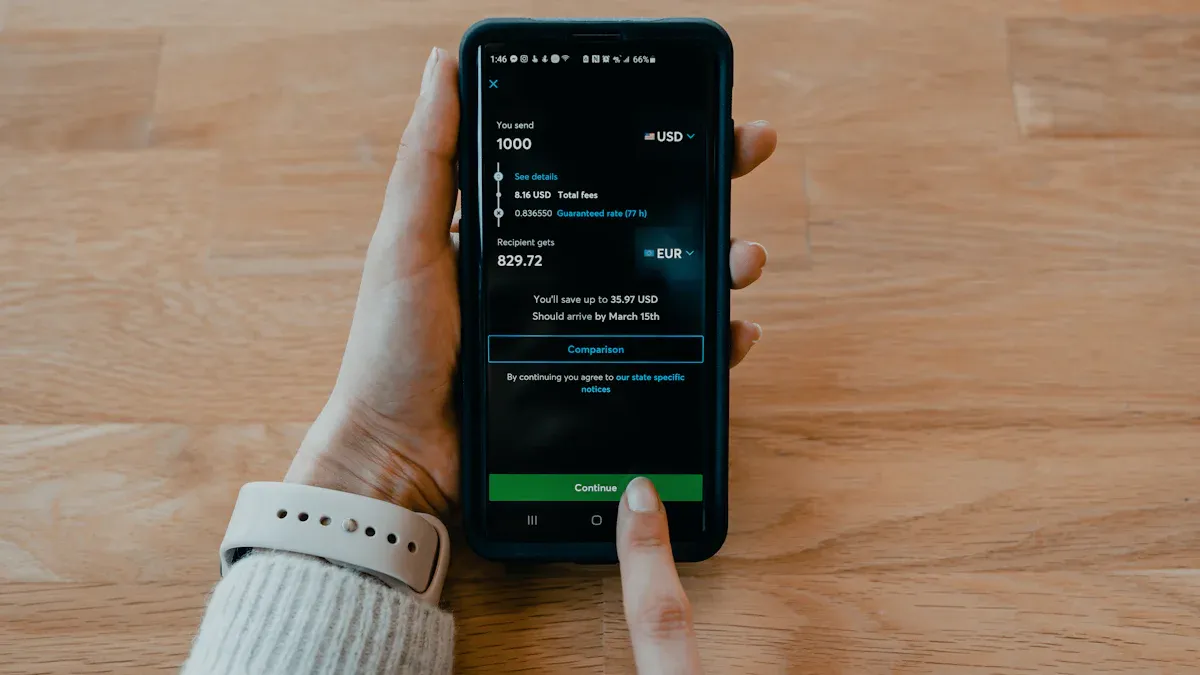

Frequent Failures When Withdrawing from OKX/Binance to Bank Card? Try Switching Fiat Off-Ramp Providers to Licensed Financial Apps

Image Source: pexels

Many users frequently encounter failures or long pending statuses when withdrawing from OKX or Binance to bank cards. The main reasons include delays caused by bank holidays, incomplete KYC certification on accounts, withdrawal amounts exceeding limits, mismatch between bank account name and platform, insufficient liquidity, etc. You can try switching the fiat off-ramp provider to a licensed financial App, which can improve compliance and fund security, making fund arrival more stable. You need to focus on safer, more compliant, and more stable withdrawal methods to optimize your operating experience.

Key Takeaways

- Choosing licensed financial Apps can increase the success rate of withdrawals to bank cards, ensuring fund security and compliance.

- Ensure identity information is real, complete, and consistent with the bank account to avoid withdrawal failures.

- Understand the platform’s fee structure and choose transparent service providers to avoid hidden fees affecting the final received amount.

- Using licensed financial Apps usually allows faster arrival, with funds typically arriving within 1-2 business days.

- During operations, maintain network security and avoid transferring funds on public Wi-Fi to protect personal information.

Reasons for Withdrawal to Bank Card Failures

Image Source: pexels

Impact of Compliance Policies

When withdrawing to a bank card, you are first directly affected by regulatory policies in mainland China. Since mainland China strengthened regulation of cryptocurrencies, related policies have imposed strict restrictions on fund flows. You can refer to the table below to understand the impact of policy changes on withdrawal success rates to bank cards:

| Evidence Point | Description |

|---|---|

| Regulatory Changes | China prohibits cryptocurrency trading and implements strict overseas withdrawal restrictions. |

| Withdrawal Limits | Since January 1, overseas withdrawal limit for mainland China bank cards is USD 15,400 per year. |

| Impact | Policies aim to curb capital outflows, restrict fund access, and reduce success rate of withdrawals to bank cards. |

You will find that compliance directly determines whether funds can arrive smoothly. After policy tightening, many platforms and banks automatically intercept or reject related transactions, leading to withdrawal failures.

