When "Anti-Freeze Card" Becomes a Crypto Essential: Reviewing the Three Mainstream USDT Cashout Methods in 2026

Image Source: unsplash

In 2026, with stricter crypto regulation, you will find that bank transfers involving cryptocurrency are often delayed, reviewed, or frozen. Many banks cannot accurately classify or explain related transactions, leading to paused transfers. Global reporting obligations have increased, and banks become particularly conservative when information is incomplete. Anti-freeze cards have become an essential tool to help you avoid account freezing risks. You can choose three mainstream USDT cashout methods, including lending, staking, and liquidity provision. Evaluation criteria cover security models, transparency of yield sources, liquidity, performance records, and net returns. You need to select the most suitable solution based on your actual situation.

Key Takeaways

- Anti-freeze cards are an important tool to avoid bank freezing risks, ensuring fund security and liquidity.

- OTC platforms are suitable for large transactions, with fast processing, usually completing fund exchange within 5-30 minutes.

- P2P trading offers flexibility and privacy, suitable for experienced users, but beware of fraud risks.

- Third-party payment cards support global spending, ideal for cross-border payments, with high transaction efficiency but slightly higher fees.

- When choosing a cashout method, consider fund size, liquidity needs, and compliance requirements to ensure fund security.

OTC Platforms

Image Source: pexels

Operation Process

You can cash out USDT to USD through OTC platforms. Taking Biyapay as an example, first register an account and complete KYC identity verification. You select to sell USDT, enter the amount, and the platform automatically matches buyers. After confirming the order, you transfer USDT to the platform’s designated wallet. Once received, the platform arranges USD payment, usually via Hong Kong licensed banks. You need to verify the receipt information to ensure funds arrive. The entire process is straightforward, but pay attention to transaction amounts and accuracy of bank receipt details.

| Fee Type | Description |

|---|---|

| Transaction Fee | Includes trading fees, withdrawal fees, and currency conversion fees. |

| Processing Time | Transactions are usually fast, but bank transfers may require additional time. |

Pros and Cons

OTC platform cashout methods offer high liquidity and faster processing speeds. You can conduct large transactions, with platforms providing dedicated customer service to meet personalized needs. You don’t need to worry about sharp market price fluctuations, as OTC platforms reduce market impact. Drawbacks include higher transaction fees and some platforms imposing limits on new users. You also bear risks of bank transfer delays and compliance reviews.

Risk Analysis

- Bank Risks: Some banks flag crypto-related transfers, leading to settlement delays or temporary account restrictions.

- Compliance Risks: KYC verification delays, enhanced due diligence, or withdrawal restrictions may slow down your fund extraction.

- P2P Fraud Risks: When cashing out USDT in peer-to-peer markets, reversal scams, payment disputes, or identity mismatches may occur.

Role of Anti-Freeze Cards

Anti-freeze cards play a key role in OTC platform cashouts. Using anti-freeze cards can effectively avoid bank freezing risks and enhance fund security. Anti-freeze cards help bypass sensitive transaction tags, ensuring smooth fund arrival. For large transactions, anti-freeze cards become an essential tool to safeguard fund flow.

Suitable Users

- OTC trading is mainly suitable for high-net-worth individuals and institutional investors.

- If you need large fund transfers, seek higher confidentiality and liquidity, you can choose OTC platforms.

- Platforms suit users who want to complete large USDT cashouts without affecting market prices.

P2P Trading

Operation Process

You can cash out USDT directly with buyers through P2P platforms. Taking Binance P2P and Biyapay as examples, register an account and complete identity verification. You post a sell USDT order, set the price and payment method. The platform automatically matches buyers; after both parties confirm, the platform escrows the USDT. Once the buyer completes USD payment, you confirm receipt, and the platform releases USDT. Common payment methods include Hong Kong licensed bank transfers, third-party payment cards, etc. Ensure receipt account information is accurate to avoid transaction disputes.

| Platform Name | Supported Currencies | Main Features | Security Measures |

|---|---|---|---|

| LocalBitcoins | USDT, BTC | Multiple payment methods, user-friendly interface, escrow protection | Two-factor authentication, user rating system |

| Paxful | USDT, USDC | Direct trading, multiple payment methods, user-friendly interface, escrow protection and customer support | Two-factor authentication |

| Binance P2P | USDT, USDC | Large payment options, reputation system, competitive fees, fast trades | Smart contracts |

| WazirX P2P | USDT, USDC | Escrow protection, multiple payment methods, high security | Two-factor authentication |

| Remitano | USDT, USDC | Multiple digital assets, escrow protection, intuitive interface | Smart contracts, two-factor authentication |

| HodlHodl | USDT, BTC | Decentralized trading, multi-signature smart contracts, multiple payment methods | No traditional institutions needed, enhanced privacy |

