Creating a Will for Your Digital Wealth: How to Safely Pass Overseas Accounts and Digital Assets to Your Family in Case of Unexpected Events

Image Source: unsplash

Do you want your family to smoothly inherit your overseas accounts and digital assets? A digital wealth will can help you plan ahead, designate heirs, and securely store access information. You need to understand that failing to plan in advance brings serious risks, including asset loss, inheritance disputes, and legal barriers. For example, many third-party platforms require inheritance certificates or will probate documents, overseas service providers are often subject to foreign laws, and self-custodied wallets require control of private keys or seed phrases. Only by making arrangements in advance can your family truly take control of your digital wealth.

Core Key Points

- Plan a digital wealth will in advance to ensure your family can smoothly inherit your overseas accounts and digital assets.

- Understand the differences between digital assets and traditional assets, create a detailed asset inventory, and ensure your family can quickly locate and manage these assets.

- Choose trustworthy heirs and executors who have the ability and experience to manage digital assets.

- Regularly review and update your digital asset inventory to maintain accuracy and availability of information, avoiding financial losses due to outdated information.

- Use password managers and cold storage methods to ensure the security of access information and prevent hacker attacks and information leaks.

The Importance of a Digital Wealth Will

Image Source: unsplash

Differences Between Digital Assets and Traditional Assets

When planning your estate, you must recognize that digital assets and traditional assets have fundamental differences. Digital assets include cryptocurrencies, NFTs, cloud files, social media accounts, etc. The transfer of these assets faces unique challenges:

- Digital assets are ephemeral and can easily become unrecoverable due to data corruption or loss.

- You need exclusive control, such as private keys or passwords; otherwise, it is difficult for your family to inherit them.

- The relevant legal framework is still immature, and inheritance procedures are often inconsistent.

- You must establish a detailed asset inventory and take security measures, whereas traditional physical assets do not require such complex management.

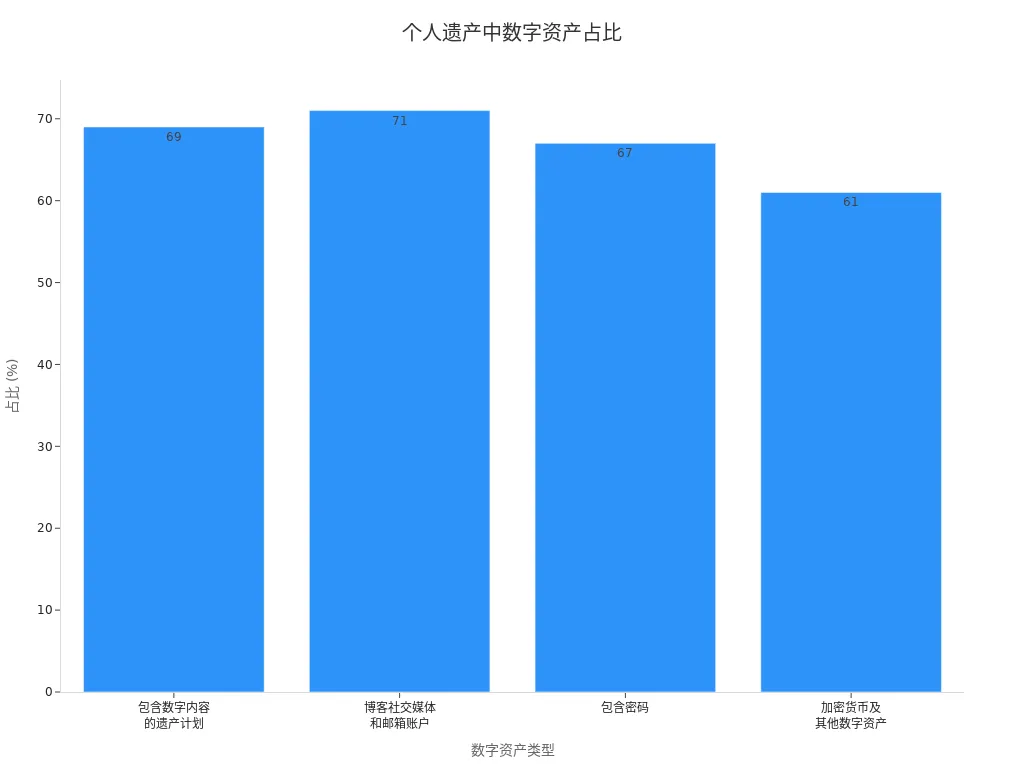

You can see from the chart below that more than 60% of personal estate plans already include digital content, social media, cryptocurrencies, and other digital assets:

