of cryptocurrency you are selling and your region, the platform may require you to complete quick KYC verification.

- After completing KYC verification, you usually do not need to repeat this step, making subsequent transactions more convenient.

During the verification process, make sure the submitted information is true and valid to avoid review failure due to mismatched documents. Compliant KYC processes not only enhance account security but also provide compliance assurance for subsequent large-amount fund operations.

Fees and Arrival Time

Image Source: pexels

Handling Fee Comparison

When choosing a platform to convert USDT to USD and withdraw to a US local bank account, handling fees are an important factor affecting total cost. Mainstream exchanges such as Binance, Coinbase, and Kraken typically charge 0.1% to 0.5% trading fees, plus additional USD withdrawal fees when withdrawing to a US bank account. Taking digital currency payment providers like Biyapay as an example, the overall fee structure is more transparent and suitable for Chinese-speaking users. Peer-to-peer platforms have lower fees but require caution regarding hidden costs. The table below compares handling fees and exchange rates across different platforms:

| Platform | 20 USD to USDT | Notes |

|---|---|---|

| Coinbase | ~19.97 USDT | After fees |

| Kraken | ~19.95 USDT | Including spread |

| Binance | ~19.98 USDT | Including trading fees |

Exchange Rate and Cost

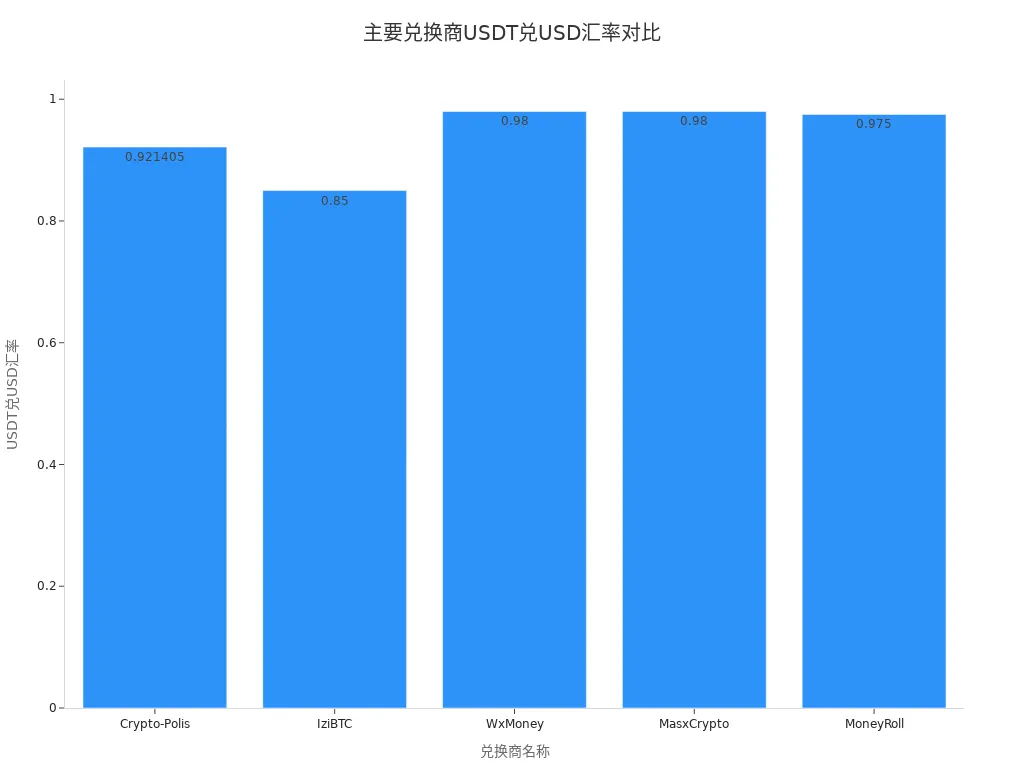

During the conversion process, the actual amount received is affected not only by fees but also by the exchange rate. Different exchangers have varying USDT-to-USD exchange rates. Recent data shows that mainstream exchangers’ rate range is 0.85 to 0.98 USD/USDT, with an average rate of about 0.98 USD. Some platforms like WxMoney and MasxCrypto have rates close to 1:1, suitable for large-amount conversions. You can refer to the table below:

| Exchanger | 1 USDT to USD Rate | Minimum Amount | Maximum Amount |

|---|---|---|---|

| Crypto-Polis | 0.921405 | 578 | 12,839 |

| IziBTC | 0.850000 | 140 | 50,000 |

| WxMoney | 0.980000 | 1,021 | 76,930 |

| MasxCrypto | 0.980000 | 5,613 | 100,000 |

| MoneyRoll | 0.975000 | 7,180 | 150,000 |

| Average Rate | 0.979635 | None | None |

You should also pay attention to USDT’s own price fluctuations. Currently, 1 USDT is approximately 1.0002 USD, with a 24-hour low of 0.99979 USD and high of 1.0006 USD. Over the past 30 days, the overall trend has been downward.