Pros and Cons

You can flexibly choose buyers and payment methods, with higher transaction privacy. P2P platforms like Biyapay support multiple payment channels to meet Chinese-speaking users’ needs. You don’t rely on centralized institutions, and transaction fees are lower. Drawbacks include transaction speed depending on buyer availability, potentially slower. You need some experience, as the process is complex. Platform security measures are limited, with fraud risks.

| Feature | P2P Trading Platforms (e.g., Binance) | OTC Platforms (e.g., Breet) |

|---|---|---|

| Security | Transactions occur directly between users, with fraud risks. | Provides strong security measures like dual identity verification. |

| Convenience | Complex process, suitable for experienced users. | Simple design, user-friendly interface, easy to operate. |

| Transaction Speed | Speed depends on market buyer availability, may be slow. | Fast transactions, average completion within 5 minutes. |

| Reliability | Depends on individual buyers, may be unstable. | Centralized platform, consistent and reliable service. |

| User Experience | May not be beginner-friendly. | Suitable for beginners, simple operations. |

| Privacy | Requires KYC, limited information sharing. | Requires KYC, but information is confidential. |

Risk Prevention

In P2P trading, beware of the following risks:

- Buyers may be scammers, using fake identities for fraud.

- Accounts may be frozen due to suspected illegal activities, making funds unusable.

- Decentralized exchange P2P platforms are more easily exploited by scammers, increasing transaction risks.

Reduce risks by choosing reputable platforms, enabling two-factor authentication, verifying buyer identity and transaction records. Avoid large transactions with unknown buyers and prioritize platform escrow features.

Role of Anti-Freeze Cards

Anti-freeze cards help avoid bank freezing risks in P2P trading. You can bypass sensitive transaction tags with anti-freeze cards, enhancing fund arrival security. For high-frequency or large transactions, anti-freeze cards become an important tool to safeguard fund flow, especially suitable for users needing multi-channel receipts.

Suitable Users

P2P trading suits experienced users seeking transaction flexibility and privacy. If you want to independently choose buyers and payment methods or need multi-channel receipts, consider P2P platforms. Chinese-speaking users, cross-border fund demanders, and those valuing privacy and security can benefit from P2P trading.

Third-Party Payment Cards

Image Source: pexels

Operation Process

You can quickly cash out USDT to USD through third-party payment card platforms. Taking Biyapay as an example, first register an account and complete identity verification. You select to sell USDT, and the platform generates receipt card information. Transfer USDT to the platform’s designated wallet; the platform automatically completes USDT to USD conversion. The platform then loads USD onto your third-party payment card, usually supporting Hong Kong licensed bank transfers or international card payments. You can spend or withdraw USD globally. The entire process is concise: blockchain confirmation usually within 10 minutes, USDT to USD conversion about 5-30 minutes, bank settlement 1-3 business days.

Note: Ensure receipt card information is accurate to avoid delays or loss due to errors.

| Type | Fee/Time Description |

|---|---|

| USDT Sale Fee | Trading platforms usually charge 0.1%-0.3% transaction fees, or include spreads in instant sales. |

| Network Fee | TRC20 USDT usually has low fees, while ERC20 USDT fees are higher during Ethereum congestion. |

| Bank Transfer Fee | Bank processing fees and card payment fees may incur additional service charges. |

| Processing Time | 0-10 minutes: blockchain confirmation; 5-30 minutes: USDT to USD conversion; 1-3 business days: bank settlement time. |

Pros and Cons

You enjoy high efficiency and global liquidity. Third-party payment cards support multi-currency spending, suitable for cross-border payments and international shopping. You don’t rely on traditional bank accounts, with higher fund security. Drawbacks include slightly higher transaction fees and some platforms limiting new users. You may encounter unstable card payment channels or bank settlement delays. Some countries strictly regulate third-party payment cards, potentially affecting fund flow.

Risks and Compliance

Pay attention to compliance risks. Some third-party payment card platforms lack financial licenses, posing fund security hazards. During use, focus on identity verification and legal fund sources to avoid card freezing due to suspected illegal activities. Banks and payment institutions strengthen transaction reviews, especially for large fund flows. Choose legitimate platforms and prioritize Hong Kong licensed bank channels to ensure fund security.

Role of Anti-Freeze Cards

Anti-freeze cards play an important role in third-party payment card cashouts. You can bypass sensitive transaction tags with anti-freeze cards, reducing bank freezing risks. Anti-freeze cards help improve fund arrival efficiency and ensure liquidity. For high-frequency trading and large fund transfers, anti-freeze cards become indispensable security tools.