Risks and Consequences of Inheritance

If you do not create a digital wealth will in advance, your family may face the following risks:

- Financial loss: Cryptocurrencies and online business assets may become permanently inaccessible.

- High legal costs: On average, $50,000 to $400,000 USD in court fees are required to establish access rights to digital assets.

- Emotional trauma: Family photos, letters, and digital memories may be lost forever.

- Identity theft risk: Unmanaged accounts easily become targets for cybercriminals.

- Heirs may not receive all the funds you wish to leave them, and social media accounts may remain unmanaged for a long time.

If you ignore digital asset inheritance planning, executors will find it difficult to locate and access these assets, ultimately resulting in assets that cannot deliver real value to your family.

The Significance of Digital Cultural Heritage

Digital cultural heritage is not just economic assets; it also carries your life memories and cultural value. International institutions such as UNESCO have included digital objects such as databases, websites, software, texts, videos, and photography in the scope of cultural heritage protection. You can refer to the table below to understand the legal and protection principles of digital cultural heritage:

| Evidence Type | Description |

|---|---|

| International Documents | UNESCO points out that digital heritage objects include databases, websites, software, texts, videos, and photography, which have cultural value and require legal protection. |

| Intellectual Property Challenges | The legal protection of intellectual property for digital heritage is a major challenge, with discussions focusing on how to formulate laws that promote rather than hinder its protection. |

| Cultural Heritage Protection Principles | International cultural heritage protection is based on a series of definitions, principles, and guidelines aimed at protecting tangible and intangible cultural property. |

By creating a digital wealth will, you can not only protect your family’s economic interests but also ensure that your digital cultural heritage is properly inherited and preserved.

Digital Wealth Inventory and Classification

Sorting Digital Asset Types

When planning your digital wealth, the first step is to sort through all your digital assets. Common types include:

- Social media accounts (e.g., WeChat, Facebook, Twitter)

- Bank accounts (domestic and overseas)

- Streaming service accounts (e.g., Netflix, Spotify)

- Mobile carrier accounts

- Cryptocurrencies (e.g., Bitcoin, Ethereum, USDT, etc.)

- Electronic devices and their passwords (e.g., Apple ID)

- Email accounts

- Online shopping accounts (e.g., Amazon)

- Online payment and asset management platforms (e.g., BiyaPay, supporting global payments, fiat-to-cryptocurrency exchange, USDT to USD/HKD, stock fund management, cryptocurrency trading)

You need to categorize these assets, recording the name, location, username, associated email, and approximate value of each item. This will help you or your family quickly locate and manage them when needed.If your digital estate also includes cross-border payment or investment accounts, it is better not to record only that the account exists. You should go one step further and distinguish the account’s function, asset type, and the access materials your family may later need. A platform such as BiyaPay, positioned as a multi-asset trading wallet, may simultaneously involve fund management, digital assets, conversion, and investment access. If heirs know only the platform name but not the asset types inside the account, the handover process becomes harder.

A more practical method is to record that type of platform account by function, such as whether it involves an exchange-rate comparison tool, stock information lookup, or other fund-transfer scenarios, while also organizing login methods, linked email addresses, and device-verification requirements. The goal is not to add unnecessary detail, but to reduce the heir’s difficulty in understanding an account that mixes cross-border and digital asset functions.

Overseas Accounts and Online Assets

Inheritance of overseas accounts is more complex than domestic Chinese accounts. You need to pay attention to:

- Inheritance of overseas accounts involves multiple reporting obligations, especially when the accounts belong to an estate or trust.

