- More

- Download

How to Prepare Overseas Accounts: Opening, FX, Receiving Payments, and Investment Funding in One Guide

Preparing an overseas account is not only about whether you can open one. You first need to know what the account will be used for. You may need it to receive salary, collect platform payments, pay tuition or rent, exchange currency, make cross-border transfers, pay for overseas subscriptions, or fund an investment account. Different use cases determine whether you need a bank account, a multi-currency wallet, a brokerage account, or a combination of several account types. The order of preparation also matters: define your source of funds and purpose first, then organize identity proof, address proof, tax residency information, and source-of-funds documents, and finally test the route with small transactions. This can reduce the risk of failed payments, high FX costs, rejected deposits, or account reviews.

Key Takeaways

- Before preparing an overseas account, define the use case first, then choose a bank, wallet, brokerage, or multi-currency setup.

- Account opening documents usually include identity proof, address proof, tax residency information, and source-of-funds explanation.

- FX conversion should not be judged only by the displayed rate; compare spreads, fees, settlement routes, and account limits.

- Cross-border receiving requires careful checks of account name, SWIFT, IBAN, routing number, and payment reference.

- Investment funding often requires an account in your own name and may involve tax forms such as W-8BEN.

- For large fund movements, keep contracts, bank statements, salary records, investment records, or asset-sale documents.

Step One: Define the Use Case and Fund Route for Your Overseas Account

The first step in preparing an overseas account is not submitting an application immediately. It is writing down the account’s purpose and the fund route. You need to know where the money comes from, which currency it enters in, whether it needs to be converted, and whether it will ultimately be used for daily spending, receiving payments, investment funding, or transfer back. If the purpose is unclear, you may later face account mismatch, failed receiving, rejected brokerage deposits, or requests for additional compliance documents. An overseas account is not an isolated account; it is part of a fund flow.

You can divide your needs into four categories. The first is a daily-use account, such as for study abroad, work, rent, bills, and living expenses. The second is a receiving account, such as for salary, freelance income, platform settlement, business income, and client payments. The third is an FX and payment account, used for converting between HKD, USD, EUR, RMB, and other currencies, as well as cross-border remittances. The fourth is an investment account, used for funding US stocks, Hong Kong stocks, funds, bonds, or other asset transactions.

Distinguish Four Common Types of Overseas Accounts

An overseas bank account is suitable for formal receiving, large transfers, study-abroad living expenses, salary payments, property payments, and situations where bank statements are needed. Its advantages are formal records, clear account ownership, and higher institutional acceptance. Its disadvantages include account-opening thresholds, account maintenance fees, transfer fees, and stricter compliance reviews.

A multi-currency wallet is suitable for small cross-border payments, exchange-rate monitoring, staged FX conversion, and daily receiving or payment needs. It is usually more flexible, but availability, supported currencies, limits, fees, and fund protection vary by platform. You should not judge it only by whether the app is easy to use; you also need to check whether it can complete real receiving and transfers.

A brokerage account is suitable for investment trading, but it is usually not suitable as a general receiving account. Its core functions are receiving deposits that meet platform rules, placing trades, keeping transaction records, and processing withdrawals. If you use a brokerage account as a third-party receiving or transit account, it may trigger refunds, restrictions, or additional reviews.

A business or freelancer account is suitable for business receipts, platform settlements, supplier payments, and invoice management. If you use a personal account to receive funds that clearly look like business payments, the bank or platform may ask you to explain the source of funds, client relationship, invoices, and contracts.

Map Out the Fund Route

Before preparing the account, you can use a simple route map:

Source of funds → Receiving account → FX route → Use case → Withdrawal or later asset arrangement

The source of funds may be salary, savings, bonus, investment sale proceeds, business income, property sale proceeds, family gift, or loan. The receiving account may be a local bank, overseas bank, multi-currency wallet, or payment platform. The fund exit may be living expenses, tuition, rent, supplier payments, brokerage deposits, cross-border remittances, or asset allocation. Each step may involve limits, fees, settlement time, reviews, and supporting documents.

