Compute Power Anxiety in the AI Era: Beyond NVDA, Which US-Listed Chip Stocks Are Worth Heavy Long-Term Holding?

Image Source: pexels

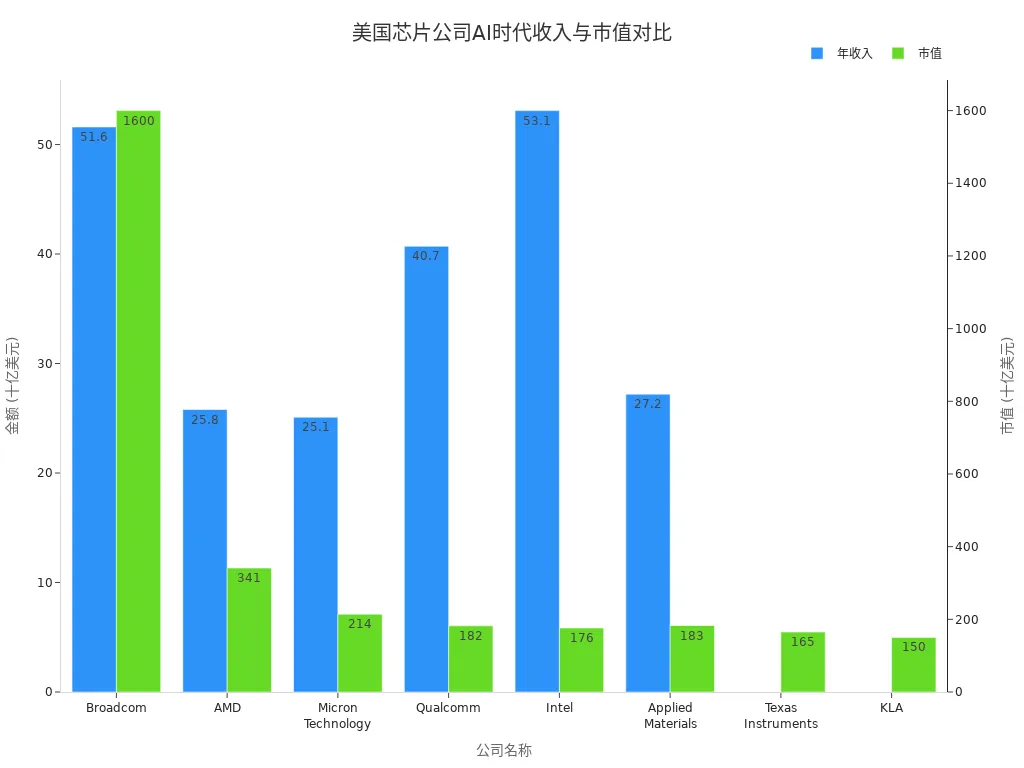

AI technology is driving the world into an era of compute power anxiety. NVIDIA has become the market’s focal point, but the US market features several other chip companies showing impressive growth, such as AMD, Broadcom, TSMC, ASML, and Qualcomm. Data shows these companies not only excel in annual revenue but also rank at the forefront of the industry in market capitalization.

| Company Name | Annual Revenue (Billion USD) | Market Capitalization (Billion USD) |

|---|---|---|

| Broadcom | 51.6 | ~1566 (as of early 2026) |

| AMD | 25.8 | ~314 |

| Micron Technology | 25.1 | ~417 |

| Qualcomm | 40.7 | ~145 |

| Intel | 53.1 | ~217 |

| Applied Materials | 27.2 | ~258 |

| Texas Instruments | N/A | ~176 |

| KLA | N/A | ~177 |

The chip industry landscape continues to evolve, with these companies leveraging technological innovation and business positioning to demonstrate strong competitiveness in the AI wave.

Core Key Points

- AI technology drives explosive growth in compute power demand; investors should focus on companies like AMD, TSMC, and ASML for their robust growth in the market.

- Diversified investment is an effective strategy to reduce risk; investors can allocate across multiple chip companies to cover design, manufacturing, and application segments.

- Pay attention to industry cycles and policy changes; investors need to flexibly adjust asset allocation to address challenges from market volatility and technological iterations.

- AI-related company stock prices fluctuate significantly; investors should maintain a long-term perspective, focusing on corporate financial performance and technological innovation capabilities.

- Over the next five years, the AI chip market will continue to grow; investors should seize this structural opportunity and focus on leading companies in the industry.

New Investment Opportunities Amid Compute Power Anxiety

Image Source: unsplash

Drivers of Surging Compute Power Demand

The rapid development of AI technology has propelled global compute power anxiety. Generative AI, real-time data analysis, and automation applications have become the foundation of modern digital services, with these technologies driving continuously rising demand for computing power. Major US tech companies are increasingly investing in AI development, computer hardware, and new data centers, with related investments expected to exceed $300 billion by 2025. AI’s compute demand growth has far outpaced Moore’s Law, with global compute demand projected to reach 200 gigawatts by 2030. The table below summarizes the main factors driving the surge in compute power demand:

| Source | Main Content |

|---|---|

| AI Infrastructure Era | Artificial intelligence has evolved from a niche technology into the foundation of modern digital services; generative AI, real-time analysis, and widespread automation drive explosive demand for computing power. |

| Powering the AI Era | The AI industry attracted massive investment from late 2022; by 2025, the largest US tech companies are expected to invest over $300 billion in AI development, computer hardware, and new data centers. |

| AI’s insatiable demand for compute power | AI compute demand growth exceeds Moore’s Law; global compute demand is projected to reach 200 gigawatts by 2030. |

The widespread adoption of generative AI technology also imposes higher requirements on data centers and cloud infrastructure. Data center energy consumption has increased significantly, making advanced cooling solutions standard, and power availability has become a key site-selection factor. Compute power anxiety is not only technical but also reflected in capital market investment enthusiasm and high expectations for future returns.