- U.S. trustees and beneficiaries must comply with FBAR reporting requirements; if the estate and all trustees and beneficiaries are non-U.S. persons, the FBAR obligation may terminate upon death.

- If multiple U.S. heirs jointly inherit an overseas account, their respective reporting obligations need to be coordinated to avoid penalties due to inconsistent filings.

When using BiyaPay and other global payment and cryptocurrency exchange platforms, you should also pay attention to relevant compliance requirements to ensure smooth asset inheritance.

Digital Cultural Heritage and Materials

Digital cultural heritage includes your photos, videos, documents, websites, blogs, etc. These materials carry personal memories and cultural value. You should include these materials in the inventory along with economic digital assets, clearly stating how you want your family to handle them: transfer, memorialize, or delete.

Asset Location and Reminders

You can help your family locate and manage digital assets in the following ways:

- Create a detailed digital asset inventory, categorizing and recording asset information.

- Clearly specify access and disposal methods for digital assets in your will or trust.

- Use a password manager to automatically record information for various accounts.

- Do not overlook physical devices that store digital assets, such as smartphones, tablets, computers, external hard drives, USB drives, etc.

Tip: California’s Revised Uniform Fiduciary Access to Digital Assets Act (RUFADAA) authorizes executors to access and manage digital assets. You can set up “online tools” in your will or trust to provide your family with access guidance and reduce the difficulty of locating assets.

Designation and Allocation in a Digital Wealth Will

Choosing Heirs and Executors

When creating a digital wealth will, choosing appropriate heirs and executors is crucial. Digital asset management and inheritance are more complex than traditional assets, involving passwords, private keys, platform rules, and many other factors. You should prioritize people who are familiar with digital asset operations, especially relatives, friends, or professionals with practical experience in cryptocurrencies and global payment platforms (such as BiyaPay).

When selecting an executor, you can refer to the following criteria:

- Trustworthiness: You need to choose someone you completely trust, as the executor will have access to your assets and sensitive information.

- Organizational ability: The executor should be methodical and capable of managing multiple tasks and documents.

- Financial literacy: A certain level of financial knowledge helps with asset management.

- Willingness to serve: The executor must be willing and able to take on responsibility.

- Impartiality: If your estate distribution may cause disputes, an impartial executor can reduce conflicts.

- Geographic location: A local executor is more convenient for handling affairs, but digital assets can be managed remotely, so location has less impact.

- Age and health: Choosing a younger, healthier executor reduces the risk of replacement.

You can compare these criteria with family, friends, or professionals to ultimately determine the most suitable candidate. For Chinese-speaking users, if your digital assets involve global payment and cryptocurrency platforms such as BiyaPay, it is recommended to prioritize an executor familiar with the relevant business processes to ensure smooth asset inheritance.

Tip: You can clearly designate a digital asset executor in your will or trust and authorize them to access and manage the relevant accounts. This can reduce legal barriers and enhance asset security.

Asset Allocation and Access Methods

You need to develop clear allocation and access plans for each type of digital asset. A digital wealth will should not only specify asset ownership but also detail access methods. You can take the following measures:

- Specify access permissions: Provide each heir with the necessary usernames, passwords, or private keys to ensure they can log in and manage accounts smoothly.

- Utilize legacy contacts: Some platforms (such as BiyaPay) allow you to set beneficiaries or legacy contacts, facilitating automatic asset transfer after your death.

- Configure external sharing: You can centrally store important files in cloud storage and authorize family members or executors to access them. For example, store BiyaPay account information, transaction records, etc., in an encrypted cloud drive.

- Embed instructions in the will: You should clearly state the allocation and access process for each digital asset in your will or trust documents to avoid subsequent disputes.

- Separate reference file: You can create a dedicated digital asset allocation inventory that lists various assets and their access methods in detail for easy executor operation.

You should also communicate regularly with your family to ensure they understand your asset distribution and access procedures. The value of digital assets may change over time, and some accounts may depreciate or be lost quickly if left inactive for a long period. You should review the asset inventory and security measures at least once a year to ensure the information is accurate and available.

