How to Manage Idle USD Funds in US Stock Accounts? High-Yield USD Cash Product Recommendations

Image Source: pexels

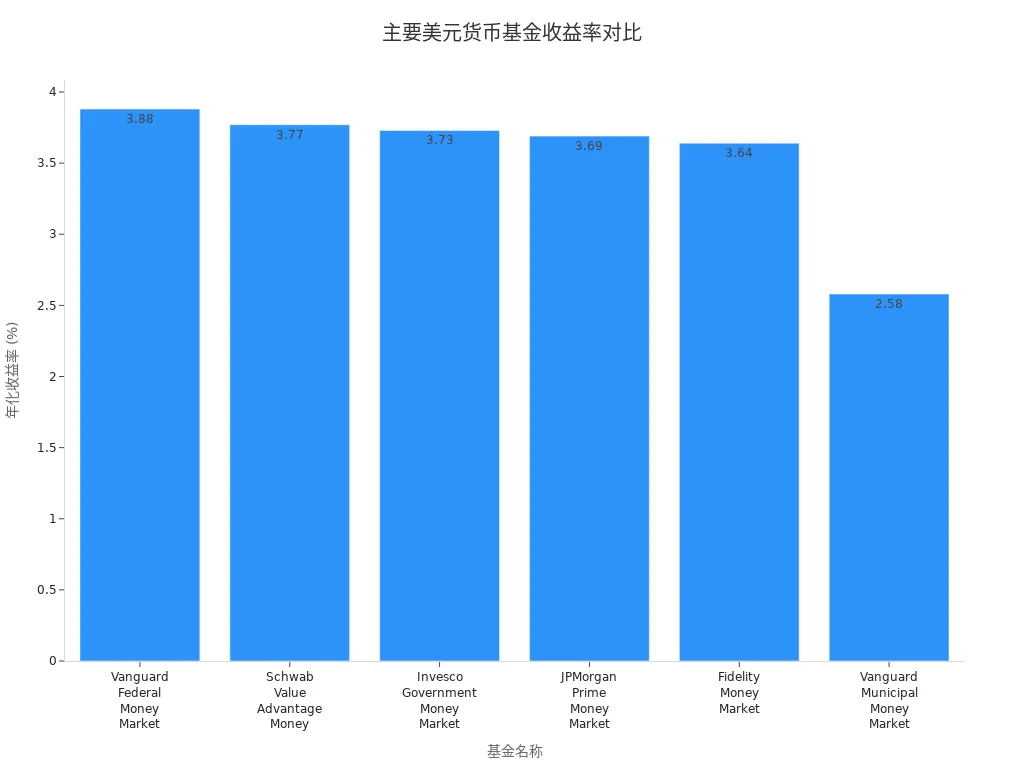

You can manage idle funds in your US stock account through various methods, such as money market funds, short-term Treasury ETFs, broker cash management services, and USD fixed deposits. These products typically feature stable returns, strong liquidity, low risk, and easy operation. For example, money market funds generally offer annualized yields between 3.6% and 3.9%, with some products having no minimum investment threshold. The table below shows the latest annualized yields and investment minimums for mainstream USD money market funds:

| Fund Name | Yield (%) | Expense Ratio (%) | Fund Assets ($ billion) | Minimum Investment ($) |

|---|---|---|---|---|

| Vanguard Federal Money Market Fund (VMFXX) | 3.88 | 0.11 | 371.3 | 3,000 |

| Schwab Value Advantage Money Fund (SWVXX) | 3.77 | 0.34 | 249.6 | None |

| Invesco Government Money Market Fund (INAXX) | 3.73 | 0.32 | 6.4 | 1,000 |

| JPMorgan Prime Money Market Fund (VMVXX) | 3.69 | 0.48 | 90.4 | 1,000 |

| Fidelity Money Market Fund (SPRXX) | 3.64 | 0.42 | 136.3 | None |

| Vanguard Municipal Money Market Fund (VMSXX) | 2.58 | 0.11 | 17.8 | 3,000 |

Key Takeaways

- Choose money market funds to manage idle funds, with stable annualized yields of 3.6% to 3.9%, strong liquidity, suitable for subscription or redemption at any time.

- Short-term Treasury ETFs offer low-risk investments, ideal for investors wanting flexible fund allocation, with yields typically higher than regular savings deposits.

- Broker cash management services automatically sweep idle funds into cash management accounts, earning interest higher than ordinary savings, with funds available anytime.