| Account use case | More suitable account type | Documents to prepare | Main risk |

|---|---|---|---|

| Study abroad and daily living | Overseas bank account, multi-currency wallet | Passport, visa, address proof, school documents | Settlement delays, FX costs, account limits |

| Salary and employment income | Overseas bank account | Identity proof, employment contract, tax information | Employer may not accept non-local accounts |

| Freelance receiving | Business account or payment platform | Contracts, invoices, business description, platform records | Personal account receiving business funds may be reviewed |

| Large FX conversion | Bank account, compliant FX tool | Bank statements, source-of-funds proof | Larger spreads and source-of-funds review |

| Investment funding | Bank account, brokerage account | Same-name account, tax forms, funding instructions | Third-party funding may be rejected |

| Cross-border remittance | Bank account, multi-currency wallet | Recipient details, SWIFT, payment reference | Incorrect details, returned funds, unclear fees |

You should also separate your “primary account” from your “tool account.” A primary account handles important funds such as salary, large savings, tuition, or investment capital. A tool account is used for FX conversion, staged payments, or temporary receiving. This structure makes the fund route clearer and makes it easier to identify the source of delays or extra fees when problems occur.

Summary: Overseas account preparation should start from the use case, not from opening an account first and deciding later. You should define the source of funds, receiving method, currency, final use, and later transfer route before choosing a bank account, multi-currency wallet, brokerage account, or business account. A clear purpose makes account-opening documents easier to prepare. A clear route reduces FX and receiving errors. A clear source of funds makes large-transaction reviews easier to handle. For most users, one overseas account cannot solve every problem. A more practical setup is to assign different accounts to different tasks: bank accounts for formal and large funds, multi-currency tools for efficiency, and brokerage accounts only for compliant investment funding and trading.

What Documents Do You Need to Open an Overseas Account?

Opening an overseas account usually requires identity proof, address proof, tax residency declaration, contact details, occupation information, and source-of-funds explanation. Requirements vary by country, bank, and account type, but the underlying logic is the same: the financial institution needs to confirm who you are, where you live, your tax status, the account purpose, and whether the account funds come from a legitimate source. The more consistent your documents are, the more stable the account opening and later use will be. The more vague the documents are, the more likely you will be asked for additional clarification.

Common Documents for Personal Accounts

The most common document for personal account opening is identity proof. This can include a passport, national ID card, local identity document, residence permit, visa, driver’s license, or local tax identification number. Accepted documents vary by institution. For online account opening, the system may require document photos, a selfie video, or NFC passport chip reading.

The second category is address proof. Many banks require a recent utility bill, bank statement, government letter, lease agreement, tax notice, or phone bill. For example, HSBC International Banking lists identity proof, address proof, employment income, and tax information among overseas account opening materials. HSBC Singapore also states that applicants may need to provide original proof of identity and latest address proof, such as a passport, utility bill, phone bill, government-issued identity document, or bank statement.

The third category is tax and occupation information. You usually need to provide tax residency, tax identification number, employer, occupation, income range, expected account transaction size, and account purpose. Do not confuse nationality, residence, and tax residency. For example, holding a passport from one country does not automatically make you a tax resident there. Traveling temporarily in another place does not necessarily change your tax residency.

Common Documents for Business and Freelancer Accounts

Business accounts are usually more complex than personal accounts. You may need to provide a certificate of incorporation, business registration, articles of association, directors and shareholders list, ultimate beneficial owner information, business description, website, contracts, invoices, client sources, business bank statements, and tax documents. If your company has multiple shareholders or a cross-border structure, the bank may also ask for explanations of actual controllers, source of funds, and operating countries.

Freelancers should also prepare business evidence. Even if you do not have a company, you may still need client contracts, platform income records, invoices, service descriptions, payment screenshots, tax filings, or bank statements. Do not treat long-term freelance income as vague “personal transfers,” because that creates a mismatch between account use and fund nature.

How to Improve Approval Stability Before Applying

The core principle of account-opening documents is that they should be consistent, clear, and verifiable. Your name spelling should match your passport. The name and address on your address proof should match the application information. Tax residency should be stated truthfully. Source of funds and account purpose should match your occupation and expected transaction scale.

| Document type | Common documents | Purpose | Common mistake |

|---|---|---|---|

| Identity proof | Passport, ID card, residence card, driver’s license | Confirms account holder identity | Expired document, blurred photo, inconsistent name spelling |

| Address proof | Utility bill, bank statement, lease, government letter | Confirms residential address | Too old, incomplete address, unclear screenshot |

| Tax information | Tax residency, tax ID, self-certification | Supports CRS, FATCA, and related rules | Treating nationality as tax residency |

| Occupation and income | Employer details, payslips, income range | Assesses account usage reasonableness | Income does not match expected transaction scale |

| Source of funds | Bank statements, contracts, asset-sale records | Supports explanations for large transactions | Showing only balance, not source |

| Account purpose | Study, receiving, investment, FX explanation | Assesses account suitability | Description too vague or inconsistent with transactions |

Before applying, you can do three things. First, convert all documents into clear PDFs or photos, avoiding excessive compression. Second, prepare your English address and name spelling and make sure they match your documents. Third, think through the account purpose in advance. Do not provide an untrue purpose just to increase the chance of approval. A false purpose may pass in the short term, but if later transactions do not match it, the account may be more easily restricted.

