How to Withdraw $50,000 Daily Without Triggering Risk Controls? Compliant Fiat Off-Ramp Paths for High-Net-Worth Crypto Holders

Image Source: pexels

If you want to smoothly withdraw $50,000 daily without triggering risk controls, you must choose compliant paths. You need to legally prove the source of assets and strictly comply with regulatory requirements in China and relevant jurisdictions. Once you opt for illegal operations, you may face account freezes, fund losses, or even legal risks. Only through compliance and security can you ensure smooth realization of your crypto assets.

Key Points

- Choosing compliant paths is key to ensuring smooth daily withdrawals of $50,000. Follow laws and regulations and avoid illegal operations.

- Understand regulatory policies in different jurisdictions, select compliant and regulated platforms, and ensure fund security.

- Completing KYC and AML requirements is essential for large withdrawals; prepare relevant identity and source-of-funds documentation.

- Reasonably plan withdrawal frequency and amounts, use batch operations to reduce risk control triggers and ensure smooth fund flows.

- Maintain transparency and compliance, regularly organize transaction records, promptly declare taxes, and avoid legal risks.

Compliance Principles and Regulatory Requirements

Compliant Cash-Out Logic

When conducting large-scale crypto asset realization, you must follow a clear compliance logic. Compliance is not just about meeting regulatory requirements but also the key to protecting your asset security. You need to focus on the following core elements:

- Strong legal framework: Choose platforms protected by law to ensure asset security.

- Layered liquidation model: Platforms should have transparent liquidation mechanisms to reduce risks.

- Fiat channels: Platforms must support smooth conversion of crypto assets to fiat currencies like USD and direct transfer to personal bank accounts.

- Regulatory compliance: Prioritize platforms operating in jurisdictions with clear regulation.

- Capital efficiency: Pay attention to the platform’s loan-to-value (LTV) ratio to improve liquidity.

Only by operating on these foundations can you achieve the goal of withdrawing $50,000 and effectively avoid risk controls.

Major Regulatory Policies

Regulatory policies for cryptocurrencies continue to improve across countries. When choosing cash-out paths, you must understand the legal status and exchange requirements in different jurisdictions. The table below compares major policies in the United States, Singapore, and the EU:

| Jurisdiction | Crypto Legal Status | Crypto Exchange Requirements |

|---|---|---|

| United States | Not considered legal tender | Legal, with varying state-level regulation |

| Singapore | Not considered legal tender | Legal, requires registration with MAS |

| EU | Widely accepted legally | Varies by member state |

You need to select compliant and regulated platforms based on your needs to ensure safe fund circulation.

AML and KYC Requirements

When conducting large crypto asset withdrawals, you must strictly comply with KYC (Know Your Customer) and AML (Anti-Money Laundering) regulations. Regulatory bodies such as the U.S. Treasury require financial institutions to conduct compliance reviews on crypto transactions. Platforms violating AML rules face fines and may impact banking partnerships. Major exchanges typically set different KYC tiers based on withdrawal amounts:

| Tier Level | Requirements | Daily Withdrawal Limits |

|---|---|---|

| Tier 2 | - Government-issued photo ID (passport, national ID, driver’s license) * Live check (selfie or video confirming holder matches photo) * Address verification (utility bill, bank statement, or government document from last 3 months) |

$10,000-$50,000 |

| Tier 3 | - All Tier 2 requirements * Source of funds documents (pay stubs, tax returns, business documents) * Source of wealth statement * Enhanced ongoing monitoring |

$100,000+ |

Only by completing the corresponding identity verification and document submission can you successfully complete large withdrawals.

Asset Proof

In the compliant realization process, proof of asset source is fundamental. You need to prepare pay stubs, tax returns, business contracts, and other documents to prove the legitimate origin of crypto assets. Regulators will require detailed transaction records and source-of-wealth statements. You should organize all materials in advance to respond quickly during reviews and reduce the probability of risk control triggers.

Only under the premise of compliance and transparency can you achieve efficient and secure crypto asset realization, ensuring free flow of funds.

Compliant Paths for Withdrawing $50,000

Image Source: pexels

If you want to smoothly withdraw $50,000 daily, you must choose compliant and efficient realization paths. Different paths suit different scenarios, with varying compliance requirements and security measures. The following details mainstream compliant paths to help you choose based on your needs.

