- More

- Download

How Foreign Trade SOHO Can Settle USD Payments Most Cost-Effectively? Stay Away from Underground Money Houses

Image Source: unsplash

When choosing a method to settle USD payments, you must consider safety, compliance, and cost. Banks, third-party platforms, and agency companies each have their advantages and disadvantages. Underground money houses carry multiple risks, such as difficult regulation, highly anonymous transactions, and bypassing foreign exchange limits through stablecoins, which can easily put your funds at risk of freezing or legal issues. Choosing compliant channels allows you to stay away from these hidden dangers and ensure every payment arrives smoothly.

Key Points

- Choose compliant channels such as banks and third-party platforms to ensure fund safety and avoid legal risks.

- Bank settlement is suitable for large transactions, providing fund protection and compliance support, with processing times usually 1 to 5 business days.

- Third-party platforms like PayPal and PingPong offer convenient operations, suitable for small-amount settlements, with fast arrival times, but pay attention to compliance requirements.

- Agency companies can simplify the settlement process, but commissions are higher; choose carefully and ensure their compliance.

- Regularly review settlement channels and fees, reasonably plan settlement methods to improve fund liquidity and compliance.

Recommended USD Payment Settlement Methods

Image Source: pexels

Advantages and Applicable Scenarios of Bank Settlement

You can choose banks as the main channel for settling USD payments. Bank settlement offers high compliance and fund security, suitable for Chinese-speaking users who want stable fund arrival and larger amounts. Hong Kong licensed banks perform excellently in USD payment settlement and can meet cross-border trade needs. The bank settlement process is standardized, with transparent fund flows, complying with relevant Chinese regulatory requirements.

Bank settlement processing time is usually between 1 to 5 business days. You need to submit identity information, and the bank will check the source of funds and charge handling fees. Transfers initiated after the bank's cutoff time will be delayed to the next business day. Funds usually pass through intermediary banks, which may increase arrival time. Currency conversion is affected by bank policies and market conditions. If the bank marks it for manual review, compliance checks will extend processing time. After funds arrive at the receiving bank, additional processing time may be required.

- Applicable scenarios for bank settlement:

- You need large-amount USD payment settlement, prioritizing fund safety.

- You want clear fund flows for easy tax declaration.

- You value compliant operations to avoid legal risks.

Although bank settlement has higher handling fees, you can obtain the strongest fund protection and compliance support. You should prioritize bank channels, especially Hong Kong licensed banks, to meet cross-border trade and USD payment settlement needs.

Third-Party Platform Settlement (e.g., PayPal, PingPong)

If you pursue flexibility and ease of operation, you can choose third-party platforms for USD payment settlement. Platforms like PayPal and PingPong provide multi-currency transactions and fast arrival services for Chinese-speaking users. You can achieve personal and business cross-border collections through these platforms, suitable for small-amount settlements and efficient fund turnover.

| Platform | Advantage Description |

|---|---|

| PayPal | Supports multi-currency transactions, suitable for individual users and small businesses, simple registration, covers over 200 countries and regions, ideal for cross-border shopping and service payments. |

| PingPong | Direct settlement in multiple major currencies, reduces exchange rate conversion costs, ensures fast and secure fund arrival, suitable for B2B transactions and businesses with efficient fund needs. |

When using third-party platforms for settlement, you need to pay attention to compliance requirements. Platforms implement KYC/KYB and AML policies to protect user information and prevent money laundering and fraud. You need to cooperate with the platform to complete identity verification and ensure the legitimacy of fund sources. Platforms set transaction limits and use multi-factor authentication to safeguard fund security.

In this context, a third-party platform is more useful for document handling, process transparency, and cross-border settlement efficiency than for replacing bank review. You can first check the BiyaPay official website to understand its service scope, then review the remittance page for supported currencies, required documents, and the operating flow. As a multi-asset wallet, BiyaPay covers cross-border remittance and fund-management scenarios, and operates under relevant regulatory frameworks in jurisdictions such as the United States and New Zealand. For SOHO users with genuine trade background and clear documentation, this kind of tool works better as a compliant execution option .

| Compliance Requirement | Specific Content |

|---|---|

| KYC/KYB & AML | Non-bank payment institutions must establish sound due diligence systems to combat illegal activities like money laundering, including ongoing risk monitoring of users. |

| Data Residency & Privacy | Payment institutions protect user information, store customer data locally, emphasize transparent pricing and personal data protection. |

| Fraud Control | Payment providers implement effective risk management systems to prevent telecom fraud and other financial crimes, including transaction limits and multi-factor authentication. |

| Record Keeping & Auditing | Payment institutions maintain sound business management systems, follow specific data storage schedules, and fulfill comprehensive supervision and auditing obligations. |

You can prioritize platforms like Biyapay to meet the multi-currency settlement needs of Chinese-speaking users. Third-party platform settlement is suitable for scenarios with frequent fund turnover and moderate amounts, with simple operations and fast arrival times.