- USD fixed deposits suit investors seeking higher yields, with annualized returns usually above money market funds, but lower liquidity requiring locked funds.

- Flexibly select suitable wealth management products based on your liquidity and return needs to ensure fund safety and growth.

Ways to Manage Idle USD Funds in US Stock Accounts

Money Market Funds

You can choose money market funds to manage idle funds in your US stock account. Money market funds are mutual funds that primarily invest in high-quality short-term debt instruments, such as Treasury bills, commercial paper, and bank certificates of deposit. These products aim to maximize current income while maintaining liquidity and capital safety. You can subscribe or redeem at any time, with funds typically available in 1-2 business days. Money market fund yields are stable, with mainstream products in 2024 offering 7-day annualized yields of about 3.6% to 3.9%. The table below summarizes the main features of money market funds:

| Feature | Description |

|---|---|

| Investment Objective | Maximize current income while maintaining liquidity and capital preservation |

| Daily Liquid Assets | Daily liquidity requirement increased from 10% to 25% starting April 2, 2024 |

| Average Maturity | 60 days or less |

| Investment Approach | Invest in high-quality money market instruments with remaining maturity not exceeding 13 months |

Short-Term Treasury ETFs

You can also consider short-term Treasury ETFs. These products primarily invest in U.S. Treasury securities with maturities usually within 1 year. Short-term Treasury ETFs have extremely low risk and strong liquidity, allowing you to buy and sell like stocks during trading hours. Yields are slightly higher than savings deposits and typically correlate with Fed rate changes. They suit investors with high principal safety requirements who want flexible allocation of idle US stock account funds.

Broker Cash Management Services

Many US stock brokers provide cash management services for clients. You can automatically sweep idle funds into the broker’s cash management account to earn interest higher than ordinary savings deposits. Funds are available anytime, with no need for advance redemption when trading US stocks or transferring. Broker cash management products typically invest in money market instruments, with yields close to money market funds, excellent liquidity, and suitability for frequent traders or users needing high liquidity.

USD Fixed Deposits

If you prioritize returns, you can choose USD fixed deposits. USD fixed deposits are offered by banks or brokers, with terms ranging from 1 month to 12 months. You need to lock funds during the deposit period, with penalties for early withdrawal. USD fixed deposit annualized yields are usually higher than money market funds and cash management, but liquidity is poorer. They suit investors who do not need to use US stock account idle funds in the short term and seek higher returns.

You can flexibly choose the above methods to manage idle funds in your US stock account based on your liquidity and return needs.

High-Yield Product Recommendations for Idle USD Funds in US Stock Accounts

Image Source: pexels

You can choose from various high-yield USD cash products to manage idle funds in your US stock account. Each product has advantages in yield, liquidity, investment threshold, and risk. Below is a detailed introduction to mainstream products to help you quickly select the right option.

Vanguard Federal Money Market Fund (VMFXX)

You can manage idle funds in your US stock account through Vanguard Federal Money Market Fund (VMFXX). This fund primarily invests in U.S. government short-term bonds and high-quality money market instruments. VMFXX offers high safety and liquidity, suitable for investors seeking stable returns and flexible fund allocation. You only need to meet the minimum investment requirement to participate. Latest data shows VMFXX’s current 7-day SEC yield at 4.98%, with a minimum investment of USD 3,000.

| Item | Value |

|---|---|

| Minimum Investment Requirement | $3,000 |

| Current 7-Day SEC Yield | 4.98% |

You can subscribe or redeem anytime, with fast fund availability, suitable for managing idle US stock account funds needing high liquidity.

Fidelity Government Money Market Fund (SPAXX)

Fidelity Government Money Market Fund (SPAXX) provides a low-threshold, high-liquidity USD cash management option. SPAXX primarily invests in U.S. government bonds and money market instruments, with extremely low risk. You can participate with just USD 1, suitable for smaller fund sizes or users wanting flexible management of US stock account idle funds. SPAXX’s latest 30-day SEC yield is 4.98%, with assets under management of $247.5 billion and an expense ratio of 0.42%.

| Metric | Value |

|---|---|

| 30-Day SEC Yield | 4.98% |

| Expense Ratio | 0.42% |

| Total Assets Under Management | $247.5 billion |

| Minimum Initial Investment | $1 |

You can buy or redeem anytime, with excellent fund liquidity.

iShares Short Treasury Bond ETF (SHV)

You can choose iShares Short Treasury Bond ETF (SHV) as a wealth management tool for idle funds in your US stock account. SHV primarily invests in U.S. short-term Treasuries, with extremely low risk and yields closely tied to Fed rates. You can buy and sell like stocks during trading hours, with high liquidity. SHV suits investors with high principal safety requirements who want flexible fund allocation. No complex operations needed; trade directly through broker platforms.