Compliant Exchanges

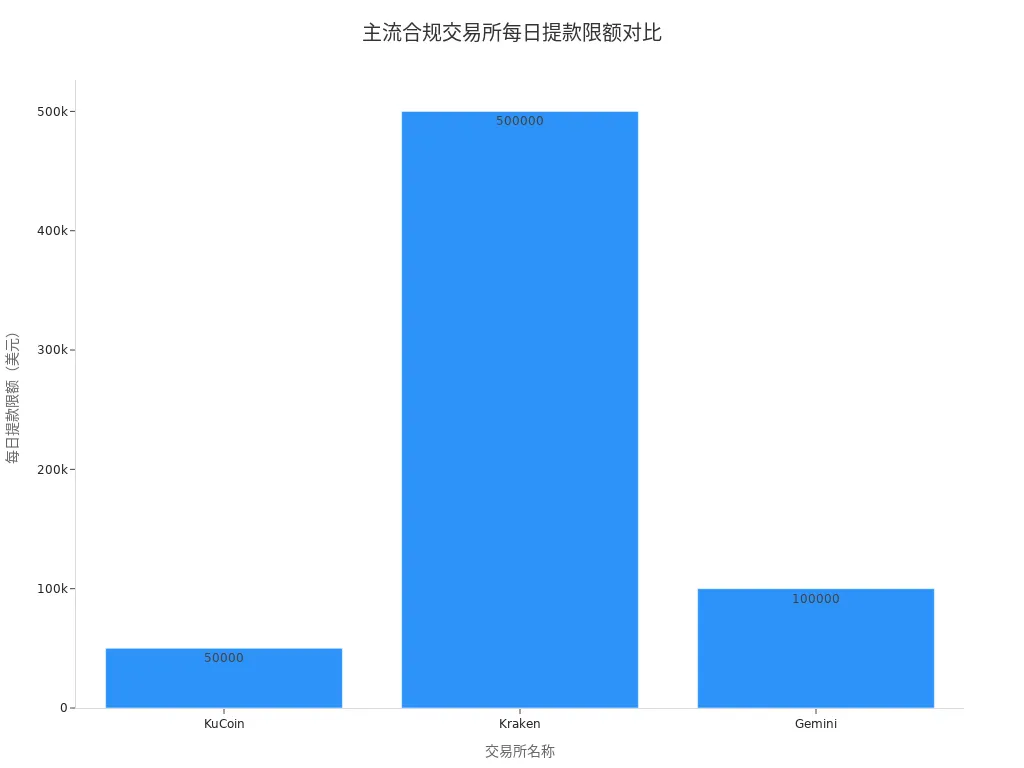

Compliant exchanges provide the most direct way to withdraw $50,000. Major platforms such as KuCoin, Kraken, and Gemini support large withdrawals with transparent compliance processes. After completing advanced KYC on these platforms, you can enjoy higher daily withdrawal limits. The table below shows daily withdrawal limits and specific requirements for several major exchanges:

| Exchange | Daily Withdrawal Limit | Specific Requirements |

|---|---|---|

| KuCoin | $50,000 | Users can buy or sell crypto with fiat; daily limit $50,000, up to $100,000 when purchasing with bank card. |

| Kraken | $500,000 | Intermediate verification users have $500,000 daily withdrawal limit; Pro accounts enjoy higher freedom. |

| Gemini | $100,000 | U.S. clients using ACH bank transfers have $100,000 daily limit; other methods have lower limits. |

When selecting an exchange, prioritize the platform’s compliance qualifications, withdrawal speed, and service fees. Some platforms support docking with Hong Kong licensed bank accounts, allowing funds to settle directly to personal accounts and improving circulation efficiency. You can also refer to compliant service providers like Biyapay for more flexible fiat channels and multi-currency support.

OTC Desk Trading

OTC (Over-the-Counter) trading suits large crypto asset realization under special needs. You can negotiate directly with buyers or sellers via OTC platforms, flexibly arranging transaction times and asset pairs. OTC trading has the following advantages and risks:

- Advantages:

- Strong confidentiality, protecting buyer/seller identity information.

- Customized transactions, supporting multiple payment methods and currencies.

- Large trades do not impact market prices, reducing slippage risk.