Pros and Cons of Agency Company Settlement

If you want to simplify the operation process, you can choose agency companies for USD payment settlement. Agency companies usually help you complete fund receipt, payment, and settlement procedures, suitable for users unfamiliar with bank or third-party platform operations. You need to note that agency companies charge higher commission rates, and fund safety and compliance require key attention.

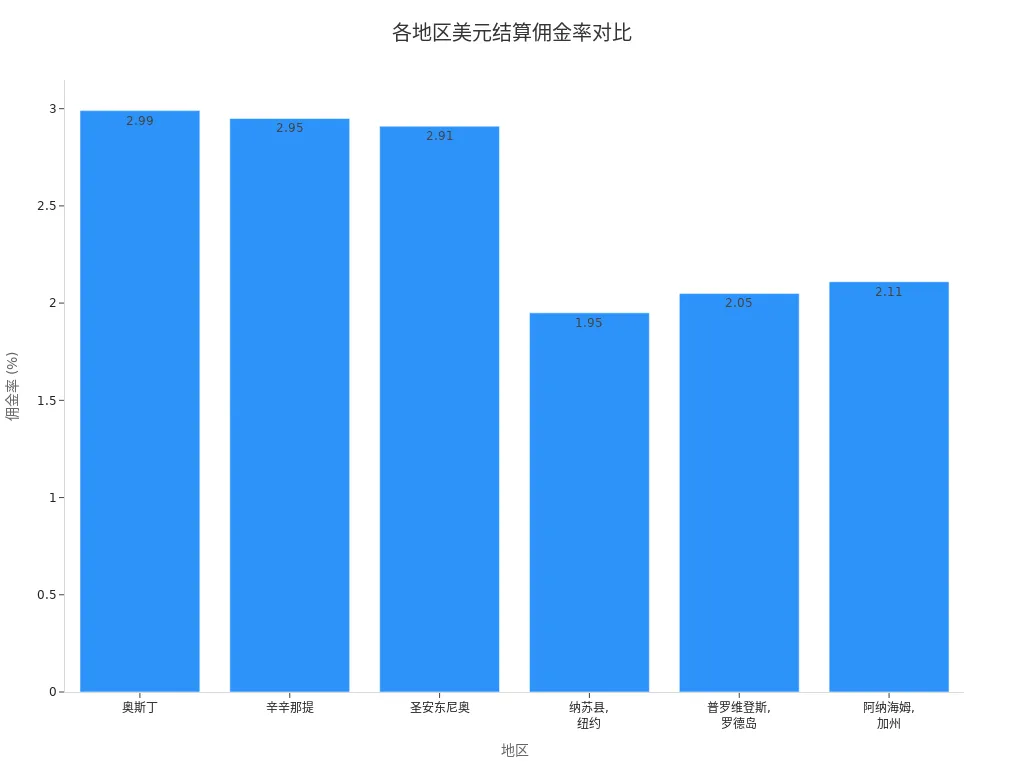

| Region | Commission Rate |

|---|---|

| Austin | 2.99% |

| Cincinnati | 2.95% |

| San Antonio | 2.91% |

| Nassau County, New York | 1.95% |

| Providence, Rhode Island | 2.05% |

| Anaheim, California | 2.11% |

When choosing an agency company, you should prioritize compliance qualifications and fund safety. Agency company settlement is suitable for users who require simple operation processes and are willing to bear higher fees. You need to be wary of illegal channels like underground money houses to avoid fund freezing or legal risks.

In the USD payment settlement process, you should prioritize banks and third-party platforms to ensure fund safety and compliance. Agency companies serve as supplementary channels for special needs, but you must strictly review their qualifications and stay away from underground money houses.

Settlement Channel Comparison

Image Source: unsplash

Fees and Arrival Speed

When choosing a USD payment settlement channel, you should first focus on handling fees and arrival speed. Bank wire transfers usually charge fixed handling fees, commonly $35 per transaction, with arrival times of 1-5 business days. Third-party platforms like Biyapay and PingPong have withdrawal fees to RMB accounts of about 0.3%, with faster arrival speeds; some platforms achieve T+1 arrival. PayPal withdrawal fees are relatively high, with noticeable exchange rate losses. Agency company settlement fees vary greatly, with some regions exceeding 2%, and arrival times affected by agency processes, possibly extending to several days. You should flexibly choose the optimal channel based on fund size and time requirements.