Schwab Value Advantage Money Fund (SWVXX)

Schwab Value Advantage Money Fund (SWVXX) provides a no-minimum-investment-threshold USD money market fund option. SWVXX primarily invests in high-quality money market instruments, with stable returns and strong liquidity. You can subscribe or redeem anytime without fund restrictions. SWVXX’s current yield is 3.77%, expense ratio 0.34%, and assets under management $249.6 billion.

| Item | Value |

|---|---|

| Expense Ratio | 0.34% |

| Yield | 3.77% |

| Fund Assets | $249.6 billion |

| Minimum Initial Investment | None |

You can flexibly manage idle US stock account funds, enjoying high liquidity and stable returns.

Tiger Brokers Idle Cash Management

You can manage idle funds in your US stock account through Tiger Brokers’ idle cash management product. This product provides automatic cash management services, with funds available anytime, suitable for frequent traders or users needing high liquidity. Tiger Brokers idle cash management offers 1% annualized yield, minimum transfer-in amount USD 1, and fast transfer-out daily limit of USD 100,000.

| Annualized Yield | Liquidity Terms |

|---|---|

| 1% | Minimum transfer-in USD 1, fast transfer-out daily limit USD 100,000 |

You can transfer funds in or out anytime without complex operations, making fund management convenient.

Interactive Brokers (IB) Cash Interest

Interactive Brokers provides cash interest services, suitable for larger-scale idle USD funds in US stock accounts. You can earn different rates based on account asset levels, with 3.79% APY for assets over USD 320,000 and 0% for under USD 20,000. Funds are available anytime, suitable for investors needing high liquidity and higher returns.

| Asset Level | Rate |

|---|---|

| Above $320,000 | 3.79% APY |

| Below $20,000 | 0% |

You can flexibly allocate funds, enjoying high returns and convenient operations.

Longbridge Securities Balance Access

Longbridge Securities Balance Access provides multiple convenient features for managing idle funds in US stock accounts. You can trade freely without stock trading restrictions, with idle funds earning potential returns. The Balance Access product is based on money market funds, with low risk and small fluctuations. You only need to sign the agreement once for automatic subscription, no manual operation required. Low minimum investment, no account upper limit, flexible fund management.

- Free trading: No stock trading restrictions, idle funds earn potential returns.

- Return growth: Fund management continues during market holidays.

- One-time agreement: Automatic subscription, no manual operation.

- Money market fund basis: Invest in low-risk, low-volatility products.

- Low threshold: Low minimum investment requirement, no account upper limit.

You can easily manage idle US stock account funds with automation and high liquidity.

Moomoo Cash Plus

Moomoo Cash Plus provides a high-yield, low-risk management scheme for idle funds in US stock accounts. You can invest in money market funds and Treasuries, with annualized yields between 3.48% and 5.18%, and promotional rates up to 6.8%. Funds have strong liquidity and low risk, suitable for investors seeking returns and safety.

| Annualized Yield | Risk Features |

|---|---|

| 3.48% - 5.18% | Low risk, invested in money market funds and Treasuries |

| Highest Promotional Rate | 6.8% |

You can subscribe or redeem anytime, with flexible fund management suitable for various fund sizes and needs.

Through the above products, you can flexibly manage idle funds in your US stock account based on fund size, liquidity needs, and return goals. Each product offers advantages in high liquidity, low risk, and easy operation to help achieve fund growth and efficient management.

Yield, Liquidity, and Risk Comparison

Image Source: unsplash

Annualized Yield

When choosing wealth management products for idle funds in US stock accounts, you first focus on annualized yield. Different products show clear yield differences. The table below shows current annualized yields and expected future trends for mainstream USD cash management products:

| Product Type | Current Annualized Yield | Expected Change |

|---|---|---|

| Money Market Funds | Over 5% | May decline rapidly due to rate cuts |

| Extended Cash Portfolios | Higher stability | Opportunity to lock in higher yields |

You can see that money market funds and extended cash portfolios currently have similar yields. If the Fed cuts rates, money market fund yields will be directly affected. Extended cash portfolios offer the chance to lock in higher returns for certain periods, suitable for users seeking stable yields.