- Risks:

- Counterparty default, potentially causing fund or asset loss.

- Regulatory policy changes; continuously monitor local compliance requirements.

- Operational and fraud risks; choose reputable OTC platforms.

During OTC trading, always select platforms with strict KYC/AML processes and prioritize security measures like cold storage and two-factor authentication. Some platforms also offer freeze-compensation services to reduce losses from disputes.

Third-Party Custody

Third-party custody suits scenarios with extremely high asset security requirements. You can custody crypto assets with regulated independent institutions, enjoying professional security and compliance services. Key features of third-party custody include:

- Assets segregated from custodian accounts, preventing commingling risk.

- Cold storage and multi-signature technology to enhance security level.

- Institutional-grade operation permission management and audit logs.

- Legal remedies and rights protection in case of disputes.

When choosing third-party custody, focus on service fees (typically 0.1%-0.5%/year) and withdrawal processes. Some custodians support docking with Hong Kong licensed bank accounts, facilitating compliant $50,000 withdrawals. Service providers like Biyapay can also offer customized custody and realization solutions for Chinese-speaking users.

Cross-Border Payment Solutions

If you need to remit realized crypto funds to overseas accounts, choose compliant cross-border payment solutions. Mainstream options include settlement via Hong Kong licensed banks, international payment companies, or compliant payment platforms. When operating, note:

- Clearly state fund purpose and prepare relevant materials (contracts, invoices, etc.) in advance.

- Suggest controlling single transactions at lower amounts, batch withdrawing $50,000 to reduce risk control probability.

- Prioritize platforms supporting multi-currency and multi-region settlement to improve fund liquidity.

You can also combine compliant services like Biyapay for higher arrival efficiency and lower exchange costs.

Path Comparison

Different compliant paths vary in compliance requirements, security controls, and applicable scenarios. The table below briefly compares mainstream paths:

| Platform Type | Compliance Requirements | Security Controls |

|---|---|---|

| OTC Desk | Strict KYC/AML procedures, identity verification and transaction monitoring | Cold storage, two-factor authentication, IP whitelist |

| Third-Party Custodian | Strict compliance standards | Multi-signature wallets, hardware security modules |

| Crypto Exchange | Depends on platform policy, usually advanced KYC required | Platform’s own risk control system |

In practice, you can flexibly combine multiple paths based on withdrawal frequency of $50,000, fund security needs, and compliance convenience. For example, first complete KYC on a compliant exchange, then batch withdraw via OTC and third-party custody, and finally settle funds through Hong Kong licensed banks. Prioritize local small bank cards to diversify risk and avoid frequent large inflows/outflows on a single account triggering controls.

Tip: When selecting compliant paths, focus on the platform’s compliance qualifications, service fees, and fund arrival speed. Reasonably plan the rhythm of $50,000 withdrawals to ensure asset security and free fund flow.

If you are still comparing routes, it can help to first review what asset types, funding methods, and account connections a platform actually supports before moving into execution. A practical starting point is the BiyaPay website or its trading entry page. In large compliant off-ramp scenarios, checking supported scope first usually makes it easier to judge whether the platform fits your KYC tier, source-of-funds documentation, and receiving-bank setup.

BiyaPay is better understood as a multi-asset wallet, with common use cases covering currency conversion, cross-border payments, and unified management across digital assets, US stocks, and Hong Kong stocks. If fiat settlement or later outbound transfers are also part of your plan, its remittance service can be reviewed as part of the overall path, provided your documentation is complete, the purpose of funds is clear, and the flow remains compliant in the relevant jurisdiction.