Changes in the Chip Industry Landscape

The global semiconductor industry is experiencing an unprecedented investment boom. Major players like TSMC, Intel, and SMIC continuously adjust strategies to capture emerging markets in AI, 5G, autonomous driving, and quantum computing. TSMC has cumulatively invested over $500 billion, focusing on advanced manufacturing and AI chips. Intel plans to capture 10% of the global foundry market share by 2030, advancing in custom AI and high-performance computing chips. China’s SMIC has increased its market share from 4% to around 5-6%, reducing reliance on foreign suppliers despite US sanctions. The table below shows major companies’ investment directions and target markets:

| Company | Investment Amount | Target Markets |

|---|---|---|

| TSMC | Over $500 billion | AI, 5G, autonomous driving, quantum computing |

| Intel | Aims for 10% foundry market share by 2030 | Custom AI, high-performance computing, enterprise chips |

| SMIC | Market share increased from 4% to ~6% | Reducing dependence on foreign suppliers |

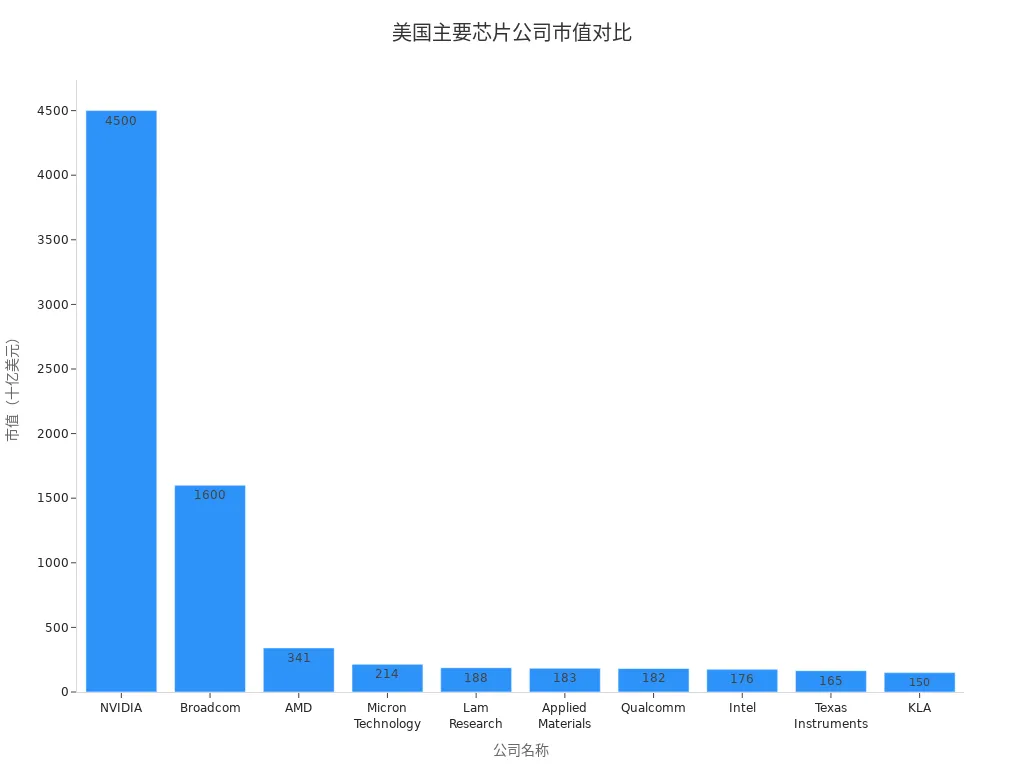

US chip company market caps have changed significantly over the past five years. NVIDIA’s market cap has exceeded $4.3 trillion (reaching around $4.38 trillion as of March 2026), with Broadcom, AMD, and others also achieving substantial growth. The chart below shows the latest market cap landscape for major US chip companies:

AI-related company stock prices have surged dramatically, especially NVIDIA, intensifying market anxiety over AI investment returns. Data shows 80% of US stock market gains come from AI companies; investors need to focus on opportunities and risks from industry volatility. Compute power anxiety drives deep transformation in the chip industry and creates new layout windows for investors.

