How to Withdraw U.S. Stock Dividends? Seamless Conversion to Fiat or Reinvestment Cycle Strategy in Crypto

Image Source: pexels

During the process of withdrawing dividends from U.S. stocks, you must focus on the efficiency and safety of fund flows. Many investors easily fall into some common pitfalls, such as:

- Mistaking dividends as new income, ignoring their impact on the value of the investment account.

- Failing to declare taxes promptly after withdrawing dividends, leading to tax risks.

- Overlooking the long-term return potential of dividend reinvestment.

You need to rationally plan fund management, pay attention to handling fees, tax policies, and fund safety to avoid the above mistakes. Standardized fund flow operations can effectively improve asset appreciation efficiency.

Key Takeaways

- Pay attention to the dividend arrival process, understand key dates, and ensure timely receipt of dividends.

- Rationally manage dividend funds, choose appropriate withdrawal methods, and improve fund liquidity.

- Understand tax compliance requirements, ensure timely tax declaration, and avoid legal risks.

- Select compliant exchange channels, compare handling fees and arrival times, and optimize fund flows.

- Regularly review your investment portfolio, flexibly adjust strategies, and achieve long-term steady asset growth.

Dividend Arrival Process

Dividend Distribution Methods

When you hold U.S. stocks, the company will distribute dividends to your broker account according to the established process. The entire process typically includes the following key dates:

- Declaration Date: The company officially announces it will pay dividends.

- Ex-Dividend Date: You need to hold the stock before this date to qualify for the current dividend.

- Record Date: The company determines which shareholders are eligible for the dividend.

- Payment Date: Dividend funds actually enter your broker account.

You can choose cash dividends or automatically reinvest dividends into more shares through a Dividend Reinvestment Plan (DRIP). Many brokers support DRIP, which helps you achieve long-term compound growth.

Account Types & Arrival Time

Different broker account types affect the speed and management method of dividend arrival. Generally, standard U.S. stock brokerage accounts receive dividend funds on the payment date or within a few days afterward. Some brokers provide automatic notifications and dividend details, making it convenient for you to track funds at any time. When choosing a broker, focus on arrival efficiency and fund management tools.

Dividend Fund Management

After receiving dividends, you can choose to keep them in the broker account, participate in DRIP, or perform U.S. stock dividend withdrawal operations. Rational management of dividend funds helps improve asset liquidity and returns. You should regularly check dividend details and decide whether to reinvest or transfer funds based on your investment goals. Some brokers also provide dividend history reports, facilitating your tax declaration and asset planning.

U.S. Stock Dividend Withdrawal Methods

Fund Withdrawal Process

After receiving U.S. stock dividends, you can withdraw funds to your bank account through the broker platform. Typically, brokers offer multiple withdrawal methods, including wire transfer (Wire Transfer), ACH transfer, and check mailing. You need to log in to the broker backend, select the “Fund Withdrawal” function, fill in bank account information, and confirm the withdrawal amount. When withdrawing U.S. stock dividends, it is recommended to verify the receiving conditions of your bank account in advance to ensure it supports USD deposits. Some brokers support automated withdrawal processes, with funds automatically transferred to your bank account within the specified cycle. You can choose one-time withdrawals or regular automatic withdrawals based on your needs, improving fund liquidity.

Handling Fees & Arrival Time

During U.S. stock dividend withdrawals, you must pay attention to handling fees and arrival time. Fee standards vary across brokers and banks. The following are common fees and time arrangements:

- Wire Transfer: Handling fees usually range from $25–35, with arrival in 1–3 business days.

- ACH Transfer: Lower fees—some brokers waive them entirely—with arrival in 2–5 business days.

- Check Mailing: Handling fees about $5–10, with longer arrival time, possibly exceeding one week.

You need to note that some banks charge additional incoming fees upon receipt. It is recommended to consult your bank’s customer service in advance to understand specific fee standards. During U.S. stock dividend withdrawals, arrival speed is limited by broker processing efficiency and bank systems. You can query withdrawal progress in real time through the broker backend to ensure funds arrive safely.

Compliance & Tax Considerations

During U.S. stock dividend withdrawals, you must strictly comply with tax requirements. The U.S. tax authority applies a withholding tax policy on dividend income for non-U.S. tax residents. You need to understand tax rates and declaration methods for different account types. The following are the main tax compliance points:

- Non-U.S. tax residents typically face 30% withholding tax.

- Canadian residents can enjoy a reduced 15% withholding tax rate by submitting Form W-8BEN.