Operation Process and Risk Control

Image Source: pexels

KYC and Identity Verification

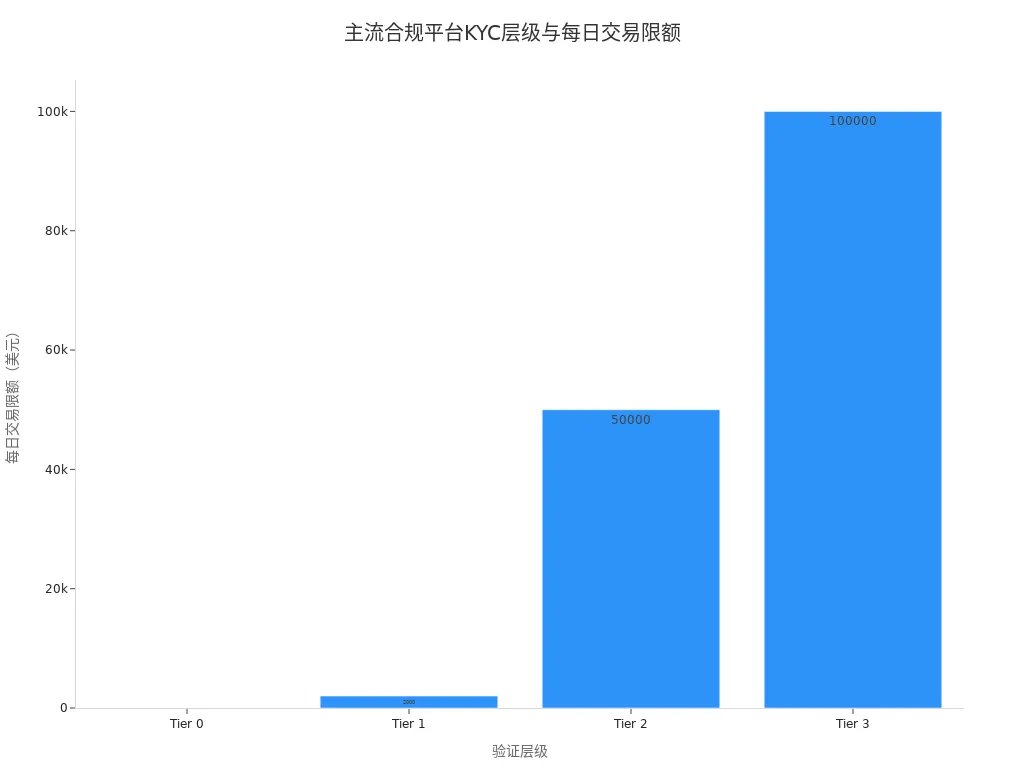

When conducting large-scale compliant crypto realization, first complete the KYC (Know Your Customer) and identity verification process. Major compliant platforms require submission of corresponding identity materials based on different verification tiers. Refer to the table below to understand required documents per tier and corresponding transaction limits:

| Verification Tier | Required Documents | Transaction Limits |

|---|---|---|

| Tier 0 | No documents required | None |

| Tier 1 | Email and phone verification, full name, date of birth, country of residence | Daily $1,000-$2,000, monthly $5,000-$10,000 |

| Tier 2 | Government-issued photo ID, live check, address verification | Daily $10,000-$50,000, monthly $100,000-$500,000 |

| Tier 3 | All Tier 2 requirements, source of funds documents, source of wealth statement | Daily $100,000+, monthly $1,000,000+ or unlimited |

After completing Tier 2 or higher verification, you can meet the $50,000 withdrawal limit requirement. The identity verification process typically includes uploading ID proof, address proof, liveness detection, etc. Platforms will manually or automatically review materials to ensure authenticity and validity.

Batch Withdrawals and Limit Management

In actual operations, reasonably plan withdrawal frequency and single-transaction amounts. It is recommended to control single amounts at a few thousand dollars, completing withdrawals in batches to reduce the probability of triggering risk controls. Prioritize local small bank cards or Hong Kong licensed bank accounts to diversify fund flows and avoid frequent large inflows/outflows on a single account.

When performing high-frequency operations or multi-account collaboration, note the following:

- Avoid multiple large fund inflows to the same bank account within the same period.

- Reasonably schedule withdrawal times, stagger peak periods, and reduce attention from banks and platforms.

- Regularly check transaction records across accounts to ensure all fund flows have legitimate sources and purpose explanations.

Through scientific limit management, you can effectively improve fund flow efficiency while reducing risk control risks.

Fund Purpose and Documentation

In the compliant realization process, you must prepare fund purpose explanations and related materials in advance. Regulators and banks typically require contracts, invoices, transaction records, etc., to prove the legitimacy and reasonableness of funds. Organize materials by actual use, for example:

- Investment income: Provide investment agreements, profit distribution explanations.

- Labor remuneration: Provide service contracts, payment vouchers.

- Asset transfer: Provide transfer agreements, receipt/payment records.