Recommended US-Listed Chip Stocks

Image Source: pexels

AMD — AI and High-Performance Computing Positioning

AMD continues to advance in AI and high-performance computing, becoming a key growth engine in the US chip industry. The company focuses on R&D for high-performance CPUs and GPUs, driving widespread applications in data centers, cloud computing, and AI workloads. AMD’s EPYC server processors and Instinct GPU series perform strongly in the global data center market, favored by multiple cloud providers and AI enterprises. The company’s 2023 revenue was approximately $25.8 billion, demonstrating strong market competitiveness.

| Metric | Value |

|---|---|

| Revenue | ~$25.8 B |

| Net Profit Growth | N/A |

| AI and High-Performance Computing | N/A |

AMD’s product line covers high-performance CPUs, high-performance GPUs, and data center chips, forming a diversified layout. High-performance CPUs drive market share gains in servers and AI training, while GPU technology holds an important position in AI inference and scientific computing. Continued growth in data center business further solidifies AMD’s industry standing in the AI compute power market.

| Product Line / Technology | Description |

|---|---|

| High-Performance CPU | AMD’s strong performance in the high-performance CPU market drives applications in data centers and AI workloads. |

| High-Performance GPU | AMD’s GPU technology holds an important position in AI and high-performance computing. |

| Data Center | AMD’s growing presence in data centers enhances its competitiveness in AI workloads. |

AMD attracts more developers and enterprise customers through compatibility with mainstream AI training platforms and an open ecosystem. The company continues to increase R&D investment, improving product performance and energy efficiency to actively address market challenges from compute power anxiety.

TSMC — Foundry Leader

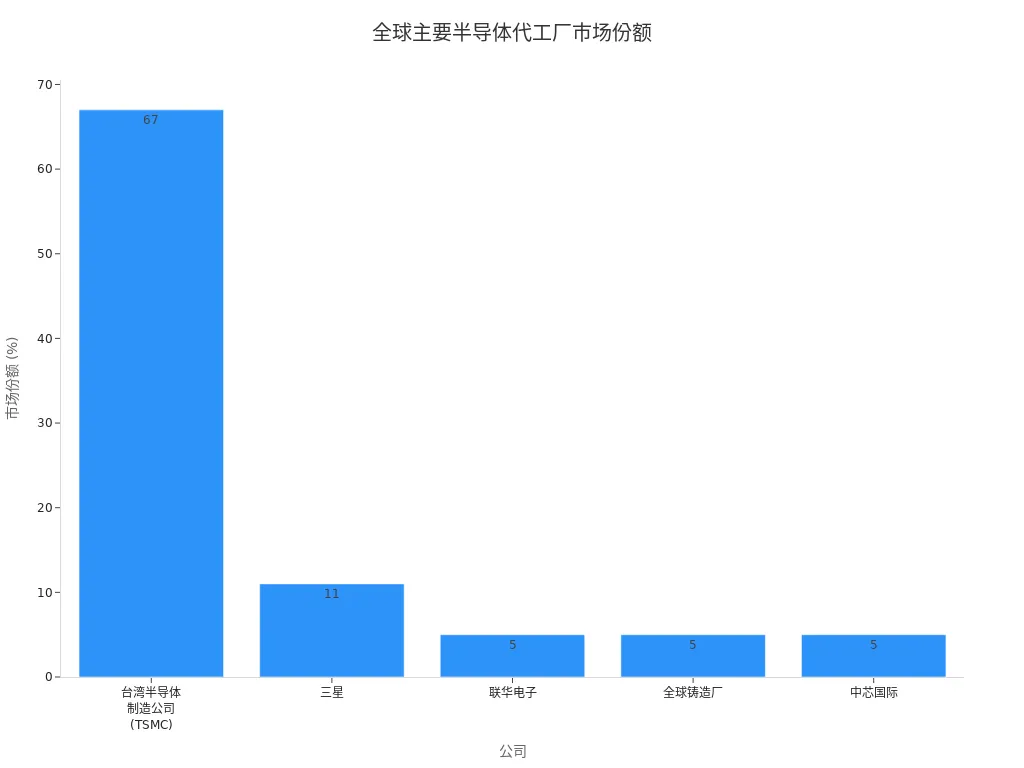

Taiwan Semiconductor Manufacturing Company (TSMC), as the world’s largest semiconductor foundry, controls core links in advanced process and high-end chip manufacturing. The company’s global market share reached nearly 70% in 2025 (around 69.9-70.4%), far surpassing historical competitors. TSMC provides 7nm, 5nm, and more advanced process chip manufacturing services to tech giants like Apple, NVIDIA, and AMD, becoming key support for AI chip mass production.

| Company | Country | Market Share |

|---|---|---|

| Taiwan Semiconductor Manufacturing Company (TSMC) | Taiwan | ~70% |

| Samsung | Korea | ~11% |

| United Microelectronics | Taiwan | 5% |

| GlobalFoundries | US | 5% |

| SMIC | China | ~5% |

TSMC continues to increase capital expenditure and R&D investment, with 2021 capital expenditure at $50 billion and R&D at $320 billion. The company maintains technological leadership in EUV lithography, 3nm, and more advanced processes, driving global AI chip manufacturing capabilities. TSMC’s efficient production and stable supply chain provide a solid foundation for the global AI industry chain.