- Withholding tax paid from non-registered accounts can be claimed as foreign tax credit (FTC) or deduction during Canadian tax filing.

- U.S.-source dividend income in certain registered retirement accounts (such as RRSP, RRIF, and LIRA) may be exempt from withholding tax, but this does not apply to Canadian mutual funds or ETFs held.

- U.S.-source dividend income received in other registered accounts (such as TFSA, FHSA, RESP, and RDSP) still faces 30% withholding tax, possibly reduced to 15%.

During tax declaration, you need to combine account type and dividend source to reasonably apply for tax rate reductions and foreign tax credits. After withdrawing U.S. stock dividends, it is recommended to retain dividend details and tax withholding records for subsequent declaration and compliance review.

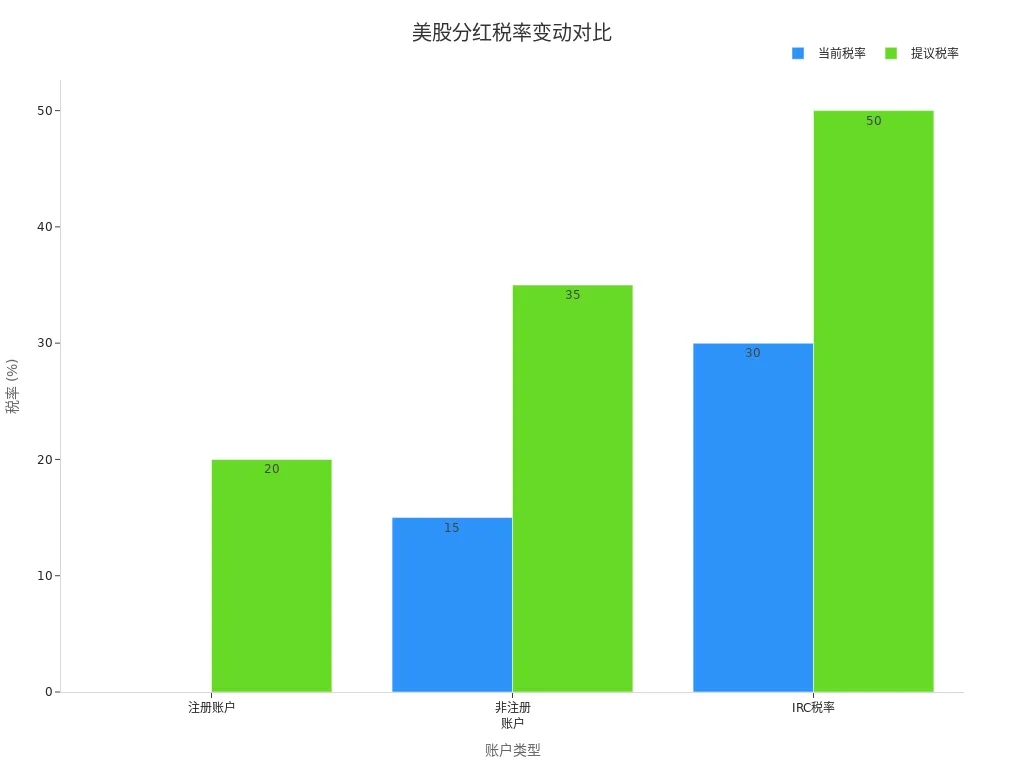

Recent regulatory changes may affect tax rates and declaration methods for U.S. stock dividend withdrawals. You need to monitor policy adjustments and update operational strategies promptly. The table below shows a comparison of current and proposed tax rates for three account types:

| Tax Type | Current Rate | Proposed Rate | Notes |

|---|---|---|---|

| Registered Accounts | 0% | 20% | May apply |

| Non-Registered Accounts | 15% | 35% | May apply |

| IRC Rate | 30% | 50% | May apply |

You can intuitively understand tax rate change trends across different account types through the chart below:

During U.S. stock dividend withdrawals, you must pay attention to tax rate changes and compliance requirements, rationally plan fund flows and tax declarations. It is recommended to consult professional tax advisors regularly to ensure operations comply with the latest regulations and avoid tax risks.

Dividend Conversion to Fiat Process

Image Source: pexels

Common Conversion Channels

After receiving U.S. stock dividends, you usually need to convert USD funds to fiat currency to meet daily consumption, asset allocation, or reinvestment needs. Current mainstream conversion channels mainly include the following categories:

- Hong Kong Licensed Banks: You can complete USD-to-fiat (such as RMB, HKD, etc.) conversion and withdrawal through Hong Kong licensed banks. The Hong Kong banking system offers high internationalization and compliance, supporting multi-currency account management with efficient fund flows. After opening a Hong Kong bank account, you can directly withdraw U.S. stock dividends to that account and then perform fiat conversion based on actual needs.