Liquidity

Liquidity determines how quickly you can convert funds to cash. Starting May 28, 2024, the U.S. securities settlement cycle shortened from T+2 to T+1. You can now buy and sell most US stock-related products with faster fund availability.

In money market funds, short-term Treasury ETFs, and broker cash management, you typically achieve T+1 settlement, significantly improving fund allocation efficiency. USD fixed deposits offer higher yields but require locking funds, with interest penalties for early withdrawal. If you have high requirements for fund flexibility, prioritize products with strong liquidity.

Tip: T+1 settlement makes fund management and reinvestment more efficient, reducing wait times and liquidity risks.

Risk Analysis

When selecting wealth management products, you cannot ignore risk factors. The table below summarizes core risks of major USD cash management products:

| Risk Factor | Description |

|---|---|

| Liquidity Transformation Risk | Money market funds allow daily redemptions, but underlying assets may be hard to sell quickly. |

| Potential for Large-Scale Redemptions | Certain cash management tools may face massive redemptions during market volatility, pressuring liquidity. |

| Vulnerability of Cash Management Tools | USD-denominated offshore funds and short-term investment funds may also face liquidity risks. |

In money market funds and short-term Treasury ETFs, you typically face liquidity transformation risk and potential impacts from large-scale redemptions. Broker cash management and USD fixed deposits have lower risks but may still be affected in extreme market conditions. You should allocate idle US stock account funds reasonably based on your risk tolerance, balancing returns and safety.

If you also want to keep flexibility for later stock buying, currency conversion, or cross-border fund movement while managing idle USD, it may help to first review relevant US and Hong Kong stock names on BiyaPay’s stock lookup page, then use its exchange rate comparison tool to estimate the real cost of different fund-routing options. For cash that is being managed mainly for liquidity, seeing both the investable targets and the conversion cost is often more useful than comparing headline yields alone.

BiyaPay is better understood as a multi-asset wallet, with common use cases covering currency conversion, cross-border payments, and unified management across US stocks, Hong Kong stocks, and digital assets. If you may later switch part of these idle funds between account management and investment use, you can review its official website or trading entry page first and then decide how to position that USD balance.

Investment Threshold and Operation Process

Investment Starting Point

When choosing wealth management products for idle funds in US stock accounts, you first need to understand the minimum investment thresholds for various products. Different products have varying starting capital requirements. Some cash management accounts support zero threshold, while money market funds and broker-issued CDs have certain minimums. The table below summarizes minimum investment requirements for mainstream USD cash management products:

| Product Type | Minimum Investment Threshold |

|---|---|

| Vanguard Cash Plus Account | $0 |

| Money market funds | $3,000 |

| Brokered CDs | $1,000 |

You can flexibly choose based on your fund size. If you want anytime deposits and withdrawals, cash management accounts and some money funds are more suitable. For higher returns, consider fixed deposits but meet higher starting amounts.

Account Opening and Purchase Process

When purchasing USD cash management products on US stock broker platforms, you need to complete the following main steps:

- Submit personal information, including name, Social Security number or taxpayer ID, address, phone, email, date of birth, ID information, employment status, annual income, net worth, investment objectives, investment experience, etc.

- Select account type. You can choose cash account or margin account based on needs.

- Set cash management method. You can choose bank sweep plans, money market funds, or keep funds in the brokerage account.

- Complete account opening application online, by phone, or mail.

After completing account opening, you can directly subscribe to money market funds, buy short-term Treasury ETFs, or select cash management products on the broker platform. The entire process is efficient and convenient, usually completed in a few days. Ensure information is true and complete during operations for smooth compliance review.

Tip: Prepare relevant documents and materials in advance during account opening and purchase to effectively improve efficiency.

Pros, Cons, and Suitable Investor Types

Pros and Cons of Various Products

When choosing wealth management products for idle funds in US stock accounts, you need to understand the main advantages and limitations of each product. The table below compares core pros and cons of money market funds, short-term Treasury ETFs, broker cash management, and USD fixed deposits:

| Product Type | Main Advantages | Main Disadvantages |

|---|---|---|

| Money Market Funds | Returns higher than traditional savings accounts, low risk, strong liquidity, low investment threshold, professional management, diversified investment | Returns affected by market rates, potential liquidity pressure in extreme markets |

| Short-Term Treasury ETFs | High principal safety, strong liquidity, easy trading, low fees | Returns fluctuate with market rates, possible price volatility |

| Broker Cash Management | High convenience, low fees, returns higher than traditional savings, funds available on demand | Limited cash deposits and special banking services, less in-person support |

| USD Fixed Deposits | Yields usually higher than cash products, locked rates, suitable for medium-short term planning | Poor liquidity, penalties for early withdrawal, funds locked |

You can see that money market funds and broker cash management excel in liquidity and convenience. Short-term Treasury ETFs suit users prioritizing principal safety. USD fixed deposits are better for scenarios not needing funds soon and seeking higher returns.