| Year | Capital Expenditure (Billion USD) | R&D Expenditure (Billion USD) |

|---|---|---|

| 2021 | 50 | 320 |

ASML — Lithography Technology Barrier

ASML is the world’s only company capable of mass-producing EUV extreme ultraviolet lithography machines, holding key technological barriers in chip manufacturing. The company maintains a monopoly in EUV lithography technology, capable of generating, shaping, and controlling 13.5-nanometer photons—a capability stemming from decades and tens of billions of dollars in continuous R&D investment. ASML’s equipment has become indispensable for TSMC, Samsung, Intel, and others to produce high-end AI chips.

| Evidence Type | Details |

|---|---|

| Technology Barrier | ASML maintains a monopoly in EUV lithography; its dominance stems from generating, shaping, and controlling 13.5-nanometer photons, requiring decades and tens of billions in R&D. |

ASML’s technological barriers are extremely high, with global high-end chip manufacturers highly dependent on its equipment. The company continues to innovate, driving chip processes toward smaller nodes and ensuring significant performance improvements for AI and high-performance computing chips.

AVGO (Broadcom) — New Player in AI Compute Power

Broadcom has achieved rapid expansion in the AI-related chip market in recent years, becoming an important supplier of AI compute power infrastructure. The company has a $73 billion AI hardware backlog (with visibility toward over $100 billion in AI chip revenue in 2027), providing strong support for future revenue growth. In fiscal Q1 2026, revenue reached $19.31 billion, up 29% year-over-year, with AI-related revenue growing over 106%.

Broadcom has a $73 billion AI hardware backlog, providing strong support for its future revenue growth.

| Financial Metric | Value |

|---|---|

| Q1 Revenue | $19.31 billion |

| Year-over-Year Growth | 29% |

| AI-Related Revenue Growth | Over 106% |

Broadcom’s AI-related revenue has accounted for half of semiconductor revenue for consecutive quarters, with strong demand for data centers and AI chips. The company’s stock price has doubled in the past 12 months, reflecting high market recognition of its AI infrastructure capabilities.

| Revenue Source | Growth Rate | Notes |

|---|---|---|

| AI-Related Revenue | Over 50% | Accounts for half of semiconductor revenue for consecutive quarters |

| Total Revenue | 29% | Q1 revenue $19.31 billion |

Broadcom strengthens product lines in AI networking chips, storage chips, and custom ASICs through acquisitions and self-development, becoming a key participant in AI data centers and cloud computing infrastructure.

QCOM (Qualcomm) — Mobile and Edge Compute Power

Qualcomm continues to innovate in mobile processors and edge AI chips, driving AI technology penetration into terminal devices and IoT scenarios. The company launched AI200 and AI250 chips, supporting large language models and multimodal models, using near-memory computing architecture to significantly increase memory bandwidth and reduce power consumption. AI200 is expected to commercialize in 2026, and AI250 in 2027.

| Chip Name | Main Features | Commercial Availability |

|---|---|---|

| Qualcomm AI200 | Supports 768 GB LPDDR memory, optimized for general inference tasks, suitable for large language models and multimodal models. | 2026 |

| Qualcomm AI250 | Uses near-memory computing architecture, providing over 10x effective memory bandwidth and significantly reducing power consumption. | 2027 |

Qualcomm actively challenges NVIDIA’s dominance in the AI data center market, seeking to break through traditional smartphone chip business and enter the AI infrastructure market. The company’s market cap is around $145 billion, continuing to dominate connectivity computing in billions of global devices and leading in mobile innovation, RF, and on-device AI.

- Qualcomm launched AI200 and AI250 chips to challenge NVIDIA’s dominance in the AI data center market.

- The company is seeking to move beyond traditional smartphone chip business into the fast-growing AI infrastructure market.

- Market reaction is positive, with Qualcomm’s stock surging, reflecting investor confidence in its strategic transformation.

- Qualcomm’s market cap is around $145 billion, continuing to dominate connectivity computing in billions of global devices.

- The company maintains leadership in mobile innovation, RF leadership, and on-device AI.