- Third-Party Cross-Border Payment Platforms: Emerging cross-border payment platforms like Biyapay provide convenient USD-to-fiat services for Chinese-speaking users. You can transfer U.S. stock dividend funds to your Biyapay account—the platform supports multi-currency conversion and flexible withdrawals with simple operations and fast arrival. Biyapay excels in compliance, fund safety, and user experience, especially suitable for Chinese users needing efficient fund flows and multi-currency management.

- Broker Built-in Conversion Services: Some international brokers provide direct USD-to-fiat conversion services for users. You can initiate a conversion request in the broker backend—the system automatically completes the conversion at real-time exchange rates and transfers to the designated bank account. This method suits users with simple fund flow path requirements, but exchange rates and fees are usually less competitive than professional payment platforms.

- Digital Currency Channels: Some users choose to convert USD dividends into stablecoins (such as USDT, USDC), then achieve fiat conversion through cryptocurrency trading platforms. This method offers flexible fund flows but involves compliance and risk management issues—operate with caution.

When choosing conversion channels, you should comprehensively consider arrival speed, handling fees, exchange rates, compliance, and fund safety. For Chinese-speaking users pursuing efficiency and multi-currency management, third-party platforms like Biyapay offer clear advantages. Hong Kong licensed banks are suitable for users with higher requirements for compliance and fund safety.

Exchange Rates & Limits

During dividend conversion to fiat, exchange rates and limits are key factors affecting fund efficiency and cost. Exchange rate policies, conversion limits, and handling fee standards vary significantly across channels and platforms. The following are the main reference points:

- Exchange Rate Policy: Hong Kong licensed banks typically use international mainstream forex rates—transparent but with large fluctuations. Third-party platforms like Biyapay price based on real-time market rates; some platforms support rate locking to help you avoid short-term exchange rate fluctuation risks. Broker built-in conversion services generally offer slightly worse rates than banks and third-party platforms—you need to pay attention to actual received amounts.

- Fee Structure: Hong Kong banks charge $15–30 per transaction for USD-to-fiat conversion; some premium accounts enjoy waivers. Third-party platforms like Biyapay have transparent fees, usually in the 0.2%–0.5% range, with lower rates during certain promotions. Broker conversion services charge 1%–2%—calculate total costs in advance.

- Conversion Limits: Hong Kong banks set upper limits on per-transaction and daily conversion amounts—common per-transaction limits are $50,000 USD, with higher daily cumulative limits possible. Third-party platforms like Biyapay support large fund flows, with per-transaction limits up to $100,000 USD or more—suitable for high-net-worth users. Broker conversion services have relatively lower limits—suitable for small-amount operations.

- Arrival Time: Hong Kong banks generally arrive within 1–2 business days; third-party platforms like Biyapay can achieve T+0 arrival at the fastest; broker services require 2–5 business days.

In actual operations, you should understand each channel’s exchange rate, handling fee, and limit policies in advance, rationally plan fund flow paths, and avoid unnecessary losses due to limits or exchange rate fluctuations.

| Channel Type | Exchange Rate Transparency | Handling Fee (USD) | Per-Transaction Limit (USD) | Arrival Time |

|---|---|---|---|---|

| Hong Kong Licensed Banks | High | $15–30 | 50,000+ | 1–2 business days |

| Biyapay Platform | High | 0.2%–0.5% | 100,000+ | T+0–T+1 |

| Broker Conversion Services | Medium | 1%–2% | 10,000–20,000 | 2–5 business days |

| Digital Currency Channels | Low | 0.1%–0.5% | Varies by platform | Depends on chain confirmation speed |

Risk Prevention & Compliance Recommendations

During dividend conversion to fiat, you must attach great importance to risk prevention and compliant operations. The following are the main recommendations:

Compliance Reminder: You must ensure all fund sources are legitimate and strictly comply with anti-money laundering (AML) and counter-terrorism financing (CFT) regulations in Hong Kong and relevant jurisdictions. Third-party platforms like Biyapay and Hong Kong licensed banks require users to complete KYC (real-name verification) processes, ensuring full traceability of fund flows.

- Fund Safety: You should prioritize licensed financial institutions or compliant third-party platforms and avoid non-regulated channels. Platforms like Biyapay adopt multiple encryption and risk control systems to protect user fund safety. Hong Kong banking systems feature comprehensive deposit protection mechanisms with high fund security.