Preparing these materials in advance allows quick response during bank or platform reviews, improving approval rates.

Cold Wallets and Multi-Sig

When managing large crypto assets, prioritize cold wallets and multi-signature technology to enhance asset security. Cold wallets isolate private keys in offline environments, effectively preventing hacker attacks. Multi-signature wallets require multiple private keys to co-sign transactions, further dispersing risk. Specific advantages include:

- Multi-signature wallets require two or more private keys to sign and send transactions, effectively dispersing access control and reducing unauthorized transaction risks.

- Assuming three holders, transactions can only proceed with at least two signatures, preventing losses from a single holder’s mistake or malicious behavior.

- This method is similar to a bank vault, which can only be opened with multiple keys, thereby enhancing security.

Adopting cold wallet and multi-sig solutions can significantly improve asset security during large $50,000 withdrawals.

Transaction Records and Reporting

In compliant operations, you must fully retain all transaction records and report large withdrawals to regulators as required. Compliant platforms continuously monitor transactions to identify suspicious activity. Note:

- You should maintain accurate records of all customer information, transaction flows, and AML compliance activities.

- You are obligated to cooperate with platforms in reporting any suspicious transactions or activities to relevant authorities, assisting in investigations and preventing money laundering and other financial crimes.

- Regularly organize and back up transaction data to provide timely information during regulatory inspections.

Through standardized record-keeping and reporting processes, you can effectively avoid legal risks and safeguard fund security.

Bank Account Management

When managing bank accounts, prioritize compliant financial institutions such as Hong Kong licensed banks, diversify fund flows, and enhance security. Bank transfer solutions across different platforms vary in fees, limits, and arrival times. The table below compares mainstream solutions:

| Method | Fee | Limit | Typical Processing Time |

|---|---|---|---|

| Standard bank transfer | 0.1%-0.3% | $20 min / $100,000 max | 30 minutes – 2 business days |

| Bank withdrawal | 0.2%-0.5% | $100 min / $50,000 max | 1–5 business days |

| Fiat withdrawal | 0.1%-0.4% | $10 min / $100,000 max | 15 minutes – 2 business days |

When withdrawing cryptocurrency, you must complete KYC verification to ensure authentic identity information. Based on fund scale and arrival needs, flexibly choose different bank accounts and transfer methods, reasonably diversify funds, and reduce the probability of single-account risk control.

Tip: Throughout the entire operation process, maintain compliance and transparency, strictly follow regulatory requirements at every step, and ensure smooth and secure arrival of $50,000 withdrawals.

Risks and Common Issues

Risk Control Trigger Reasons

Common risk control triggers during large crypto asset withdrawals include:

- High-risk fund inflows, such as from anonymous wallets or addresses under regulatory scrutiny.

- Purchasing crypto on behalf of others, easily suspected as nominee holding or money laundering.

- Withdrawals for high-risk uses like gambling, closely monitored by banks and platforms.

- Offline transactions lacking transparent records, increasing compliance risk.

- Assisting suspicious individuals in money laundering, involving criminal liability.

If involved in the above behaviors, you are highly likely to face bank or exchange risk controls, leading to account freezes or delayed fund arrivals.

Consequences of Violations

Once you violate compliance requirements, you may face serious legal and financial consequences. The table below shows typical cases in major jurisdictions:

| Type | Example | Impact |

|---|---|---|

| Regulatory fine | CB Payments Limited fined £3.5 million by UK FCA in 2024 | Company financial loss and reputational damage |

| Average fine | Average fine for crypto firms due to AML non-compliance in 2025: $3.8 million | Industry-wide compliance risks |

| Total fine amount | Crypto firms faced over $5.1 billion in fines in 2024 for inadequate AML programs | Severe financial consequences for non-compliance |

You should also pay attention to real cases such as PlusToken, FTX, MT.Gox, etc. These incidents not only caused huge losses but also drove stricter global regulation. For example, the FTX collapse caused $8-10 billion in losses, with the founder convicted and regulators strengthening exchange governance.

Handling Account Freezes

If your account is frozen, it is recommended to take the following measures:

- Proactively contact platform or bank customer service, explain transaction details thoroughly.

- Understand the freeze reason and obtain official explanation.

- Supplement identity verification materials as required to prove source and purpose of funds.