Summary: The core of overseas account opening is KYC and compliance, not simply uploading a few photos. The institution needs to confirm your identity, address, tax residency, occupation, source of funds, and account purpose. Personal accounts usually require identity proof, address proof, and tax information. Business and freelancer accounts also require business documents, contracts, invoices, and beneficial owner information. Before applying, the most important thing is consistency: name, address, documents, tax status, and fund purpose should all explain each other. The more complete your documents are, the smoother future FX conversion, receiving, investment funding, and large transfers will be when additional reviews arise.

How to Use an Overseas Account for FX Conversion and Receiving Payments

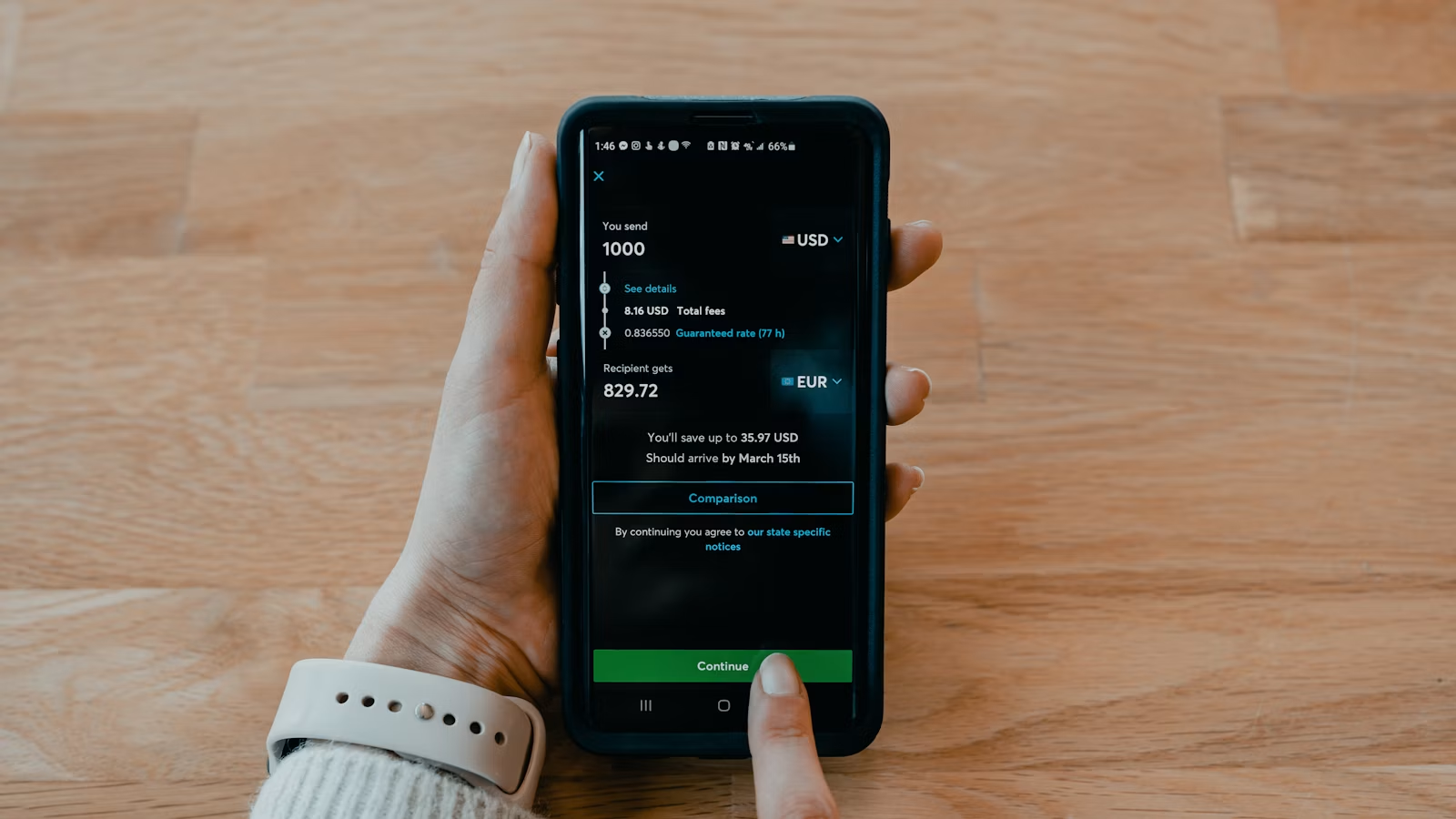

FX conversion and receiving payments through an overseas account require attention to currency, settlement route, fees, and account name. You cannot compare only the displayed exchange rate. You also need to confirm whether the account supports the currency, whether the payer can transfer using the correct information, whether SWIFT, IBAN, Routing Number, Sort Code, Bank Code, or Branch Code is needed, and whether the platform may require source-of-funds proof. For FX conversion, the key is the final arrival amount. For receiving payments, the key is correct routing, clear purpose, and consistent information.

Compare the Real Arrival Amount Before Converting Currency

FX cost is not only the exchange rate. The true cost usually consists of four parts: exchange-rate spread, fixed fee, transfer or withdrawal fee, and time cost. For small conversions, fixed fees may represent a larger percentage. For large conversions, the FX spread is often more important. You should compare different channels using the same amount, same currency, and same receiving account, rather than looking only at the exchange rate displayed on one platform’s homepage.

A practical comparison can be done in three steps. First, input the same amount and see how much of the target currency each channel says will arrive. Second, record the fee details, including platform fees, bank fees, intermediary bank fees, and withdrawal fees. Third, confirm estimated arrival time and refund rules. If a channel offers a better exchange rate but is slower, requires more documentation, or is not accepted by the recipient, it may not be the best route.

If you only want to observe exchange-rate movement, real-time exchange rates can help you establish a market reference before confirming the final quote with a bank or platform. Real-time FX tools are useful for early comparison, but the actual execution should still follow the final quote shown on the order page, bank board rate, or platform confirmation.

How to Check Receiving Details