When choosing, balance the pros and cons of different products based on your liquidity, return, and operational convenience needs.

Suitable Investor Types

You can select the most suitable wealth management product based on your fund size, liquidity needs, and risk preference:

- If you want funds available anytime, emphasizing liquidity and easy operation, choose money market funds or broker cash management.

- If you prioritize principal safety and accept some market volatility, short-term Treasury ETFs are appropriate.

- If you have clear fund plans and no short-term need for funds, USD fixed deposits help lock in higher returns.

- If your fund size is small, prioritize low-threshold, high-liquidity products like broker cash management or some money funds.

You can flexibly allocate idle US stock account funds based on your actual situation to balance returns and safety.

US Stock Account Idle Funds Product Comparison Table

When choosing wealth management products for idle funds in US stock accounts, you often need a quick overview of core features of different products. The table below compares mainstream high-yield USD cash products, covering yield, liquidity, risk, investment threshold, and applicable scenarios. You can efficiently select suitable options based on your needs and the table information.

| Product Name/Type | Annualized Yield (2024) | Liquidity | Risk Level | Minimum Investment Threshold (USD) | Applicable Scenario |

|---|---|---|---|---|---|

| Vanguard Federal Money Market Fund | 4.98% | T+1 availability, redeem anytime | Extremely low | 3,000 | Seeking stable returns and high liquidity |

| Fidelity Government Money Market | 4.98% | T+1 availability, redeem anytime | Extremely low | 1 | Flexible management of small funds |

| iShares Short Treasury Bond ETF | 4.7% (floating) | T+1 settlement, intraday trading | Extremely low | 1 share | Principal safety, flexible allocation |

| Schwab Value Advantage Money Fund | 3.77% | T+1 availability, redeem anytime | Extremely low | 0 | No threshold, funds available on demand |

| Broker Cash Management (e.g., Tiger Brokers Idle Cash) | 1%~3% | Real-time transfer in/out | Extremely low | 1 | High-frequency trading, funds anytime available |

| Interactive Brokers Cash Interest | Up to 3.79% | Available anytime | Extremely low | 20,000 (interest threshold) | Larger fund sizes, seeking returns |

| USD Fixed Deposits (brokers/Hong Kong licensed banks) | 4%~5.5% | Not withdrawable before maturity | Extremely low | 1,000 | Funds not needed short-term, lock high returns |

| Moomoo Cash Plus | 3.5%~5.2% | T+1 availability, redeem anytime | Extremely low | 0 | Balancing flexibility and returns |

You can prioritize products with strong liquidity and low thresholds, such as money market funds or broker cash management. For larger fund sizes or funds not needed short-term, USD fixed deposits and high-yield cash management accounts are worth considering. It is recommended to flexibly allocate idle US stock account funds based on your liquidity needs, risk tolerance, and return goals to achieve efficient fund growth.

Investment Recommendations and Notes

Recommendations for Conservative Investors

If you are a conservative investor, prioritize principal safety and liquidity. It is recommended to maintain at least six months of living or operating cash reserves, allocating short-term (0-6 months) funds to savings accounts, checking accounts, money market funds, or U.S. Treasury bills. For 6 months to 3 years funds, choose 12-month fixed deposits, Treasury bills, or short-term bonds. Funds not needed for over three years can consider long-term fixed deposits or fixed-maturity bonds. Through layered cash management, you can balance liquidity and returns while effectively diversifying risks.

- Maintain six months cash reserves

- Place short-term funds in high-liquidity accounts

- Layer mid-to-long-term funds to enhance returns

Liquidity-Priority Recommendations

If you prioritize fund flexibility, choose products with strong liquidity. Money market funds, ultra-short funds, and customized portfolios can meet different liquidity needs. You can refer to the table below:

| Product Type | Features |

|---|---|

| Money Market Funds | Protect principal, strong liquidity, competitive returns |

| Ultra-Short/Short-Term Funds | Diversified cash management options for different liquidity needs |

| Customized Portfolios | Meet specific liquidity and return goals, suitable for institutional clients |

You can place 1-day to 3-month funds in trading-level products, 3- to 12-month funds in strategic level, and 12- to 24-month funds in opportunity-level products, balancing liquidity and returns.