- When necessary, submit Suspicious Activity Reports (SAR) to relevant institutions and cooperate with investigations.

Maintaining communication and cooperation helps accelerate the unfreezing process and reduce fund loss risks.

Anti-Fraud and Information Security

During large withdrawals, attach great importance to anti-fraud and information security. The following measures can effectively reduce risks:

- Multi-layer verification to ensure every character in the receiving address is accurate.

- Use wallet address book to avoid errors from manual copy-paste.

- Enable withdrawal address whitelist; multi-factor verification required for first transfers to new addresses.

- Conduct small test transactions first to confirm address correctness before large transfers.

- Maintain device security, regularly update antivirus software, avoid installing unknown plugins, and use dedicated devices for crypto operations.

Through these measures, you can effectively prevent phishing, theft, and other security incidents, safeguarding asset security.

Tax Compliance

In the crypto asset realization process, focus on tax compliance. Major markets like the United States treat cryptocurrency as taxable assets, requiring declaration of capital gains and related income. You should proactively retain transaction records and promptly declare to tax authorities to avoid legal risks from tax evasion. Compliant declaration not only facilitates smooth fund flows but also provides convenience for subsequent asset allocation and cross-border operations.

Only by adhering to compliant operations can you achieve fund security and free flow in a complex regulatory environment, avoiding uncontrollable risks from violations.

In the process of large-scale compliant crypto realization, you must prioritize compliance and security. Continuously monitor regulatory developments and choose qualified professional service institutions such as BNY Mellon, State Street, DBS Bank, and Safeheron to ensure every step meets the latest requirements. You can refer to the following risk management strategies:

| Risk Management Strategy | Description |

|---|---|

| Portfolio diversification | Diversify investments to reduce single-point failure risk |

| Stop-loss orders | Timely stop losses to control potential losses |

| Security best practices | Use hardware wallets, two-factor authentication, etc., to protect assets |

You must also strictly implement identity verification, transaction limits, address whitelists, and regular security audits to ensure asset security and free fund flow.

FAQ

How to choose a compliant cryptocurrency trading platform?

You should prioritize the platform’s regulatory qualifications, KYC process, withdrawal limits, and service fees. Mainstream platforms in markets like the United States and Singapore usually have comprehensive compliance systems to effectively safeguard fund security.

What documents will the bank require when withdrawing $50,000?

You need to provide identity proof, source-of-funds proof, transaction records, and fund purpose explanations. Banks will review materials according to regulatory requirements to ensure every fund flow is legal and compliant.

Will frequent large withdrawals cause account freezing?

If you frequently make large withdrawals, bank and platform risk control systems may trigger alerts. You should reasonably batch operations, diversify accounts, and reduce the probability of risk control.

Do I need to declare taxes after realizing crypto assets?

Major markets like the United States require truthful declaration of crypto realization proceeds. You should retain complete transaction records and promptly declare to tax authorities to avoid legal risks from tax evasion.

Is OTC off-chain trading safer than exchanges?

OTC trading is flexible but carries higher risks. You should choose platforms with compliant qualifications, strictly implement KYC and AML processes, and prioritize third-party custody to reduce counterparty default and fraud risks.

*This article is provided for general information purposes and does not constitute legal, tax or other professional advice from BiyaPay or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or warranties, express or implied, as to the accuracy, completeness or timeliness of the contents of this publication.

Related Blogs of

How to Understand Futu NiuNiu US Stock Fees? Trading Fees, FX Conversion and Funding Costs

Best US Stock Trading Apps 2025/2026: Fees, Funding and Account Setup

What Are After-Hours Pricing and After-Hours Odd-Lot Trading? Rules, Fees, and Use Cases

Choose Country or Region to Read Local Blog

Contact Us

BIYA GLOBAL LLC is registered with the Financial Crimes Enforcement Network (FinCEN), an agency under the U.S. Department of the Treasury, as a Money Services Business (MSB), with registration number 31000218637349, and regulated by the Financial Crimes Enforcement Network (FinCEN).

BIYA GLOBAL LIMITED is a registered Financial Service Provider (FSP) in New Zealand, with registration number FSP1007221, and is also a registered member of the Financial Services Complaints Limited (FSCL), an independent dispute resolution scheme in New Zealand.