- Information Protection: During operations, properly safeguard account information and transaction vouchers to prevent personal information leaks. It is recommended to change passwords regularly and enable two-factor authentication.

- Exchange Rate Fluctuation Risk: For large conversions, consider batch operations or rate locking features to reduce losses from short-term exchange rate fluctuations.

- Tax Compliance: You should proactively declare relevant tax information based on your residence and fund flows to avoid legal risks from non-declaration or misreporting. It is recommended to consult professional tax advisors regularly to ensure full compliance throughout fund flows.

When selecting conversion channels and platforms, you should comprehensively consider compliance, fund safety, exchange rate costs, and operational convenience. For Chinese-speaking users, compliant platforms like Biyapay and Hong Kong licensed banks provide efficient and secure solutions for dividend-to-fiat conversion. You should continue monitoring regulatory policy changes and promptly adjust fund flow strategies to safeguard asset safety and compliance.

If your main concern is how to make the next step after dividend arrival more seamless, it helps to break the path into parts: first confirm the withdrawal channel, arrival time, and fees, then use BiyaPay’s exchange rate comparison tool to review conversion cost, while checking service details and compliance disclosures on the official website. BiyaPay is positioned as a multi-asset trading wallet covering cross-border payments, investing, and fund management scenarios, so it fits naturally as a reference point in the “withdraw dividend – convert – reallocate” workflow.

Dividend Reinvestment into Cryptocurrency

Image Source: pexels

Fund Flow Process

You can withdraw U.S. stock dividend funds from your broker account to a USD-supporting bank account, then recharge to a cryptocurrency trading platform through compliant third-party platforms like Biyapay or Hong Kong licensed banks. Biyapay provides convenient USD deposit services for Chinese-speaking users, supporting multi-currency management and efficient fund flows. Within the platform, you can choose to purchase mainstream stablecoins (such as USDT, USDC) to achieve diversified asset allocation. After funds arrive, you can directly invest in cryptocurrency on the trading platform, flexibly adjust asset structure, and improve fund utilization efficiency.

Platform Selection & Safety

When choosing a cryptocurrency investment platform, you should prioritize safety and compliance. Third-party platforms like Biyapay adopt multiple encryption and strict risk control systems to protect fund safety. Among cryptocurrency exchanges, Coinbase stands out as the top choice for many professional investors due to its globally leading security standards and compliant operations. You can also indirectly participate in the cryptocurrency market through investment in related ETF products, such as the Harvest Coinbase High Income Shares ETF, which invests in Coinbase shares and combines safety with return potential. The table below shows some mainstream investment options and their features:

| Investment Option | Description |

|---|---|

| Harvest Coinbase High Income Shares ETF | Invests in Coinbase shares—Coinbase is considered the world’s safest cryptocurrency exchange. |

Investment Precautions

When reinvesting dividends into cryptocurrency, you need to focus on platform compliance, fund safety, and investment risks. It is recommended to choose licensed financial institutions or compliant third-party platforms to avoid fund losses due to unclear platform qualifications. The cryptocurrency market is highly volatile—before investing, fully understand product characteristics and risks, and rationally diversify asset allocation. You also need to pay attention to each platform’s handling fees, withdrawal limits, and fund arrival times to ensure efficient fund flows. It is recommended to regularly review your investment portfolio, dynamically adjust strategies based on your risk tolerance, and achieve long-term steady asset growth.

Cycle Strategy & Risk Reminders

Fund Cycle Management Recommendations

When formulating a fund cycle strategy, you need to actively manage fund flow paths and flexibly allocate assets. After withdrawing U.S. stock dividends, funds can efficiently flow between different markets to achieve diversified investment goals. You can adopt the following methods to improve fund management efficiency:

- Actively adjust your investment portfolio to adapt to cyclical fluctuations in the cryptocurrency market and capture growth opportunities in emerging areas such as mining, fintech, and infrastructure.

- Combine research-driven oversight mechanisms to screen out underperforming assets and avoid high-cost failures.

- Regularly review fund flow paths, optimize fund allocation, and improve overall returns.

Through active management and cyclical adjustments, you can form an efficient cycle between U.S. stock dividend withdrawal, fiat conversion, and cryptocurrency reinvestment, enhancing asset appreciation capabilities.

Main Risk Prevention

When executing cycle strategies, you must be vigilant against multiple risks. Market volatility and investment decision errors may lead to fund losses. The following risk prevention recommendations are worth attention:

- Emotional decision-making easily leads to impulsive investing—misunderstanding market cycles can cause significant losses.