Suitable Users

Third-party payment cards suit users needing global spending, cross-border payments, and international fund flows. If you want to quickly cash out USDT and use USD globally, choose third-party payment cards. Chinese-speaking users, cross-border e-commerce operators, and international freelancers can benefit from this method. You need some financial knowledge, focus on compliance and risk prevention, and choose legitimate platforms to safeguard fund security.

Cashout Method Comparison

Efficiency and Convenience

When choosing USDT cashout methods, efficiency and convenience are core considerations. OTC platforms like Biyapay support large transactions with fast processing, usually completing fund exchange within 5-30 minutes. P2P trading depends on buyer availability, with speed affected by the market; some platforms like Binance P2P achieve quick matching but overall efficiency is slightly lower. Third-party payment card methods suit global spending, with short blockchain confirmation times and USDT to USD conversion as fast as 10 minutes.

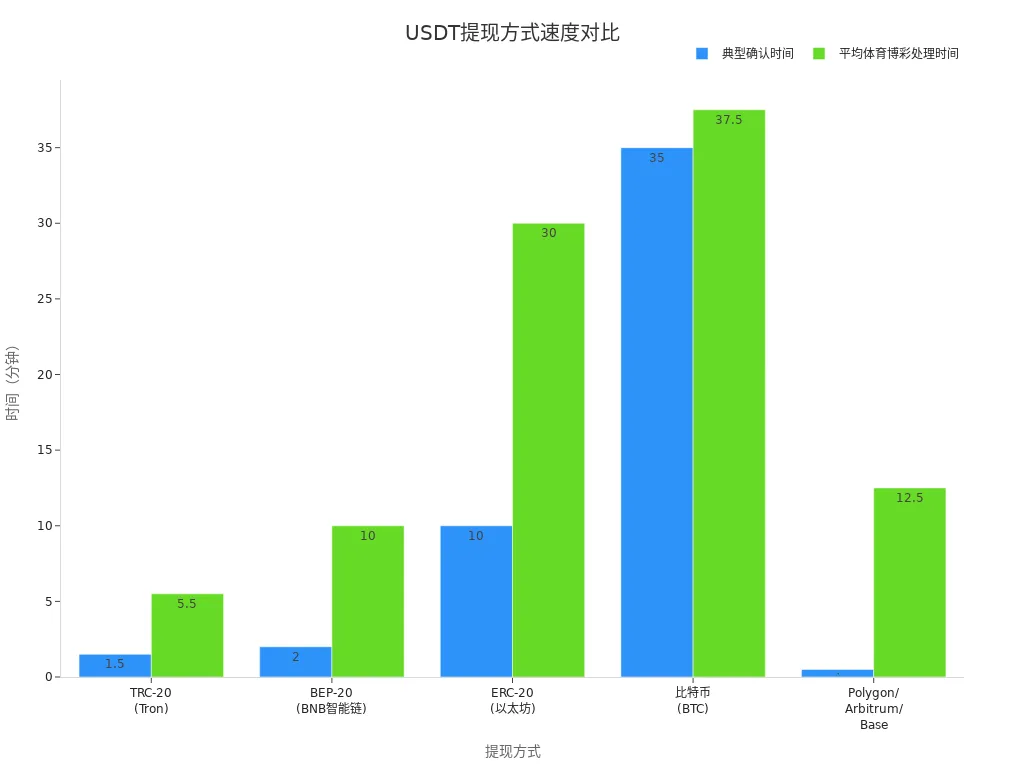

The table below shows typical confirmation times and processing efficiency for different networks:

| Network | Typical Confirmation Time | Average Processing Time | Remarks |

|---|---|---|---|

| TRC-20 (Tron) | 1–2 minutes | 1–10 minutes | Fastest and lowest-fee USDT transfers |

| BEP-20 (BNB Smart Chain) | 1–3 minutes | 5–15 minutes | Balanced cost and reliability |

| ERC-20 (Ethereum) | 5–15 minutes | 15–45 minutes | High gas fees, occasional delays |

| Bitcoin (BTC) | 10–60 minutes | 15–60 minutes | Secure but slower |

| Polygon / Arbitrum / Base | <1 minute | 5–20 minutes | Layer 2 networks, low cost |

You will find that crypto asset cashout speeds far exceed traditional bank channels, especially in scenarios like sports betting, where blockchain processing is more transparent and efficient.

Risks and Security

Focus on the security of each method. OTC platforms usually have strict KYC and fund escrow measures, suitable for large fund flows. P2P trading platforms provide escrow protection to reduce fraud risks, but you must verify buyer identity yourself. Third-party payment card methods depend on platform compliance; some unlicensed platforms pose fund security hazards.