The most common problem in cross-border receiving is incorrect information or account-name mismatch. You should verify the account name, account number, bank name, bank address, SWIFT/BIC, IBAN, Routing Number, Sort Code, Bank Code, Branch Code, and payment reference. Different countries use different fields. Europe commonly uses IBAN, the US commonly uses Routing Numbers, the UK commonly uses Sort Codes, and Hong Kong or Singapore may involve Bank Code, Branch Code, or SWIFT.

The account name should preferably match the identity document, bank record, and payment platform registration name. If you ask a client, employer, or family member to send money, the payment instruction should be clear. Incorrect references, spelling mistakes, or a recipient account that does not support the currency may cause delays, returned funds, or extra charges. Before using a bank wire, SWIFT lookup can help verify bank identification details and reduce basic risks caused by incorrect bank codes.

Prepare Documents for Large FX Conversion and Receiving

When large funds come in or are converted, the bank or platform may ask you to explain the source and purpose of the funds. Wise’s large-transfer information says users may need to provide documents for a large transfer, such as proof related to salary, loans, investments, business income, or other sources. Wise also explains that it may ask users to prove the source of funds to meet regulatory and risk-control requirements.

| Stage | What to confirm | Common fees | Main risk |

|---|---|---|---|

| FX quote | Rate, spread, fee, quote validity | Spread, platform fee | Looking only at rate, not arrival amount |

| Local transfer | Account name, account number, local clearing details | Local transfer fee | Name mismatch or insufficient limit |

| Cross-border remittance | SWIFT, IBAN, Routing Number, etc. | Wire fee, intermediary fee | Returned funds due to wrong details |

| Platform receiving | Supported currency, account type, recipient information | Withdrawal fee, FX fee | Source of funds may need explanation |

| Large incoming funds | Contracts, invoices, payslips, statements | Review time cost | Account restriction due to insufficient documents |

| Withdrawal | Receiving account, withdrawal limits, processing time | Withdrawal fee, bank receiving fee | Large withdrawal from new account may be reviewed |

For large receiving, keep documents ready in advance. Personal funds can be supported with payslips, tax documents, bank statements, asset-sale documents, investment sale records, inheritance documents, or gift explanations. Business funds can be supported with contracts, invoices, purchase orders, delivery records, tax documents, and client communication records. You may not be asked for documents every time, but when a review begins, complete documents can significantly reduce communication costs.