Fund Safety and Compliance

In the USD payment settlement process, fund safety and compliance must be prioritized. Bank channels offer the highest safety level with strict compliance reviews, suitable for large-amount settlements. Third-party platforms like Biyapay and PingPong implement KYC, AML, and other compliance policies to protect user fund safety. Although agency companies are easy to operate, some small institutions have compliance risks. You should avoid illegal channels like underground money houses to prevent fund freezing or legal risks. Compliant settlement not only safeguards funds but also aids subsequent tax declarations and fund turnover.

Quota and Tax Requirements

When settling USD payments, you need to pay attention to annual quotas and tax declaration requirements. According to Chinese foreign exchange controls, individuals can settle and remit up to USD 50,000 per year, while enterprises have an annual quota of USD 200,000. Amounts exceeding this require approval from the foreign exchange administration. Specific quotas are as follows:

| Account Type | Limit |

|---|---|

| Personal Annual Foreign Exchange Quota | Up to USD 50,000 per year |

| Enterprise Annual Foreign Exchange Quota | Up to USD 200,000 per year |

In cross-border transactions, if a single or annual settlement amount exceeds USD 50,000, tax declaration is usually required. For enterprise settlements, USD must be converted to RMB at the daily or monthly exchange rate, affecting tax calculations. Different settlement channels have varying quota and tax compliance requirements; it is recommended to plan in advance to ensure smooth and compliant USD payment settlement.

Practical Suggestions for USD Payment Settlement

How to Choose the Optimal Channel

When choosing a USD payment settlement channel, you should first clarify fund size, arrival speed, and compliance requirements. Bank channels are suitable for large-amount settlements, with high fund safety and strict compliance reviews. Third-party platforms like Biyapay are suitable for Chinese-speaking users, with convenient operations, multi-currency settlement support, fast arrival speeds, and low fees. Agency companies suit simplified process needs, but you must strictly review their qualifications. You should avoid underground money houses to ensure fund compliance. Common mistakes include using unsuitable currency channels, ignoring exchange rate fluctuations, and assuming international payments arrive instantly. You need to reasonably plan settlement methods based on your business needs to avoid fund losses.

Tips to Reduce Settlement Costs

You can effectively reduce USD payment settlement costs through the following methods:

- Use cross-border, cross-currency payments to simplify processes, reducing documentation and supplier inquiries.

- Adopt local currency payments to avoid the complexity of maintaining onshore RMB accounts.

- Accelerate fund availability; cross-border ACH payments can complete in two days, improving fund liquidity.

- Use platforms like Biyapay to support multi-currency settlement and reduce exchange rate conversion losses.

- Allow suppliers to price in RMB to lower foreign exchange risks and protect profit margins.

- Control foreign exchange conversion steps to reduce costs for small suppliers.

- Prioritize cross-border ACH payments over high-cost wire transfers to save on fees.

In the settlement process, you need to monitor exchange rate fluctuations, budget payment amounts in advance, and avoid insufficient funds due to currency depreciation. You should also regularly review settlement channels, optimize payment processes, and improve fund efficiency.

Risk Avoidance and Anti-Fraud Measures

In the USD payment settlement process, you must be vigilant against various scams and fund risks. Common scams include fake checks, lottery and sudden wealth scams, and online auction overpayment scams. You can take the following measures to prevent risks:

- Block unnecessary calls and texts to avoid leaking personal information.

- Do not provide personal or financial information in unexpected requests; legitimate institutions will not ask for sensitive information via phone or email.

- Resist pressure to act immediately; any urging for quick decisions should raise suspicion.

| Security Measure | Description |

|---|---|

| Encryption | Encrypt sensitive data during transmission to prevent unauthorized access. |

| Authentication | Verify payer and payee identities using multi-factor authentication. |

| Tokenization | Replace card information with unique tokens to reduce account information leakage risks. |

| Access Control | Restrict access to sensitive financial data; only authorized personnel can operate. |

| Firewall and Intrusion Detection | Prevent unauthorized access to financial systems and safeguard fund security. |

You also need to establish a comprehensive record-keeping strategy covering all technical platforms to avoid compliance issues. Implement effective internal controls and regular audits, using new technologies to improve information management efficiency. In the USD payment settlement process, always adhere to compliant operations, stay away from underground money houses, and ensure fund safety.

Common Questions About Settlement

Restrictions on Receiving Funds in Personal Accounts

When using personal accounts in mainland China to receive USD payments, you must pay attention to annual limits and compliance requirements. According to current policies, personal accounts can receive up to USD 50,000 per year. If you need to receive USD funds exceeding this amount, you must apply for special permission from relevant departments in advance. Additionally, banks require you to have a real-name personal account to ensure transparency of fund sources and uses.

| Restriction Type | Details |

|---|---|

| Annual Limit | Up to USD 50,000 receivable per year |

| Additional Receipt | Exceeding the limit requires special permission |

| Personal Account Requirement | Must have a personal bank account |

In actual operations, although there is no per-transaction limit for receiving international transfers, banks may require declaration based on the amount received. You should plan annual receipt quotas in advance to avoid delays in fund arrival or regulatory attention due to excess.