Other Potential Chip Companies

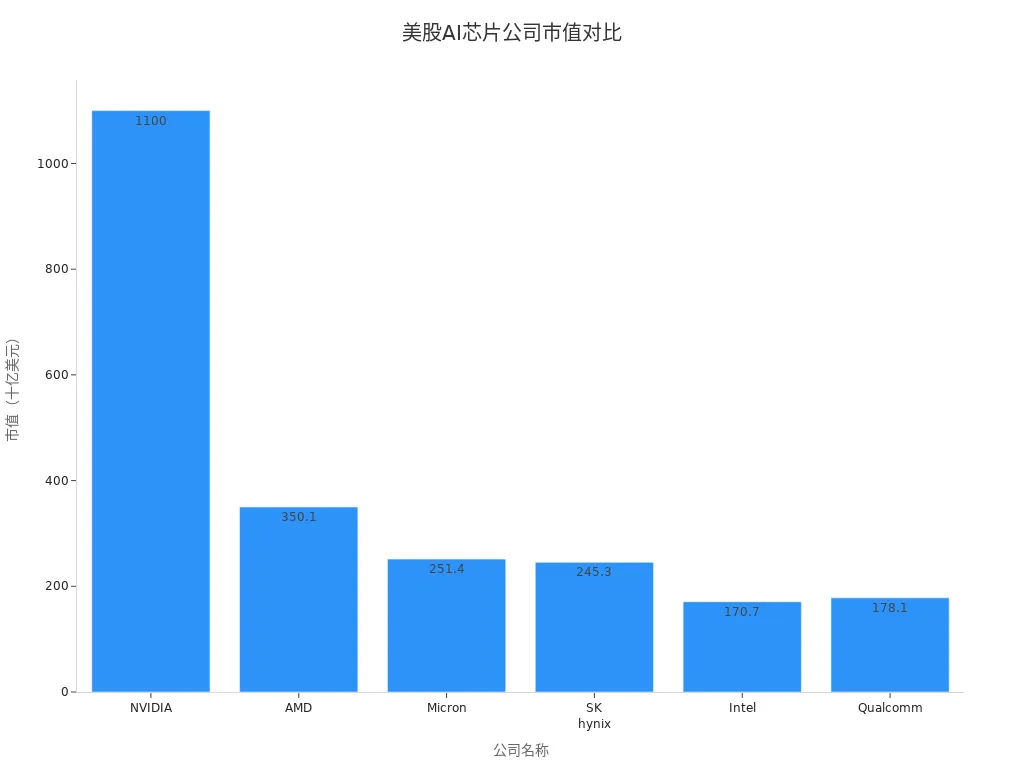

The US market features several other chip companies showing strong growth in AI and high-performance computing. Micron, as the world’s largest memory manufacturer, meets demand for high-bandwidth storage in AI and cloud computing. SK hynix holds leading advantages in DRAM and HBM, supporting AI training and inference. Intel focuses on advanced packaging and foundry services, driving AI chip ecosystem development.

| Company | Market Cap | Role Description |

|---|---|---|

| NVIDIA | ~$4.38T | Leader in AI accelerators, driving deep learning and compute power. |

| AMD | ~$314B | Revival leader in high-performance CPUs and GPUs, driving data centers and AI workloads. |

| Micron | ~$417B | World’s largest memory manufacturer, meeting AI and cloud computing needs. |

| SK hynix | ~$430B | Major force in DRAM and HBM, supporting AI training. |

| Intel | ~$217B | Industry innovation pillar, focusing on advanced packaging and foundry. |

| Qualcomm | ~$145B | Mobile innovation and RF leader, dominating connectivity computing in billions of devices. |

The global semiconductor industry valuation has first surpassed $1 trillion, marking a fundamental shift in economic structure. Micron and SK hynix benefit from high profit margins in AI hardware, with profits significantly improved. NVIDIA’s high-end AI accelerator prices reach $30,000 to $40,000, driving record industry revenue. US chip companies continue to innovate in the AI wave, actively addressing compute power anxiety and becoming core drivers of global tech industry upgrades.

| Company Name | Milestone Description | Related Data |

|---|---|---|

| Global Semiconductor Industry | Industry valuation first exceeds $1 trillion, marking fundamental economic structure shift. | Valuation over $1 trillion in 2026 |

| NVIDIA | High-end AI accelerator prices exceed $30,000 to $40,000, driving record industry revenue. | Modern AI architecture pricing |

| Micron Technology | Record profit margin growth, benefiting from high-margin AI hardware. | Record profit margins |

| SK Hynix | Benefits from rapid semiconductor market expansion, with significant profit growth. | Significant profit increase |

Investment Logic and Core Competitiveness

Business Layout and Technological Advantages

US chip companies adopt diversified business models, forming unique competitive landscapes.

- Integrated Device Manufacturers (IDMs) like Intel handle chip design and manufacturing, controlling the full industry chain.

- Fabless design companies like AMD, Qualcomm, and Broadcom focus on chip design, outsourcing manufacturing to foundries like TSMC to improve cost efficiency and concentrate on innovation.

- Foundries like TSMC focus on high-end chip manufacturing, serving major global design companies.

New entrants require over $10 billion in investment to compete with existing players. The fabless model helps companies accelerate time-to-market, leveraging third-party foundries’ advanced manufacturing capabilities to quickly respond to market demand.

Many companies significantly improve R&D efficiency and innovation by focusing on core competencies and outsourcing manufacturing.

Financial Performance and Growth Potential

Capital expenditure and R&D investment in the chip industry continue to grow, driving companies to maintain technological leadership.

| Category | 2021 Expenditure (Billion USD) | Percentage of Total Capital Expenditures |

|---|---|---|

| Semiconductor Manufacturing | 5.0 | 16% |

| Semiconductor Machinery | 0.314 | 16% |

Market capitalization data reflects the industry’s rapid growth.

| Time Point | Market Capitalization (Trillion USD) | Annual Growth Rate |

|---|---|---|

| December 2023 | 3.4 | - |

| December 2024 | 6.5 | 91% |

| December 2025 | 9.5 | 46% |

AI chip revenue is expected to reach $500 billion in 2026, accounting for about half of global chip sales.