Summary: FX conversion and receiving payments through overseas accounts should not be judged only by the exchange rate. The real comparison should focus on final arrival amount, fee details, settlement time, whether the account supports the currency, and whether receiving information is fully correct. Cross-border receiving especially requires careful checks of account name, SWIFT, IBAN, Routing Number, Sort Code, Bank Code, and payment reference. Large funds also require source-of-funds and purpose documents in advance. A safer approach is to test the route with a small amount first, then gradually increase the amount; save contracts and statements before receiving or converting large funds; and confirm recipient rules before choosing a bank, wallet, or FX platform.

What to Check Before Using an Overseas Account for Investment Funding

If you plan to use an overseas account for investment funding, you must first confirm which funding sources the broker or trading platform accepts, whether it requires an account in your own name, which currencies and transfer methods are supported, and whether tax documents are needed. An investment account is not a normal receiving account. Using the wrong route may cause deposits to be returned, delayed, or subjected to extra document requests. You also need to understand the fee structure before funding, because investment costs usually include more than commission. They may also include platform fees, external institution fees, trading activity fees, settlement fees, remittance fees, and FX spreads.

Brokerage Account Opening and Tax Documents

International brokers usually require identity proof, address proof, tax status, occupation, income, asset information, and investment experience. Charles Schwab International lists passport or government ID, proof of residence, employer information, and tax ID among account-opening materials. Requirements vary by broker, but the core logic is the same: the platform needs to confirm client identity, tax status, risk tolerance, and source of funds.

If you are a non-US person investing in US markets, one common document is W-8BEN. The IRS explains that Form W-8BEN is generally provided by a foreign individual who is the beneficial owner of relevant income when requested by a withholding agent or payer. Brokers usually ask you to complete or update tax forms during account opening to confirm foreign status and tax treatment. Completing a tax form does not mean you are tax-free, and it does not mean all income is subject to the same rate. The broker, tax rules, and personal situation should be treated as the final basis.

Investment Funding Routes and Same-Name Account Requirements

The three most important points for investment funding are account name, currency, and route. Many brokers require funds to come from a bank account in your own name. Some platforms reject third-party payments, company-account payments, or funds from unclear sources. Even if the money ultimately belongs to you, a mismatch between the sending account name and brokerage account name may lead to a return or a request for explanation.

Interactive Brokers notes in its funding instructions that wire instructions differ by currency and that clients need to create a deposit notification in the system. If funds are sent to a non-designated currency account, they may be rejected or automatically converted into the local currency according to bank policy. When using the Interactive Brokers funding instructions, choose the currency and funding method first, then provide the generated receiving details to your bank. Do not wire funds based on old records or screenshots from someone else.

Check Trading Costs Before Funding

If you are interested in overseas markets or trading opportunities after a popular IPO lists, you should look not only at price volatility but also at actual trading costs. US stock trading costs often include more than commission. They may include platform fees, external institution fees, trading activity fees, settlement fees, remittance costs, FX costs, and selling-related fees. Different platforms display costs in different ways. Some break them down clearly, while others reflect part of the cost in the exchange rate or order page.

Biya lists US stock trading commission as USD 0, while platform fees, external institution fees, and other charges are subject to the fee center and order page display. Service availability depends on the user’s location, identity verification result, platform rules, and applicable laws and regulations. Popular IPOs or highly volatile stocks may experience significant price swings after listing, so you should understand order types, fee structures, and risks before trading. If services are available in your location and under your account conditions, you can use Biya fee displays and order information as part of your assessment of trading costs after funding an overseas account.

| Check item | Why it matters | Possible consequence if wrong | Practical suggestion |

|---|---|---|---|

| Funding account name | Proves funds come from you | Third-party deposit may be returned | Use a bank account in your own name |

| Funding currency | Affects settlement and trading | Automatic FX or rejection | Select currency according to broker instructions |

| Deposit notification | Helps broker match funds | Delay or unidentified funds | Generate notification in the system before wiring |

| Tax documents | Affect withholding and account status | Abnormal trading or income handling | Complete W-8BEN or other required forms |

| Remittance fees | Affect actual funding cost | Arrival amount lower than expected | Compare wire and intermediary costs |

| Trading fees | Affect actual investment cost | Underestimating transaction cost | Check fee structure and order details |

If you are still in the research stage, you can use US stock lookup to review basic information, quotes, and market details before deciding whether to fund. Research, FX conversion, funding, and trading should be handled separately. Do not rush a transfer because of short-term market sentiment when account rules and fund routes have not yet been confirmed.