Identity Verification Issues

Identity verification is a link you cannot ignore when withdrawing to a bank card. Many users encounter obstacles in the KYC (Know Your Customer) process, mainly due to:

- KYC process requires detailed personal information; some users worry about privacy leaks, leading to incomplete certification.

- Only after passing identity checks can you access fiat channels; incomplete certification will result in platform rejection of withdrawals.

- Exchanges continuously upgrade biometric systems to prevent new types of fraud and AI forgery; some users cannot smoothly pass liveness detection due to technical reasons.

- Inconsistency between certification information and bank account information also causes withdrawal failures.

You need to ensure all identity information is real, complete, and consistent with the bank account to improve the success rate of withdrawals to bank cards.

Bank Receiving Capability

Banks’ capability to receive cryptocurrency-related funds also affects your withdrawal experience. The People’s Bank of China has declared all cryptocurrency-related transactions illegal, and banks usually take the following measures:

| Event | Content |

|---|---|

| Legal Statement | People’s Bank of China declares all cryptocurrency-related transactions illegal |

| Impact | Banks do not process related transactions; main reason for rejection is policy ban and legal framework |

During operations, you will find that some bank systems automatically identify and intercept cryptocurrency-related fund inflows. Even if the platform approves, the bank side may directly refuse the deposit, resulting in withdrawal to bank card failure.

Off-Ramp Provider Risks

Traditional fiat off-ramp providers carry significant risks in compliance and fund security. When you choose unlicensed off-ramp providers, you are prone to the following issues:

- Off-ramp providers may be seized due to policy risks, leading to funds not arriving.

- Fund flow paths are opaque, increasing money laundering and fraud risks.

- Off-ramp provider rugs or disappears, making user funds difficult to recover.

- Lack of regulation during transactions, with no protection for user rights.

You need to understand that compliance and security are key to improving withdrawal success rates to bank cards. Choosing licensed financial Apps can effectively avoid the above risks and safeguard fund security and arrival efficiency.

Advantages of Licensed Financial Apps

Image Source: unsplash

Compliance and Security Guarantees

Choosing licensed financial Apps for withdrawals to bank cards provides higher compliance and security guarantees. Taking Biyapay as an example, the platform strictly follows international regulatory standards and adopts the same compliance requirements as securities and commodity futures exchanges. The platform requires you to complete KYC identity verification to ensure every fund flow complies with anti-money laundering and anti-terrorist financing regulations. During use, all assets are custodied by licensed third parties, with transparent fund paths, greatly reducing money laundering and fraud risks.

You can rest assured that licensed financial Apps like Biyapay use cold wallet storage for most crypto assets and provide multi-factor authentication and insurance mechanisms to further enhance fund security.

Arrival Speed

When initiating withdrawals to bank cards on licensed financial Apps like Biyapay, you usually experience faster arrival times. The platform cooperates with multiple Hong Kong licensed banks to optimize the fund clearing process. After submitting a withdrawal request, the system automatically matches the optimal channel, reducing intermediate steps and improving fund circulation efficiency. In most cases, funds arrive within 1-2 business days, much faster than the multi-step transfers and manual review processes of traditional off-ramp providers.

User Experience

You will find that the operation interface on licensed financial Apps is concise and clear. Biyapay provides multi-language support and 7×24-hour customer service for Chinese-speaking users. You can check order status at any time and quickly get professional answers when issues arise. The platform automatically prompts you to complete identity authentication and risk reminders to help avoid common operational mistakes.

- You don’t need to worry about complex fund paths

- You can complete recharge, exchange, and withdrawal with one click

Comparison with Traditional Off-Ramp Providers

You can visually understand the main differences between licensed financial Apps and traditional fiat off-ramp providers through the table below:

| Feature | Licensed Financial Apps (e.g., Biyapay) | Traditional Fiat Off-Ramp Providers |

|---|---|---|

| Regulatory Compliance | Subject to international/regional financial regulation | Lack of unified regulation |

| Fund Security | Cold wallet + multi-factor authentication + insurance | Opaque fund flows |

| Arrival Speed | 1-2 business days | 3-5 business days or longer |

| User Protection | 7×24-hour customer support | Slow customer response, high risk |

Choosing licensed financial Apps can significantly increase the success rate and fund security of withdrawals to bank cards, avoiding losses due to policy risks or off-ramp provider rug pulls.

Withdrawal to Bank Card Operation Process

Registration and Authentication

Before using licensed financial Apps (such as Biyapay) for withdrawals to bank cards, you first need to complete registration and identity authentication. The platform requires you to provide real and valid personal information and ensure account security through multiple verifications. Specific steps are as follows:

- Provide mobile phone number, email address, and residential address, ensuring information is real and valid.