Recommendation: You can adopt a three-layer approach to manage digital asset inheritance—prioritizing online tools (such as BiyaPay’s beneficiary function), written consent (will/trust), and supplementing with court orders when necessary. This can maximize asset security and inheritance efficiency.

Electronic Wills and Trust Documents

You can ensure the legal inheritance effect of digital assets through electronic wills and trust documents. Many countries and regions have enacted relevant laws allowing executors and trustees to access and manage digital assets. For example, California has adopted the Revised Uniform Fiduciary Access to Digital Assets Act (RUFADAA), authorizing executors to access digital assets based on instructions in wills, trusts, or online tools.

The table below shows the digital asset inheritance legal frameworks in some countries/regions:

| Country/Region | Legal Framework | Main Cases |

|---|---|---|

| Germany | Digital accounts are considered “property rights” and can be inherited | German Federal Court ruling |

| United States | RUFADAA authorizes executors to access digital assets | California-related cases |

| Singapore | Reference to trust law and electronic will regulations | Singapore High Court precedents |

When creating a digital wealth will, you should pay attention to the following points:

- Clearly authorize trustees in the will or trust to manage digital assets, covering restrictions in platform terms of service.

- Make full use of online tools on platforms such as BiyaPay to set beneficiaries or legacy contacts and improve asset transfer efficiency.

- Understand the terms of service of each platform; some platforms may restrict asset transfer or access and require advance planning.

- Use electronic will notarization, online platform storage, and other methods to ensure documents are secure, legal, and easily accessible.

Note: If you do not include digital asset provisions in your will or trust, your loved ones may be unable to access your important accounts and materials due to lack of authorization, and may even face legal obstacles. You should complete the relevant documents as early as possible to protect your family’s rights.

Designation and allocation in a digital wealth will is the core link in digital asset inheritance. Only by planning ahead, allocating scientifically, and authorizing legally can you ensure that your digital wealth truly benefits your family and avoid asset loss due to missing information or legal barriers.

Secure Storage and Transfer of Access Information

Image Source: unsplash

Password Management and Cold Storage

When managing digital assets, you must adopt high-strength password strategies. It is recommended that each password contain at least 12 characters, mixing uppercase and lowercase letters, numbers, and special symbols. You can use a password manager to centrally store information for various accounts, but for cryptocurrency wallets and important platforms (such as BiyaPay), cold storage is recommended. Cold storage refers to keeping sensitive information such as private keys and seed phrases offline, commonly using hardware wallets and paper backups. Cold storage offers extremely high security and can effectively prevent hacker attacks and network leaks. You can refer to the table below to understand the advantages and disadvantages of cold storage:

| Advantages | Disadvantages |

|---|---|

| Excellent security, offline storage of private keys to prevent online threats | Physical vulnerability, risk of loss or damage |

| Full control of private keys without relying on third parties | Inconvenient for frequent trading, more operational steps |

| Protection from exchange risks | Higher initial cost, hardware wallets priced at 50-200 USD |

| Suitable for long-term holding of large amounts of assets | Complex for beginners, requires careful management |

You should avoid storing seed phrases or private keys electronically in the cloud or email to reduce the risk of information leakage.

Legacy Contacts and Trust Mechanisms

In digital wealth inheritance, you should designate one or more legacy contacts. Legacy contacts need to have experience in digital asset management and can assist your family in accessing and allocating assets in case of unexpected events. You can enhance security through trust mechanisms. Trust mechanisms include platform trust (such as trust in blockchain protocols), peer trust (trust in trustees or family members), and dApp trust (trust in decentralized applications). The table below shows the main components of trust mechanisms:

| Trust Mechanism Component | Description |

|---|---|

| Platform Trust | Trust in blockchain protocols |

| Peer Trust | Trust in other users and service providers |

| dApp Trust | Trust in decentralized applications |

You can distribute part of the access information, using multi-signature or segmented backups to reduce single points of failure.