Tax Declaration After Settlement

After completing USD payment settlement, tax declaration becomes an important part of the compliance process. Mainland China has clear tax declaration requirements for personal and enterprise foreign exchange income. You need to truthfully declare relevant income to tax authorities based on settlement amounts, business nature, and annual totals. Enterprise users must convert USD to RMB at the daily or monthly exchange rate, include it in enterprise income, and pay taxes according to law. Individual users with large annual settlement amounts also need to pay attention to personal income tax declaration obligations.

When choosing settlement channels, banks and mainstream third-party platforms like Biyapay will provide detailed settlement vouchers and transaction records. These materials help you complete tax declarations smoothly and reduce subsequent compliance risks. You should properly keep all settlement-related documents to provide complete materials promptly during tax audits.

Tip: Truthfully declaring taxes after settlement not only protects your legitimate rights but also lays a solid foundation for subsequent fund turnover and business expansion.

Fund Freezing and Response

In the USD payment settlement process, you may encounter fund freezing situations. The US has high control over global USD settlement infrastructure, making USD funds in international transactions susceptible to regulatory influence. The US Treasury's Office of Foreign Assets Control (OFAC) enforces relevant sanctions; if your transaction counterparty or correspondent bank is on the Specially Designated Nationals (SDN) list, US correspondent banks will immediately freeze all funds in their accounts.

Common reasons for fund freezing include:

- Transactions involving sanctioned countries or individuals

- Unclear fund sources or uses

- Account information inconsistent with actual business

When encountering fund freezing, you should immediately contact the receiving bank and settlement platform to understand the specific reasons. You need to prepare complete transaction contracts, invoices, and business explanations to cooperate with the bank or platform for compliance checks. You can also consult professional lawyers or compliance advisors to strive for quick unfreezing and minimize business losses.

Suggestion: When choosing settlement channels, prioritize platforms with strong compliance and robust risk control systems, such as mainstream third-party providers like Biyapay, which can effectively reduce fund freezing risks and safeguard fund security.

In the USD payment settlement process, you should prioritize cost efficiency, arrival speed, and risk management. Choosing compliant channels like banks and third-party platforms such as Biyapay ensures fund safety and reduces fees. Cash prepayment methods like international wire transfers can effectively avoid credit risks. You need to implement KYC and due diligence measures to enhance compliance and stay away from underground money houses.

- Recommended operation steps:

- Clarify settlement amount and needs

- Prioritize compliant channels

- Provide clear remittance instructions

- Properly keep settlement vouchers

- Regularly review settlement costs and risks

Based on your business situation, reasonably plan settlement methods to ensure fund safety and compliance while supporting sustained business growth.

FAQ

How to Determine if a Settlement Channel is Compliant?

You can check whether the channel has a license issued by financial regulatory authorities. Legitimate banks and mainstream third-party platforms like Biyapay publicly disclose qualification information. You can also consult professionals to ensure the channel complies with relevant Chinese laws and regulations.

How to Avoid Fund Freezing During USD Settlement?

You need to provide complete transaction contracts and invoices. You should choose compliant channels like banks or Biyapay. You must also ensure clear fund sources and uses to avoid transactions with sanctioned countries or individuals.

How to Keep Vouchers After Settlement for Tax Declaration?

You should properly keep bank statements, settlement vouchers, and platform transaction records. You can digitize all files for easy access at any time. You should also regularly back up materials to prevent data loss.

What Are the Quota Limits for Third-Party Platform Settlement?

When settling on third-party platforms, you are usually subject to an annual limit of about USD 50,000. If you need a higher quota, you can choose a business account or apply to the platform in advance to increase the limit.

Is Agency Company Settlement Suitable for Chinese-Speaking Users?

You can choose agency companies to simplify operation processes, but you must strictly review their qualifications. You should prioritize fund safety and compliance to avoid fund risks due to irregular channels.

*This article is provided for general information purposes and does not constitute legal, tax or other professional advice from BiyaPay or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or warranties, express or implied, as to the accuracy, completeness or timeliness of the contents of this publication.

Related Blogs of

Is ASML’s Valuation Overextended After Earnings? Backlog and 2026 Guidance Risks

AMAT, LRCX, or KLAC: Which Company Benefits Most from the Semiconductor Equipment Cycle? How ASML’s Guidance Transmits Across the Supply Chain

Will PayPal Accept Stripe’s Offer? Three Major Obstacles: Board Approval, Financing, and Regulation

Where Will IBM Stock Go After Q2 Earnings? Three Scenarios Based on Revenue, Red Hat, and Free Cash Flow

Choose Country or Region to Read Local Blog

Contact Us