Industry Position and Future Potential

Major chip companies hold core positions in the global semiconductor industry chain.

| Company | Market Cap (Trillion USD) | Future Growth Potential Description |

|---|---|---|

| NVIDIA | ~4.38 | Leadership in generative AI and computing places it in an unprecedented market position. |

| Broadcom | ~1.57 | Strong capabilities in connectivity and custom silicon continue to drive market position improvement. |

| TSMC | ~1.76 | World’s most advanced chip manufacturer; nearly all major fabless companies depend on its technology. |

| ASML | ~0.51 | Its EUV machines are indispensable core technology in chip manufacturing. |

| AMD | ~0.31 | Revival in high-performance CPUs and GPUs drives development in data centers and AI workloads. |

| Qualcomm | ~0.145 | Continued dominance in mobile innovation and RF leadership, connecting billions of devices. |

Companies like Samsung protect their innovations and influence industry standards through patent portfolios and innovation pipelines, shaping market trends. US chip companies, with strong R&D capabilities and technological barriers, are poised to maintain long-term competitive advantages amid rising compute power anxiety.

NVDA Comparison and Diversified Investment Strategy

Business and Growth Path Comparison

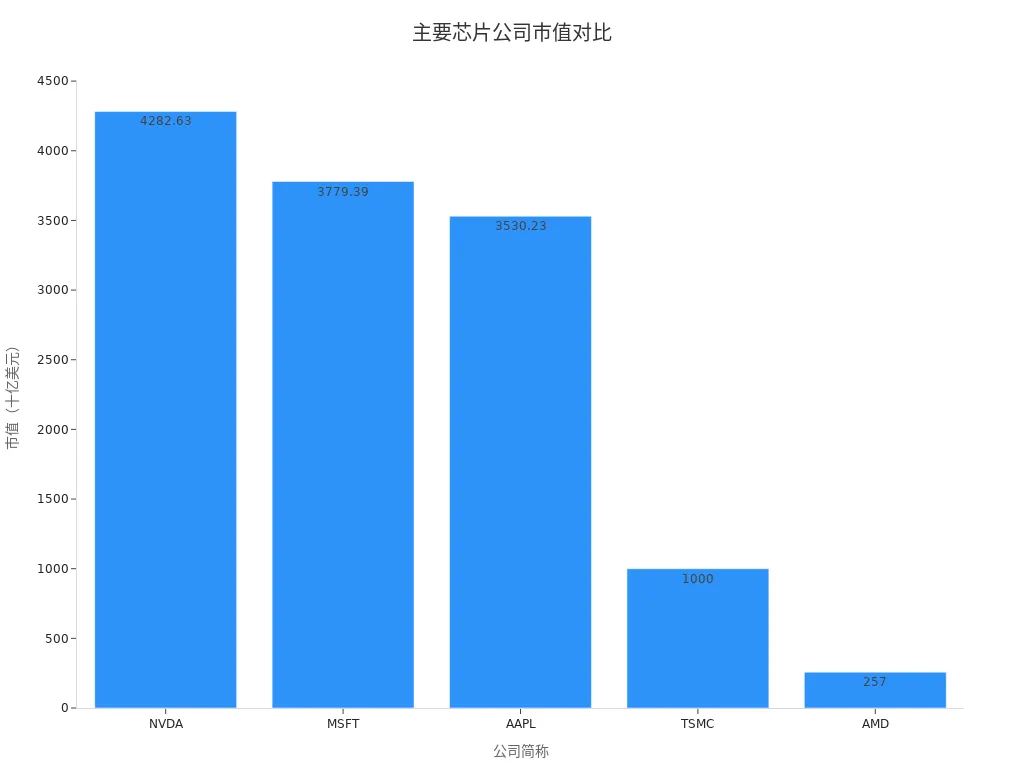

NVIDIA dominates AI infrastructure, becoming one of the world’s highest market cap chip companies. Data shows that as of September 2025, NVIDIA’s market cap reached around $4.17-4.28 trillion (currently ~$4.38 trillion in March 2026), far exceeding peers like AMD and TSMC. The table below shows market cap comparison for major chip companies:

| Stock | Market Cap (as of September 2025, USD) |

|---|---|

| NVDA | ~4,282.63B (updated to ~4.38T in 2026) |

| MSFT | 3,779.39B |

| AAPL | 3,530.23B |

| TSMC | 1,000B+ (currently ~1.76T) |

| AMD | 257B |

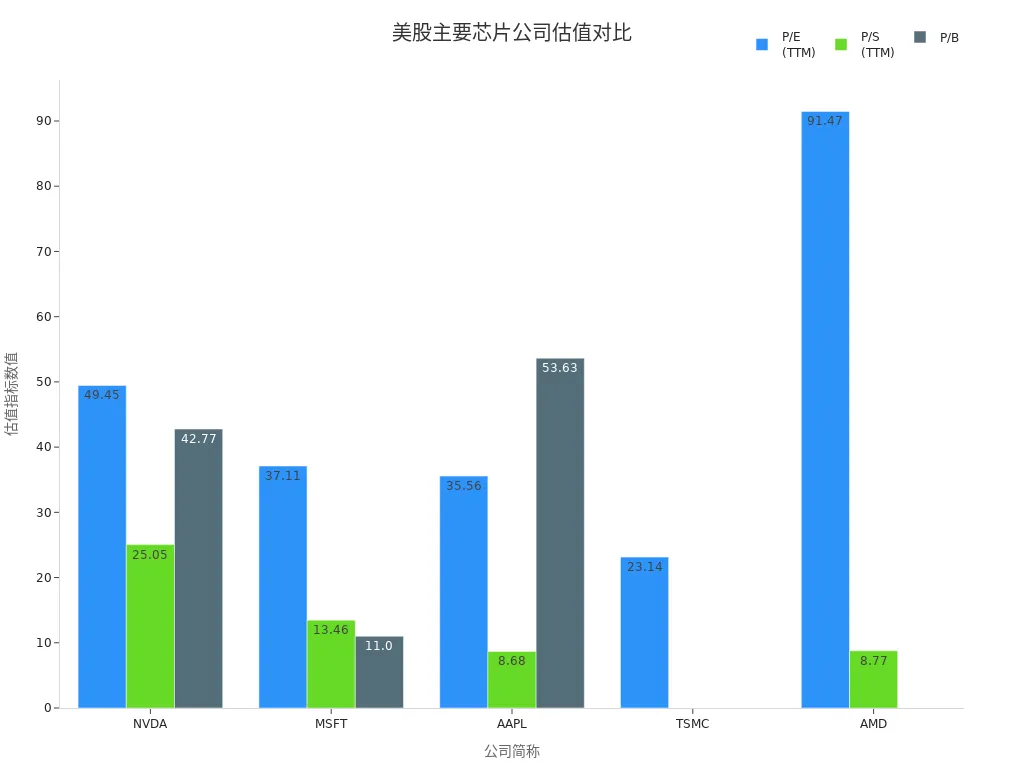

NVIDIA’s growth path heavily relies on the AI data center GPU market, with over 90% share and sustained high R&D investment ($3.09 billion in 2023) maintaining technological leadership. The company’s revenue growth rate reaches 56%, with net profit margin at 56.13%, far above industry averages. In contrast, TSMC focuses on high-end chip manufacturing with high but discounted valuation, while AMD invests continuously in high-performance computing but faces greater volatility from competition with NVIDIA and Intel. The table below compares valuation and profitability for major chip companies:

| Stock | P/E (TTM) | P/S (TTM) | P/B | Revenue Growth | Net Profit Margin | R&D Expenditure (USD) |

|---|---|---|---|---|---|---|

| NVDA | 49.45 | 25.05 | 42.77 | 56% | 56.13% | 3.09B |

| TSMC | 23.14 | N/A | N/A | 54% | 42.76% | 2.1B |

| AMD | 91.47 | 8.77 | N/A | 32% | 10.45% | 1.89B |

NVIDIA’s high valuation reflects market recognition of its AI compute power monopoly but also brings volatility and correction risks. TSMC and AMD maintain steady growth through diversified business layouts and manufacturing capabilities. Overall, NVIDIA holds significant leading advantages in AI infrastructure, but other chip companies possess irreplaceable industry positions in manufacturing, design, and applications.

Necessity of Diversified Investment

The high growth of the US stock chip industry comes with high volatility; when a single company’s valuation is excessively high, investment risk rises significantly. Although NVIDIA boasts extremely strong profitability and market share, its valuation far exceeds industry averages, and any technological iteration, market competition, or policy change could trigger sharp adjustments. Diversified investment effectively reduces systemic risks from single targets and enhances overall portfolio stability.

Investors can allocate across multiple chip companies like TSMC, AMD, ASML, Broadcom, and Qualcomm to cover the full industry chain from design and manufacturing to end applications, achieving risk hedging and return balance.In actual portfolio construction, diversification is not only about spreading positions across names, but also about managing funding routes, conversion costs, and transfer efficiency. A multi-asset trading wallet such as the BiyaPay official website can be used as a supporting tool before cross-market allocation. You can first use its stock information page to review chip-related equities, then combine that with its fiat exchange rate comparison tool to evaluate conversion costs and settlement efficiency under different funding paths.

From a usage perspective, BiyaPay covers cross-border fund movement, US and Hong Kong stock trading, and digital asset management, while holding relevant compliance registrations in jurisdictions including the United States and New Zealand. For investors trying to balance research, allocation, and capital scheduling at the same time, tools like this are better treated as execution-layer support rather than the basis of the investment thesis itself.

Using BiyaPay as an example, global users can leverage its US stock and Hong Kong stock trading deposit/withdrawal services, combined with real-time fiat and digital currency conversion functions, to flexibly allocate diversified assets and conveniently participate in US chip stock investments. BiyaPay supports USDT conversion to USD or HKD, meeting various funding sources and cross-border investment needs while improving capital liquidity and asset allocation efficiency.

Diversified investment not only helps smooth industry cycle fluctuations but also captures structural opportunities in different sub-sectors. Investors should combine their risk preferences, dynamically adjust chip stock weights, focus on valuation reasonableness and long-term growth potential, and avoid overall returns being affected by single-company volatility.