- Upload two unexpired government-issued photo ID documents, ensuring the documents are complete, glare-free, shadow-free, and all text is clearly readable when photographing.

- Select country and document type, take photos of ID documents as prompted by the platform, and complete selfie verification.

- Scan the QR code to complete mobile verification or continue authentication using a webcam in the browser.

- Maintain a stable network environment; Chrome browser is recommended, and avoid closing the window during verification.

- Wait for platform review, usually completed within 1-2 business days.

Different platforms have different requirements for authentication levels. You can refer to the table below to understand required materials for each level:

| Verification Level | Requirements |

|---|---|

| Basic | Age 18+, mobile number, email, residential address, two valid photo IDs |

| Basic Plus | Basic requirements + proof of address |

| Intermediate | Basic Plus requirements + supplementary proof of address |

| Full | Intermediate requirements + financial statements |

Licensed financial Apps adopt electronic identity verification systems and multi-factor authentication, strictly following international compliance standards such as KYC and AML. This process is far stricter than traditional fiat off-ramp providers’ reviews and effectively safeguards your account and fund security.

Recharging Cryptocurrency

After completing registration and authentication, you can recharge cryptocurrency to your licensed financial App account. The operation process is straightforward:

- Log in to the App, go to the “Recharge” page, and select the cryptocurrency you hold (such as USDT, BTC, ETH, etc.).

- Copy the recharge address generated by the platform or scan the QR code to transfer cryptocurrency from your wallet or exchange to that address.

- Wait for blockchain network confirmation; the platform will automatically credit the account upon confirmation.

Recharge fees and arrival times vary slightly across platforms. You can refer to the table below:

| Platform | Deposit Fee | Processing Time |

|---|---|---|

| FXTM | May incur fees | Instant processing (no additional verification) |

| Ndax | Free | 0-30 minutes (Interac e-Transfer) or 1 business day (wire transfer) |

Licensed financial Apps like Biyapay usually support multiple mainstream cryptocurrencies, with transparent and traceable recharge processes.

Withdrawal to Bank Card Process

After recharging, you can withdraw funds to your bank card through the following steps:

- In the App, select “Sell Digital Assets” to convert cryptocurrency to fiat (such as USD).

- Add and bind your bank card information, ensuring the bank card supports international receipts and the account name matches the authentication information.

- Enter the withdrawal amount, select the target bank card, confirm transaction details, and submit the application.

- Wait for platform review and processing; funds usually arrive within 1-2 business days.

- After receiving platform notification, log in to your bank account to verify whether the funds have arrived.

The entire process is highly automated, with the platform providing real-time progress prompts at every step. You don’t need to worry about complex fund paths; all operations are conducted under compliant regulation.

Process Considerations

During operations, pay attention to the following matters to improve the success rate of withdrawals to bank cards:

- Confirm all identity information and bank card information are real and consistent to avoid withdrawal failures due to mismatches.

- Use original, unexpired documents and ensure clear, readable photos with proper lighting.

- When recharging or withdrawing, pay attention to the platform’s announcements and avoid operations during system maintenance or peak periods.

- Understand the platform’s fee policy; some platforms charge 1-2% withdrawal fees (specifics based on actual page), all amounts priced in USD.

- Maintain a stable network environment to avoid operation failures due to interruptions.

- If delays occur, contact 7×24-hour customer service within the App; the platform will assist in troubleshooting.

Licensed financial Apps have strict standards in identity verification, fund flow, information protection, and other aspects. Simply follow the platform’s guidance to complete withdrawals to bank cards efficiently and securely.

Considerations

License Verification

When choosing licensed financial Apps, first verify whether the platform holds legitimate financial licenses. Compliant platforms strictly implement KYC (Know Your Customer) procedures, requiring submission of real identity information to reduce fraud and money laundering risks. You also need to pay attention to whether the platform conducts transaction monitoring to ensure all fund flows are legal and compliant. Compliant platforms perform sanctions list screening, politically exposed persons (PEP) screening, and adverse media screening to further safeguard fund security.

At this stage, it also helps to check whether the actual fund route is clearly presented, not just whether the platform mentions licensing. You can first review the supported business scope on the BiyaPay website, then use its fiat conversion and comparison tool to estimate exchange costs. If cross-border settlement may be involved later, the remittance service can also help you judge whether the path is easier to reconcile with a compliant receiving account. As a multi-asset trading wallet, BiyaPay covers cross-border payments, stock investing, contract trading, crypto trading, and fund management scenarios, and it discloses relevant registrations and licensing information such as US MSB and New Zealand FSP. That kind of public information is more useful as supporting context when evaluating whether a platform is suitable as a stable long-term fiat off-ramp.