Asset Privacy and Security Assurance

When inheriting digital assets, you must attach great importance to information privacy and security. It is recommended to maintain an encrypted asset inventory, back up seed phrases or private keys for all wallets, and ensure the absolute privacy of backup information. Anyone who obtains a private key or seed phrase can directly transfer your assets. You should eliminate the risk of personal devices and cloud services as the sole point of failure and avoid relying on a single device or cloud server. You also need to pay attention to platform privacy policies and terms of service, as some platforms may restrict asset transfer or access, and even inheritance rights may be limited due to legal changes. You can regularly update the asset inventory and security measures to ensure your family can smoothly inherit your digital wealth under legal and compliant conditions.

Key Points for Inheriting Different Asset Types

Self-Custodied Wallet Inheritance

When inheriting self-custodied wallets, you need to take multiple measures to ensure asset security. You can use services like Bron to assist in transferring ownership of self-custodied wallets. You should designate guardians in advance to ensure inheritance requests are verified. You must comply with a mandatory six-month delay to prevent misoperation or illegal transfer of assets. You should avoid using automatic transfers and “dead man’s switches” as these mechanisms may introduce security risks. You can store private keys and seed phrases using cold storage and enhance security through segmented backups via trust mechanisms. When planning, it is recommended to include BiyaPay’s cryptocurrency assets in the will inventory and clearly state the inheritance process to ensure your family can smoothly take over.

Third-Party Platform Account Inheritance

When handling third-party platform accounts, you need to understand each platform’s inheritance policies. Twitter does not allow access to deceased users’ profiles, but you can deactivate the account by providing a death certificate and ID. Facebook will automatically memorialize user profiles, and only immediate family members can request deletion. You can set a legacy contact or choose automatic account deletion. Google provides inactive account management tools, allowing you to designate trusted contacts to receive notifications. Apple allows adding legacy contacts, with access to iCloud data within three years. LinkedIn supports requests from legal rights holders to delete or memorialize accounts. When using global payment platforms such as BiyaPay, it is recommended to set beneficiaries or legacy contacts in advance to ensure smooth asset transfer.

Compliance for Overseas Bank Account Inheritance

When inheriting overseas bank accounts, you must strictly comply with regulatory requirements. Beneficiaries and trustees need to understand reporting responsibilities, especially when accounts were not disclosed by the deceased. If the account belongs to an estate or trust, the personal representative or trustee must report it on their individual FBAR. Any beneficiary with more than 50% beneficial interest must report as the “owner” of foreign financial accounts in the trust or estate. Only U.S. trustees and beneficiaries have FBAR reporting obligations. If undisclosed foreign accounts are evenly divided among multiple U.S. persons, you need to coordinate their respective reporting obligations to avoid penalties due to inconsistent filings. When using licensed Hong Kong banks, it is recommended to consult professionals to ensure legal and compliant asset inheritance.

Operational Recommendations and Regular Updates

Updating Asset Inventory and Access Information

You need to regularly review and update your digital asset inventory. Digital accounts, passwords, and technologies are constantly changing, and only continuous maintenance can guarantee asset security. You can adopt the following strategies:

- Check the asset inventory once a year or every six months, delete closed accounts, and add newly opened accounts.

- Adjust access methods promptly in response to platform changes, for example, pay attention to business updates and security policies for global payment platforms such as BiyaPay.

- Identify your own cybersecurity risks, deploy anti-malware and antivirus systems, upgrade software and hardware, and implement cybersecurity best practices.

- Restrict access permissions and only authorize trusted personnel to manage important files, photos, and databases.

- Regularly back up digital assets using enterprise-grade data backup solutions to prevent asset loss due to misoperation or malicious attacks.

- Audit the asset inventory at annual, semi-annual, quarterly, or monthly frequencies to help identify risky behaviors.

Tip: The asset inventory should be designed to evolve dynamically to adapt to changes in digital life. You can use password managers and cold storage methods to ensure access information is secure and reliable.