Investment Risks and Considerations

Industry Cycles and Policy Risks

The US semiconductor industry faces multiple cyclical and policy risks. Cyclical downturns mainly stem from supply oversupply; after capacity expansion, companies often encounter demand slowdowns, leading to inventory buildup and price declines. Geopolitical tensions, especially around Taiwan, affect global supply chain stability. Government policies directly impact trade and investment, with US-China export restrictions significantly reducing some companies’ revenue from the Chinese market. Investors need to monitor these risk factors and reasonably assess long-term growth potential for chip stocks.

- Cyclical downturns, mainly due to supply oversupply.

- Geopolitical tensions affect supply chains, particularly around Taiwan.

- Government policy impacts on trade and investment, especially US-China export restrictions affecting revenue from the Chinese market.

Technological Change and Market Competition

Technological iteration accelerates, and market competition intensifies. Compute power anxiety drives continuous corporate innovation but also brings valuation volatility and industry differentiation. Investors need to focus on the following influencing factors:

| Influencing Factor | Description |

|---|---|

| AI Valuation Concerns | Investors question the sustainability of AI valuations, leading to re-evaluation of high-growth tech investments. |

| Earnings Guidance Disappointment | Major companies like Broadcom’s poor financial forecasts lead to sharp stock price declines. |

| Macroeconomic Uncertainty | Overall market sentiment affected by macroeconomic factors, prompting investors to shift to more stable sectors. |

Chip companies must continuously invest in R&D to maintain technological leadership; otherwise, they risk losing market share to emerging competitors. Shortened innovation cycles in the industry require companies to respond quickly to market changes to achieve sustained growth amid compute power anxiety.

Valuation Volatility and Investment Strategies

Chip stock valuations fluctuate significantly; investors must beware of correction risks from high valuations. AI-related company stock prices are heavily influenced by market sentiment and may experience sharp short-term volatility. Recommended investment strategies include:

- Diversified investment covering different sub-sectors and industry chain links to reduce single-company risk.

- Dynamically adjust holding proportions, focusing on corporate financial performance and technological innovation capabilities.

- Combine macroeconomic and policy changes for flexible asset allocation, avoiding blind chasing of highs.

Investors should view chip stocks from a long-term perspective, focusing on industry cycles, policy risks, technological change, and valuation volatility to formulate scientific investment strategies and enhance overall portfolio stability.

The AI era drives sustained growth in compute power demand; US-listed chip companies like AMD, TSMC, ASML, Broadcom, and Qualcomm demonstrate strong growth potential and long-term heavy-holding value. Diversified investment helps balance industry volatility and reduce single-target risks. Investors should focus on industry cycles, policy changes, and technological iterations, dynamically allocate chip assets based on personal risk preferences, and seize structural opportunities.

FAQ

What are the main risks in investing in US-listed chip stocks?

Investors need to focus on industry cycle fluctuations, policy changes, technological iterations, and market competition. Chip industry valuations fluctuate significantly, with potential sharp short-term adjustments; allocate assets reasonably based on personal risk tolerance.

Beyond NVDA, which chip companies offer long-term heavy-holding value?

AMD, TSMC, ASML, Broadcom, and Qualcomm possess core competitiveness in AI, high-performance computing, manufacturing processes, and other areas, with prominent market caps and growth potential, poised to benefit long-term from sustained compute power demand growth.

How to achieve diversified investment in US-listed chip stocks?

Investors can allocate across chip companies in different sub-sectors to cover design, manufacturing, application, and other links, reducing single-company risk. Some cross-border payment platforms support USD deposits/withdrawals for flexible US stock asset allocation.

What is the future growth space for the AI chip industry?

The AI chip market benefits from generative AI, data centers, and smart terminal demand; revenue is expected to account for a rising share of global chip sales over the next five years, with strong overall industry growth and clear innovation drivers.

How to manage exchange rates and capital liquidity when investing in US-listed chip stocks?

Some platforms provide real-time USD and digital currency conversion services for Chinese-speaking users, supporting US stock and Hong Kong stock deposits/withdrawals, improving capital liquidity for investors to flexibly adjust asset allocation based on market changes.

*This article is provided for general information purposes and does not constitute legal, tax or other professional advice from BiyaPay or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or warranties, express or implied, as to the accuracy, completeness or timeliness of the contents of this publication.

Related Blogs of

How Is China’s Memory Supply Chain Different from Overseas Memory Leaders? A Comparison with Micron, SanDisk, Western Digital, and Seagate

How Does NAND Price Increase Affect SanDisk? Enterprise SSDs, Consumer Storage, and Margin Leverage

How to Read NAND Contract Prices and Spot Prices? Why Enterprise SSDs and Consumer SSDs Do Not Move in Sync

How Should You View Seagate’s HAMR Technology? Nearline HDD Capacity Upgrades and the Supply-Demand Cycle

Choose Country or Region to Read Local Blog

Contact Us

BIYA GLOBAL LLC is registered with the Financial Crimes Enforcement Network (FinCEN), an agency under the U.S. Department of the Treasury, as a Money Services Business (MSB), with registration number 31000218637349, and regulated by the Financial Crimes Enforcement Network (FinCEN).

BIYA GLOBAL LIMITED is a registered Financial Service Provider (FSP) in New Zealand, with registration number FSP1007221, and is also a registered member of the Financial Services Complaints Limited (FSCL), an independent dispute resolution scheme in New Zealand.