Summary: Using an overseas account for investment funding is usually stricter than an ordinary transfer. You need to confirm the broker’s supported currencies, funding methods, receiving account, same-name requirement, and tax documents before sending money from an account in your own name according to instructions. Do not treat a brokerage account as a normal receiving account, and do not fund it through a third-party route that the platform does not accept. You should also understand total costs before funding: remittance fees, FX spreads, platform fees, external institution fees, and trading activity fees can all affect capital efficiency. A safer process is to complete brokerage account opening and tax forms first, generate a deposit notification, test with a small or controlled amount, and only then arrange larger funds.

Tax, Compliance, and Risk Controls for Overseas Accounts

The key compliance issues for overseas accounts include real identity, tax residency, source of funds, account purpose, and reporting obligations. You should not treat an overseas account as a tool to avoid regulation or hide assets. Financial institutions identify customers and account information under KYC, AML, CRS, FATCA, and related rules. Large or unusual fund movements may also trigger additional reviews. Successfully opening an account is only the first step. Long-term stable use depends on whether your fund sources and transaction behavior can be explained.

CRS, FATCA, and Tax Residency

CRS is an international standard for the automatic exchange of financial account information. The OECD explains that under the Common Reporting Standard, jurisdictions obtain information from financial institutions and automatically exchange it with other jurisdictions on an annual basis. Singapore’s IRAS also describes CRS as an international standard for the automatic exchange of financial account information for tax purposes.

FATCA is related to US taxation. The IRS explains that FATCA requires certain US taxpayers to report foreign financial assets and foreign financial institutions to report financial accounts held by US taxpayers. Even if you are not a US tax resident, that does not mean you can ignore tax forms, because financial institutions may still ask you to declare non-US status or provide tax residency information.

Tax residency should be stated based on your actual situation. Do not confuse nationality, usual residence, account-opening location, and tax residence. You may hold a passport from country A, work in country B, open an account in location C, and fund a platform in location D. In that situation, tax residency should be determined based on actual residence, income, local tax law, and personal circumstances. If your situation is complex, consult a professional tax adviser.

KYC, AML, and Source-of-Funds Proof

KYC means know your customer, mainly confirming identity, address, occupation, account purpose, and risk level. AML means anti-money laundering, focusing on whether funds may involve money laundering, sanctions, fraud, tax evasion, illegal gambling, scams, or other unusual transactions. For ordinary users, compliance is not abstract. It appears in account-opening questions, transaction limits, requests for additional documents, and account reviews.

The following situations are more likely to trigger reviews: a new account suddenly has a large transaction, a long-idle account suddenly receives frequent payments, a personal account receives business funds, frequent third-party receiving or payments occur, payment references do not match the true purpose, funds come from high-risk platforms, or transaction size clearly does not match income level. A review does not necessarily mean wrongdoing, but if you do not have documents to explain the transaction, you will be in a passive position.

Behaviors That Can Lead to Account Restrictions

| Compliance topic | What you should do | What you should not do | Possible consequence |

|---|---|---|---|

| Tax residency | State truthfully and update regularly | Randomly choose a low-tax location | Additional tax declaration requests |

| Source of funds | Keep salary, contracts, statements, and tax documents | Keep only balance screenshots | Large transactions cannot be explained |

| Account purpose | Make transactions match account purpose | Use a personal account for business income long term | Account review or restriction |

| Third-party transfers | Use your own or compliant business account where possible | Frequently receive or pay on behalf of others | Funds may be frozen or returned |

| Large transaction splitting | Follow genuine payment arrangements | Split artificially to avoid review | Higher risk scoring |

| Payment reference | Use a truthful purpose | Use vague or false references | Delay, return, or document request |

You should build a “fund document folder.” Personal users can keep 3–6 months of bank statements, payslips, tax documents, investment sale records, property transaction documents, gift explanations, and important contracts. Business users can keep registration documents, invoices, client contracts, delivery proof, tax filings, and business bank statements. These documents may not be used every day, but they are very useful for large FX conversion, cross-border receiving, or investment funding.