When choosing, consider the following factors:

- Whether security measures are comprehensive

- Whether transaction control is sufficient

- Whether payment methods are flexible

Anti-Freeze Card Comparison

Anti-freeze cards perform differently across the three methods. In OTC platform cashouts, anti-freeze cards effectively avoid bank freezing risks and ensure smooth arrival of large funds. In P2P trading, anti-freeze cards enhance multi-channel receipt security, suitable for high-frequency trading. In third-party payment card methods, anti-freeze cards help bypass sensitive tags and improve fund flow efficiency. Reasonably allocate anti-freeze cards based on fund size and transaction frequency to ensure fund security.

User Selection Recommendations

If you pursue high efficiency and large fund flows, choose OTC platforms combined with anti-freeze cards. If you value transaction flexibility and privacy, P2P trading is more suitable, but strengthen security precautions. If you want global spending and cross-border payments, third-party payment cards are the most convenient. When choosing, combine your needs, fund size, and compliance requirements; prioritize platforms with comprehensive security measures, such as Biyapay, to ensure fund security and liquidity.

If what you really care about is whether the funds can arrive smoothly and whether the source of funds can be explained later, it is often more useful to review the cash-out path and conversion cost before focusing only on speed. You can first use BiyaPay’s exchange rate lookup tool to estimate the rough cost of converting USDT into the currency you actually need, and then use the official website to understand how its multi-asset trading wallet is used across cross-border payments, trading, and fund management scenarios. The practical benefit is that you can review both “how to cash out” and “how the funds will be used afterward” within the same workflow. BiyaPay covers payment, trading, and asset-management scenarios, and has relevant registrations and licensing disclosures in jurisdictions including the United States and New Zealand, which is the kind of information worth checking together when planning a cash-out strategy.

You can select USDT cashout methods based on your needs. OTC platforms suit large fund flows, P2P trading is flexible, and third-party payment cards facilitate global spending. USDT has strong global liquidity, but lacks compliance in European markets; USDC is more suitable for security-focused users. During operations, complete KYC verification, avoid abnormal large withdrawals, and confirm bank support for crypto-related deposits. Anti-freeze cards have become a key tool to safeguard fund security and will continue to improve cashout efficiency and safety in the future.

FAQ

How to choose the USDT cashout method that suits you?

You need to choose based on fund size, liquidity needs, and compliance requirements. OTC platforms suit large funds, P2P trading is flexible, and third-party payment cards facilitate global spending. Prioritize platforms with comprehensive security measures to ensure fund security.

How do anti-freeze cards specifically work in the cashout process?

Using anti-freeze cards allows you to bypass sensitive transaction tags and reduce bank freezing risks. Anti-freeze cards improve fund arrival efficiency and ensure liquidity, especially suitable for high-frequency or large transaction scenarios.

What to do if encountering bank delays or freezes during cashout?

Contact platform customer service promptly and provide complete transaction information. Choose Hong Kong licensed bank channels to increase fund arrival success rates. Anti-freeze cards can effectively reduce such risks; configure them in advance.

What compliance risks should be noted during USDT cashout?

Complete KYC identity verification and ensure legal fund sources. Avoid abnormal large withdrawals and check if the platform holds financial licenses. Compliant operations safeguard fund security and reduce freezing risks.

How do transaction fees and exchange rates affect the final received amount?

During cashout, pay attention to transaction fees, network fees, and bank transfer fees. Platforms perform conversions based on real-time exchange rates; fees and rates directly impact the final USD amount you receive.

*This article is provided for general information purposes and does not constitute legal, tax or other professional advice from BiyaPay or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or warranties, express or implied, as to the accuracy, completeness or timeliness of the contents of this publication.

Related Blogs of

Which Products Are Affected by NAND Price Increases? SSDs, Smartphones, Servers, and Consumer Electronics

What Is the Difference Between HBM Stocks and GPU Stocks?

Why Look at HBM and Storage After GPUs? Breaking Down the AI Infrastructure Investment Chain

Which Storage Chip Concept Stocks Are There in 2026? Classification of Related U.S. and Hong Kong Companies

Choose Country or Region to Read Local Blog

Contact Us

BIYA GLOBAL LLC is registered with the Financial Crimes Enforcement Network (FinCEN), an agency under the U.S. Department of the Treasury, as a Money Services Business (MSB), with registration number 31000218637349, and regulated by the Financial Crimes Enforcement Network (FinCEN).

BIYA GLOBAL LIMITED is a registered Financial Service Provider (FSP) in New Zealand, with registration number FSP1007221, and is also a registered member of the Financial Services Complaints Limited (FSCL), an independent dispute resolution scheme in New Zealand.