- Over-investment and lack of diversification expose you to excessive risk in specific assets, making the overall portfolio vulnerable to severe losses.

- Misinterpreting market cycles may cause you to miss bear market buying or bull market selling opportunities.

- Exiting the market too early affects long-term investment returns—trading losses stem from failure to identify market phase shifts.

You need to establish scientific investment decision mechanisms, avoid emotional influences, rationally diversify assets, and dynamically adjust strategies.

Importance of Compliant Operations

During the fund cycle process, you must strictly comply with relevant regulations. Compliant operations not only safeguard fund safety but also avoid legal risks. You should prioritize licensed financial institutions and compliant third-party platforms, complete KYC certification, and ensure legitimate fund sources. Regularly consult professional tax advisors and promptly declare tax information to help avoid risks from policy changes. Through compliant operations, you can achieve safe fund flows across U.S. stock dividend withdrawal, fiat conversion, and cryptocurrency investment, improving asset management efficiency.

During the process of U.S. stock dividend withdrawal, fiat conversion, and cryptocurrency reinvestment, you should follow these key steps:

- Track dividend income, assess dividend safety, gradually expand your investment portfolio, create a dividend calendar, and actively participate in investment communities.

- Choose efficient, safe, and compliant operation paths to improve asset flow efficiency.

| Strategy Type | Description |

|---|---|

| 4% Rule | Adjust withdrawal ratios based on personal risk tolerance to ensure long-term returns. |

| Dynamic Withdrawal Strategy | Flexibly adjust fund withdrawals according to market performance, reducing volatility risk. |

| Diversified Investment | Diversify across industries and asset classes to reduce risk from single markets or companies. |

- You can use modern screening tools to evaluate company financial health, avoid high-risk dividend traps, and focus on long-term steady growth. Combine your own needs and flexibly adjust cycle strategies to effectively avoid risks from market fluctuations.

FAQ

Can U.S. stock dividends be directly converted to fiat after arrival?

You can convert through Hong Kong licensed banks, third-party payment platforms, or broker built-in services after funds arrive. Exchange rates and handling fee standards vary across channels—it is recommended to understand relevant policies in advance.

What handling fees should be noted when withdrawing to a bank account?

When withdrawing, you need to pay attention to wire transfer, ACH transfer, and check mailing fees. Wire transfers are usually $25–35, ACH transfers have lower fees, and check mailing is about $5–10. Some banks also charge additional incoming fees.

How to declare taxes after withdrawing U.S. stock dividends?

You need to declare taxes based on account type and dividend source. The U.S. applies a withholding tax policy to non-U.S. tax residents. You should retain dividend details and tax withholding records and consult professional tax advisors regularly.

How to ensure fund safety when reinvesting dividend funds into cryptocurrency?

You should choose compliant third-party platforms and globally leading cryptocurrency exchanges. Platforms must have multiple encryption and strict risk control systems. It is recommended to enable two-factor authentication and regularly review your investment portfolio.

What are the main risks in fund cycle operations?

During fund cycles, you need to be vigilant against market volatility, emotional decision-making, and platform qualification risks. Rationally diversify assets, dynamically adjust investment strategies, and strictly comply with regulations to help reduce fund loss risks.

*This article is provided for general information purposes and does not constitute legal, tax or other professional advice from BiyaPay or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or warranties, express or implied, as to the accuracy, completeness or timeliness of the contents of this publication.

Related Blogs of

What Is the Difference Between HBM3E and HBM4? What Do They Mean for Micron and AI Servers?

What Is the Relationship Between ASMPT 0522.HK and HBM? The Role of Advanced Packaging Equipment in the AI Memory Supply Chain

What Is the Difference Between DRAM Contract Price and Spot Price? Which Indicator Should Investors Watch?

What Are NOR Flash, SLC NAND, and EEPROM? Why They Help Explain Hong Kong-Listed Memory-Related Stocks

Choose Country or Region to Read Local Blog

Contact Us

BIYA GLOBAL LLC is registered with the Financial Crimes Enforcement Network (FinCEN), an agency under the U.S. Department of the Treasury, as a Money Services Business (MSB), with registration number 31000218637349, and regulated by the Financial Crimes Enforcement Network (FinCEN).

BIYA GLOBAL LIMITED is a registered Financial Service Provider (FSP) in New Zealand, with registration number FSP1007221, and is also a registered member of the Financial Services Complaints Limited (FSCL), an independent dispute resolution scheme in New Zealand.