Summary: Overseas account compliance is not an add-on; it is the foundation for stable account use. CRS, FATCA, KYC, and AML all affect how financial institutions identify accounts and fund flows. You need to state identity and tax information truthfully, keep account purpose consistent with transaction behavior, and prepare source-of-funds proof for large or unusual funds. Do not use overseas accounts to hide assets, avoid regulation, handle third-party transfers, or artificially split funds. For ordinary users, the most controllable approach is to keep records, use your own account, transfer funds for real purposes, and update identity, address, and tax residency information when they change.

Overseas Account Preparation Steps: From Opening to Normal Use

Overseas account preparation can follow seven steps: confirm purpose, organize documents, apply for the account, run a small test, handle FX and receiving, prepare investment funding, and review regularly. Do not move a large amount into a new account all at once, and do not conduct complex cross-border transactions immediately after opening the account. Test the route first, save records, and then gradually increase the amount. This builds a more stable operating rhythm across cost, limits, settlement time, and compliance reviews.

Before Opening: Confirm Needs and Documents

First, define the main purpose. Is the account for study-abroad living expenses, salary receiving, freelance income, business payments, cross-border remittances, FX conversion, or investment funding? Different purposes determine whether you need a local bank account, overseas bank account, multi-currency wallet, business account, or brokerage account.

Second, check the account-opening region and account conditions. Look at supported currencies, minimum balance, account maintenance fees, transfer fees, FX fees, remote account-opening requirements, whether residents of your country or region are supported, and whether a local address or visa is required.

Third, organize documents. These include identity proof, address proof, contact details, tax residency, occupation information, source-of-funds documents, English name spelling, and English address. For a business account, also organize company registration documents, shareholder and director information, business description, contracts, and invoices.

After Opening: Start with Small Tests

After the account is opened, do not immediately make a large FX conversion or complex transfer. First test local deposits, cross-border receiving, FX conversion, withdrawals, outgoing transfers, and statement downloads. Save receipts, screenshots, fee details, and settlement times at every step. Small tests help you discover whether receiving fields, account name, payment reference, transfer limits, and settlement time meet expectations.

If you plan to use the account for investment funding, also confirm whether the broker accepts that account and currency. Do not assume that an account that can receive money can automatically fund a brokerage account. Broker rules, bank rules, and wallet rules can be completely different.

After Normal Use: Build a Record and Review System

Once the account is in normal use, save statements and transaction records regularly. Prepare supporting documents before large fund movements. Do not wait until a bank or platform asks before looking for contracts, invoices, and statements. If your address, contact details, tax residency, occupation, or income changes, update them according to platform requirements. For accounts you do not use often, monitor maintenance fees, minimum balance, dormancy rules, and closure procedures.

| Step | What to do | Goal |

|---|---|---|

| 1. Confirm purpose | Define living, receiving, FX, investment, or business needs | Avoid choosing the wrong account type |

| 2. Choose accounts | Compare banks, wallets, brokers, and business accounts | Build an account combination |

| 3. Organize documents | Prepare identity, address, tax, and source-of-funds files | Improve account-opening stability |

| 4. Submit application | State purpose, occupation, and tax information truthfully | Avoid later mismatch |

| 5. Small test | Test deposits, receiving, FX, and withdrawals | Check route executability |

| 6. Expand use | Increase amount gradually based on test results | Control operational risk |

| 7. Review regularly | Save statements, update information, check fees | Keep the account usable long term |

You can follow this checklist:

- Confirm the main purpose of the account.

- List the source of funds and final use.

- Choose a primary account and supporting tools.

- Prepare identity proof and address proof.

- Fill in tax residency and occupation information.

- Save source-of-funds documents.

- Make a small deposit after account opening.

- Test FX conversion and outgoing transfers.

- Test whether receiving details are correct.

- Check brokerage funding instructions before investment deposits.

- Save monthly statements and transaction records.

- Prepare additional documents before large transactions.

If you need cross-border transfers after opening the account, you can use tools such as cross-border remittances in supported scenarios to help manage fund flows, while still confirming fees, settlement time, identity verification, supported regions, and applicable regulations. Different tools fit different tasks. The key is to keep the fund route clear, costs comparable, and records complete.