Family Communication and Professional Consultation

You need to maintain communication with your family to ensure they understand your digital asset distribution and access procedures. Digital wealth inheritance involves many complex management tasks, and professional advisors can provide you with guidance:

- Professionals will help you record all digital assets to ensure nothing is missed.

- They assist in creating a comprehensive estate plan that includes specific instructions for digital asset transfer.

- You can discuss early planning for digital heritage with advisors to prevent rapid loss of asset value.

- Advisors will research legacy and transfer designation options on various online platforms to help you choose the best solution.

- For global payment and cryptocurrency platforms such as BiyaPay, professional advisors can provide compliance advice to ensure smooth asset inheritance.

Recommendation: You should regularly communicate with your family and professional advisors and update the asset inventory and access information promptly. This can reduce the risk of inheritance disputes and ensure secure digital wealth inheritance.

When creating a digital wealth will, you need to avoid common mistakes such as not including digital assets, not providing access information, and neglecting heir education. You can enhance security by creating secure inventories, using password managers, and designating digital executors. Statistics show that more than 50% of adults worldwide own digital assets, but only 12% make clear arrangements, and 78% of digital assets become permanently inaccessible after the owner’s death. You should regularly review your inheritance plan, comply with legal provisions such as RUFADAA, protect your family’s interests, and reduce financial losses and legal costs.

| Statistic | Description |

|---|---|

| 50% | More than 50% of adults worldwide own digital assets |

| 12% | Only 12% of people make clear inheritance arrangements |

| 78% | 78% of digital assets become inaccessible after death |

FAQ

How to ensure legal validity when creating a will for digital assets?

You need to clearly list digital assets in your will and authorize the executor to access the relevant accounts. It is recommended to consult a professional lawyer to ensure the documents comply with mainland China and overseas legal requirements.

How to designate a beneficiary or legacy contact for a BiyaPay account?

You can set a beneficiary or legacy contact on the BiyaPay platform. The platform supports global payments, cryptocurrency exchange, USDT to USD/HKD, stock fund management, and cryptocurrency trading. The beneficiary can smoothly take over the assets after your death.

How to securely pass cryptocurrency wallet private keys to family members?

You can store private keys using cold storage methods, such as hardware wallets or paper backups. It is recommended to store backup information in segments and inform trusted family members of the access method to avoid information leakage.

What compliance issues should be noted when inheriting overseas bank accounts?

You need to understand the reporting obligations of beneficiaries and trustees, especially FBAR filings. If the account belongs to an estate or trust, the personal representative must report it on their individual FBAR to avoid penalties due to inconsistent filings.

How to arrange the inheritance of digital cultural heritage such as photos and documents?

You can centrally store important photos, videos, and documents in an encrypted cloud drive and specify access permissions in your will. It is recommended to regularly back up materials to ensure your family can smoothly inherit your digital cultural heritage.

*This article is provided for general information purposes and does not constitute legal, tax or other professional advice from BiyaPay or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or warranties, express or implied, as to the accuracy, completeness or timeliness of the contents of this publication.

Related Blogs of

Why Holding Cash Is Inferior to Dividend Stocks: Configuring High-Yield Tech Stocks in a Multi-Asset Wallet

AI-Generated Fake KYC Materials Proliferation: How Financial Platforms Ensure Authenticity and Effectiveness of Real-Name Authentication

The Last Line of Defense in Cross-Border Remittances: Why We Need a 24/7 Online Human Bilingual Customer Service Team

AI Healthcare, AI Legal Advisors: Exploring New U.S. Stock Opportunities After Agent Deployment in Vertical Domains

Choose Country or Region to Read Local Blog

Contact Us

BIYA GLOBAL LLC is registered with the Financial Crimes Enforcement Network (FinCEN), an agency under the U.S. Department of the Treasury, as a Money Services Business (MSB), with registration number 31000218637349, and regulated by the Financial Crimes Enforcement Network (FinCEN).

BIYA GLOBAL LIMITED is a registered Financial Service Provider (FSP) in New Zealand, with registration number FSP1007221, and is also a registered member of the Financial Services Complaints Limited (FSCL), an independent dispute resolution scheme in New Zealand.