- You can check license information on the platform’s official website or regulatory authority websites to confirm the platform is regulated by financial authorities in Hong Kong, Singapore, etc.

- Prioritize financial Apps with strong compliance and transparent public information to avoid fund losses due to platform qualification issues.

Fee Transparency

Before withdrawing, you should fully understand the platform’s fee structure. Mainstream licensed financial Apps publicly display deposit and withdrawal fees, including different rates for cryptocurrency and fiat. Fees are usually influenced by asset type, transfer method, network congestion, etc. Some platforms offer low commissions, but others may have hidden fees.

- Carefully read fee explanations to avoid reduced final received amounts due to hidden costs.

- Compare withdrawal fee rates across platforms and choose service providers with reasonable, transparent fee structures.

- During operations, always use USD as the pricing unit for easy calculation of actual expenses.

Information Security

When using licensed financial Apps, information security is crucial. Compliant platforms formulate strict information protection policies based on SEC’s Regulation S-P, regularly providing users with privacy notices that clearly define information sharing scope and user rights. Platforms also implement identity theft prevention measures under Regulation S-ID to prevent illegal use of personal information.

- During fund transfers, the platform uses multi-factor authentication and encryption technology to safeguard account and asset security.

- Avoid operations on public Wi-Fi to prevent information theft by hackers.

- Regularly change passwords and enable two-factor authentication to enhance account security level.

Common Issue Handling

You may encounter various problems during withdrawal. The table below summarizes common issues and corresponding solutions to help you respond efficiently:

| Issue Type | Solution |

|---|---|

| Withdrawal status pending | Check network congestion, adjust transaction fees; raise fees if necessary or contact platform customer service. |

| Using insecure connection | Avoid public Wi-Fi; prioritize secure network environments. |

| Transaction delay | Choose efficient platforms; avoid initiating withdrawals during peak periods. |

| Insufficient transaction fees | Appropriately increase transaction fees to ensure miners prioritize processing. |

| Small-amount transactions | Consider low-cost fast channels such as Lightning Network. |

When encountering issues, contact platform customer service at any time for professional support. Also pay attention to platform announcements to stay informed about system maintenance or policy changes and avoid affecting fund flows due to information lag.

Choosing licensed financial Apps as withdrawal channels provides higher security and compliance guarantees. With fast arrival, transparent processes, and effectively reduced failure risks, you should focus on details such as identity authentication and information protection while strictly complying with requirements. This improves fund circulation efficiency and safeguards fund security.

FAQ

How to determine whether a financial App holds a legitimate financial license?

You can check the license information on the platform’s official website or relevant financial regulatory authority websites. Legitimate platforms publicly display license numbers and regulatory authorities, ensuring all business is conducted under compliant regulation.

Why is strict identity authentication required when withdrawing to a bank card?

You need to complete identity authentication to meet KYC and anti-money laundering regulatory requirements. The platform uses multiple verifications to ensure fund security, prevent illegal funds from entering the financial system, and enhance transaction compliance.

How long does it generally take for withdrawals to arrive?

Withdrawals to bank cards through licensed financial Apps usually arrive within 1-2 business days. Specific time depends on bank processing efficiency and platform review speed; slight delays may occur during peak periods.

What are the common fees during withdrawal?

During withdrawal, pay attention to publicly displayed fees on the platform, usually 1-2% of the withdrawal amount priced in USD. Some platforms also charge blockchain network fees; specifics are based on the actual page.

How to protect personal information and fund security?

You should choose platforms that use multi-factor authentication and encryption technology. Legitimate financial Apps regularly update privacy policies, strictly protect user data, and prevent information leaks and account misuse.

*This article is provided for general information purposes and does not constitute legal, tax or other professional advice from BiyaPay or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or warranties, express or implied, as to the accuracy, completeness or timeliness of the contents of this publication.

Related Blogs of

Which Products Are Affected by NAND Price Increases? SSDs, Smartphones, Servers, and Consumer Electronics

What Is the Difference Between HBM Stocks and GPU Stocks?

Enterprise SSD vs Consumer SSD: Price, Endurance, Use Cases, and Related Companies

Which Storage Chip Concept Stocks Are There in 2026? Classification of Related U.S. and Hong Kong Companies

Choose Country or Region to Read Local Blog

Contact Us

BIYA GLOBAL LLC is registered with the Financial Crimes Enforcement Network (FinCEN), an agency under the U.S. Department of the Treasury, as a Money Services Business (MSB), with registration number 31000218637349, and regulated by the Financial Crimes Enforcement Network (FinCEN).

BIYA GLOBAL LIMITED is a registered Financial Service Provider (FSP) in New Zealand, with registration number FSP1007221, and is also a registered member of the Financial Services Complaints Limited (FSCL), an independent dispute resolution scheme in New Zealand.