Summary: Overseas account preparation should be gradual. Confirm the purpose and fund route first, then choose the account type and account-opening region. Organize identity proof, address proof, tax information, and source-of-funds documents before applying. After the account is opened, run small tests before making large or complex transactions. During normal use, save statements, update identity and tax information, and review fees and limits regularly. These steps are not extra burden; they reduce the risk of failed receiving, high FX costs, rejected investment deposits, and account reviews. The more important the overseas account is, the more carefully you should build a stable usage record.

From Overseas Account Preparation to Cross-Border Money Management

After opening an overseas account, you still need to manage FX conversion, cross-border remittances, subscription payments, investment funding, multi-currency assets, and fund records. One account rarely handles every task well. A clearer approach is to combine overseas bank accounts, multi-currency tools, investment accounts, and everyday payment tools: bank accounts for formal and large-value scenarios, multi-currency tools for exchange-rate monitoring and flexible payments, and brokerage or trading accounts only for compliant investment funding and trading.

Biya is a global multi-asset trading wallet for users who need to manage cross-border payments, currency conversion, and overseas asset information at the same time. It supports USDT conversion into major fiat currencies such as USD and HKD, supports US stock, Hong Kong stock, and digital asset trading, and covers more than 190 countries and regions with over 40 local currencies. For users who have prepared overseas accounts, Biya can be part of the overall toolset for supported exchange-rate monitoring, cross-border fund arrangements, and asset management scenarios.

For US stock trading, Biya lists US stock trading commission as USD 0, while platform fees, external institution fees, and other charges are subject to the fee center and order page display. Service availability depends on the user’s location, identity verification result, platform rules, and applicable laws and regulations. The core of overseas account preparation is not to find a “universal route,” but to build a fund process that can be explained, reviewed, and used long term across account opening, FX conversion, receiving, funding, trading, and record keeping.

FAQ

What documents are usually needed to open an overseas account?

Opening an overseas account usually requires a passport or other identity proof, address proof, tax residency information, contact details, occupation information, and source-of-funds explanation. Requirements vary by country and institution, and some may also require a visa, residence permit, income proof, or local address. Always follow the actual rules of the account-opening institution.

Can an overseas account receive RMB or HKD directly?

Whether an overseas account can receive RMB or HKD directly depends on the supported currencies and receiving route. Some accounts support multi-currency receiving, while others support only local currency or designated currencies. Before receiving funds, check the account name, SWIFT, IBAN, local clearing details, and payment reference to avoid delays or returned funds.

How do you know if FX costs are high in an overseas account?

FX costs in an overseas account should not be judged only by the displayed rate. You also need to look at bid-ask spread, handling fees, transfer fees, withdrawal fees, and final arrival amount. For large conversions, compare actual arrival results across channels and check whether intermediary bank fees, platform limits, or source-of-funds reviews apply.

Can an overseas account directly fund a brokerage account?

An overseas account can fund a brokerage account only if the broker accepts that account, currency, and transfer route, and the funds usually need to come from an account in your own name. Before funding, review the broker’s instructions, create a deposit notification, verify recipient details, and confirm tax documents and fee rules.

Will overseas accounts automatically exchange tax information?

Many countries and regions participate in CRS or FATCA information exchange, and financial institutions may identify and report certain account information under the rules. Account holders should truthfully provide tax residency, tax identification numbers, and identity information, and meet reporting obligations under local tax laws. Complex cases should be reviewed with a professional tax adviser.

Why are large incoming payments to overseas accounts reviewed?

Large incoming payments to overseas accounts may trigger KYC, AML, or source-of-funds reviews. Banks or platforms may request contracts, invoices, payslips, bank statements, investment records, asset-sale documents, or other materials. The purpose and source of funds should be consistent, truthful, and explainable, and funds should not be artificially split to avoid review.

*This article is provided for general information purposes and does not constitute legal, tax or other professional advice from BiyaPay or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or warranties, express or implied, as to the accuracy, completeness or timeliness of the contents of this publication.

Related Blogs of

Lam Research Earnings Preview: Can HBM and NAND Expansion Keep Driving Equipment Orders?

Is Meta Entering AI Cloud Services? Watch Compute Sales, Broadcom Chips, and Margins Before Earnings

Meta 2026 Q2 Earnings Preview: Revenue, Ad Growth, AI Spending, and Full-Year Guidance

Will Memory Shortages Drag Down Qualcomm? China Handset Inventory, Snapdragon, and Earnings Guidance

Choose Country or Region to Read Local Blog

Contact Us