Return-Priority Recommendations

If you pursue higher returns, focus on cash management products with higher annualized yields. For example, US Premium Cash Management Fund currently yields 5.12%. However, note that ETF and mutual fund NAVs fluctuate, and past performance does not guarantee future results. You can enhance overall returns by diversifying across different maturities and types.

| Product Name | Yield | Risk Note |

|---|---|---|

| US Premium Cash Management Fund | 5.12% | NAV fluctuations, returns not guaranteed, monitor market changes |

Risk Warnings

When managing idle funds in US stock accounts, focus on the following risks:

- Avoid over-concentration in a single product or market

- Avoid frequent asset allocation adjustments based on short-term performance

- Understand that “more trading” does not equal “more progress”

- Regularly rebalance portfolios to prevent deviation from goals

Also pay attention to regulatory protections. Vanguard Cash Plus Account and brokered CDs are protected by FDIC insurance, while money market funds in brokerage accounts are protected by SIPC. Choose suitable products based on your needs to ensure fund safety.

When selecting products, prioritize the three key elements of liquidity, risk, and returns, allocate rationally, and avoid common pitfalls.

You can manage idle funds in US stock accounts through various methods like money market funds, short-term Treasury ETFs, broker cash management, and USD fixed deposits. Each product has unique features in safety, liquidity, and returns. The table below briefly compares two mainstream product types:

| Feature | Money Market Funds | Bank Deposits |

|---|---|---|

| Safety | AAA rating | 100% deposit risk in bank bankruptcy |

| Liquidity | Cash available same day | Withdrawals may be restricted |

| Returns | Usually better than short-term bank rates | Possibly lower |

You need to reasonably allocate cash management tools of different maturities based on your risk tolerance, fund usage time, and financial goals. Money market funds and short-term Treasury ETFs provide high liquidity and superior returns, performing strongly during rate fluctuation periods. You should continuously monitor market changes, flexibly adjust wealth management plans, and ensure fund safety and maximum returns.

FAQ

Are wealth management products for idle funds in US stock accounts safe?

Money market funds, short-term Treasury ETFs, and broker cash management products you choose usually have extremely low risk. The U.S. market has strict regulation, with products mainly in high-credit assets. You should still review fund prospectuses and platform compliance information, reasonably diversify funds, and reduce extreme market risks.

How to quickly redeem wealth management products in US stock accounts?

You can directly operate redemptions on broker platforms. Money market funds and cash management products usually settle T+1, short-term Treasury ETFs can be sold intraday with fast settlement. USD fixed deposits require maturity for withdrawal, with partial interest loss for early redemption.

Do wealth management products for US stock accounts have minimum amount requirements?

When choosing money market funds, some products have minimums of USD 1, others USD 3,000. Broker cash management has low thresholds, usually USD 1 to participate. USD fixed deposits and some ETFs have higher minimums; check product details in advance.

Will USD cash product yields fluctuate?

Yields of money market funds and short-term Treasury ETFs you invest in change with Fed rate adjustments. Yields rise when market rates increase; they fall during rate-cut cycles. You can monitor platform announcements and fund NAVs to adjust fund allocation timely.

Can I purchase multiple USD cash management products at the same time?

You can diversify funds across multiple products. This balances liquidity and returns while reducing single-product risk. You can flexibly combine money market funds, Treasury ETFs, and cash management based on fund purposes and maturities to optimize asset allocation.

*This article is provided for general information purposes and does not constitute legal, tax or other professional advice from BiyaPay or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or warranties, express or implied, as to the accuracy, completeness or timeliness of the contents of this publication.

Related Blogs of

How to Understand Futu NiuNiu US Stock Fees? Trading Fees, FX Conversion and Funding Costs

Best US Stock Trading Apps 2025/2026: Fees, Funding and Account Setup

Choose Country or Region to Read Local Blog

Contact Us

BIYA GLOBAL LLC is registered with the Financial Crimes Enforcement Network (FinCEN), an agency under the U.S. Department of the Treasury, as a Money Services Business (MSB), with registration number 31000218637349, and regulated by the Financial Crimes Enforcement Network (FinCEN).

BIYA GLOBAL LIMITED is a registered Financial Service Provider (FSP) in New Zealand, with registration number FSP1007221, and is also a registered member of the Financial Services Complaints Limited (FSCL), an independent dispute resolution scheme in New Zealand.