Arrival Time

Arrival time directly affects your fund liquidity efficiency. Processing times vary significantly across methods:

| Method | Processing Time |

|---|---|

| Centralized exchange | Hours to weeks |

| Peer-to-peer platform | Within one day |

| Withdrawal processing | Hours, occasional delays |

| Bank account receipt | Usually hours, occasional freezes or rejections |

Withdrawing USD to a US bank account via platforms like LatAm Payments typically takes 1–3 business days. The blockchain transfer step usually takes only minutes to 1 hour, but final arrival depends on the bank’s processing efficiency. When choosing a platform, comprehensively consider handling fees, exchange rates, and arrival speed to improve overall fund usage efficiency.

Risks and Precautions

Compliance and Fund Supervision

When converting USDT to USD and transferring to a US local bank account, you must place high importance on compliance risks. The regulatory environment for stablecoins in the United States is constantly evolving; the GENIUS Act sets federal standards for stablecoin issuers, requiring reserve management and information disclosure. You need to pay attention to the issuer’s reserve transparency—some platforms disclose daily, others only quarterly. Stablecoins are not protected by FDIC or government insurance; fund safety mainly depends on the issuer’s compliant operations. Regulations vary across countries and regions; failure to comply may result in penalties. Additionally, the GENIUS Act introduces new obligations such as reserve management and audits, which may affect cooperation between platforms, banks, and technical service providers.

Platform Security and Anti-Fraud

When choosing a platform, prioritize its security measures. Mainstream platforms typically enable multi-factor authentication (MFA) to effectively enhance account security. Platforms implement real-time transaction monitoring to promptly identify suspicious activity, use strong security protocols and firewalls to prevent hacker attacks, and regularly update systems and software to patch potential vulnerabilities. You should also ensure the platform strictly enforces KYC and AML processes to prevent identity theft and money laundering risks. It is recommended to regularly check account security settings, be vigilant against phishing websites and social engineering scams, and avoid asset losses due to personal negligence.

Tax Compliance

When converting USDT to USD and transferring to a US local bank account in the United States, you must fulfill tax reporting obligations. US tax law treats cryptocurrency as property; selling, trading, or transferring constitutes a taxable disposition of capital assets. Even though USDT is stable in price, you must record every conversion transaction as a taxable event. If you convert more volatile cryptocurrencies such as Bitcoin to USDT, additional reporting requirements may apply. You should keep detailed records of fund sources and transactions to simplify tax filing and prepare for potential future tax audits.

When converting USDT to USD and transferring to a US local bank account, prioritize centralized exchanges. Such platforms offer high liquidity and strict compliance measures, effectively reducing fund risks. You need to complete identity verification to ensure account security. Do not overlook platform transparency and security for the sake of low fees. Different users have varying needs; you can flexibly choose the most suitable conversion path based on transaction amount, arrival speed, and service experience.

FAQ

How long does it take for USD funds to arrive in a US local bank account after converting USDT?

You usually receive USD within 1 to 3 business days. Arrival speed depends on the selected platform, bank processing efficiency, and withdrawal method (such as SWIFT or ACH).

What fees are incurred during the conversion process?

You need to pay transaction handling fees, withdrawal fees, and possible exchange rate spreads. Fee structures vary by platform; it is recommended to review the platform’s official explanation in advance.

How to determine a platform’s compliance and security when choosing one?

You can check whether the platform holds financial licenses in the United States or other major jurisdictions. You should also pay attention to the platform’s KYC, AML policies, and user reviews to ensure fund safety.

Do I need to report taxes after converting USDT to USD?

When performing USDT-to-USD conversion operations in the United States, you must report related capital gains according to US tax law. You should keep transaction records to facilitate subsequent tax filing and compliance checks.

Which users are digital currency payment providers suitable for?

Digital currency payment providers are suitable for users seeking convenient operation and fast arrival. Chinese-speaking users can choose platforms that offer multilingual support and localized services to improve the experience.

*This article is provided for general information purposes and does not constitute legal, tax or other professional advice from BiyaPay or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or warranties, express or implied, as to the accuracy, completeness or timeliness of the contents of this publication.

Related Blogs of

How to Read Pure Storage and NetApp Earnings? ARR, Cloud Revenue, Gross Margin, and Cash Flow Metrics

How Does NAND Price Increase Affect SanDisk? Enterprise SSDs, Consumer Storage, and Margin Leverage

How to Read NAND Contract Prices and Spot Prices? Why Enterprise SSDs and Consumer SSDs Do Not Move in Sync

HBM/DRAM, NAND, and HDD in AI Storage: A Comparison of Elasticity, Cycles, and Risks

Choose Country or Region to Read Local Blog

Contact Us

BIYA GLOBAL LLC is registered with the Financial Crimes Enforcement Network (FinCEN), an agency under the U.S. Department of the Treasury, as a Money Services Business (MSB), with registration number 31000218637349, and regulated by the Financial Crimes Enforcement Network (FinCEN).

BIYA GLOBAL LIMITED is a registered Financial Service Provider (FSP) in New Zealand, with registration number FSP1007221, and is also a registered member of the Financial Services Complaints Limited (FSCL), an independent dispute resolution scheme in New Zealand.