Reject Banks' High Hidden Cable Fees: Analyzing the Underlying Logic of Multi-Asset Wallets Achieving “Zero Exchange Rate Hidden Costs”

Image Source: unsplash

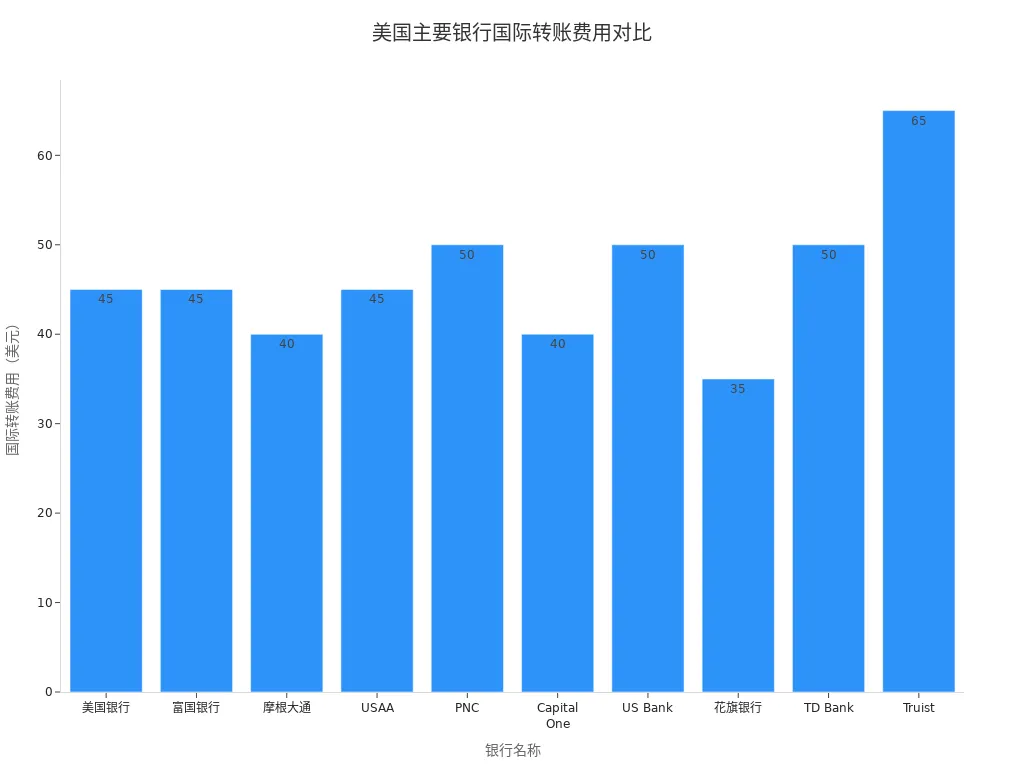

When you conduct international remittances, you often find that the cable fees charged by banks are not only expensive but also structurally complex. Taking major U.S. banks as an example, international transfer fees generally range from $35 to $65, as shown in the table below:

These hidden costs make it difficult for you to grasp the actual expenditure. By using a multi-asset wallet, you can reject banks’ high hidden cable fees and enjoy a more transparent fund flow experience.

Key Points

- Using a multi-asset wallet can help you avoid banks’ high hidden cable fees and enjoy a more transparent fund flow experience.

- Multi-asset wallets support multiple digital assets, simplifying management processes and improving fund liquidity efficiency.

- By choosing the right transfer timing and batch transactions, users can significantly reduce cross-border transfer costs.

- Blockchain technology ensures all fees are transparent, allowing users to clearly understand the specific cost of each transaction.

- Market competition and regulatory measures are driving greater transparency in financial services, enabling users to better select low-cost cross-border payment methods.

Analysis of Rejecting Banks’ High Hidden Cable Fees

Image Source: pexels

Composition of Cable Fees

When you make an international transfer, banks typically charge multiple types of fees. The cable fee is not just a simple service charge but consists of several components:

- International bank wire transfers involve multiple parties, including the originating U.S. bank, the foreign bank, and wire processing systems in both countries. Each link may charge a fee.

- Banks charge currency conversion fees when performing exchange, which covers their costs and generates profit.

- The exchange rate provided by banks usually includes a markup. The rate you see at the bank is often less favorable than the mid-market rate shown on Google or financial news websites.

You can understand the differences in domestic and international wire transfer fees among major U.S. banks through the table below:

| Bank | Domestic Wire Fee | International Wire Fee |

|---|---|---|

| Bank of America | $30 | $0 (foreign currency) / $45 (USD) |

| JPMorgan Chase | $25 (online) / $35 (branch) | $5 (foreign currency) / $40 (USD) |

| Wells Fargo | $25 | $0 (foreign currency) / $25 (USD) |

| Bank of America | $30 | $50 |

| Truist | $30 | $65 |

| Capital One | $30 | $40 |

| Citibank | $25 | $35 |

You will notice that international wire fees are significantly higher than domestic ones, with noticeable differences among banks. International wires may also incur currency conversion fees of 1% to 3%, all of which are part of the cable fee.

Manifestation of Hidden Fees

When you handle international remittances, besides the visible cable fees, you will encounter various hidden fees. These fees are often not easily noticeable but can significantly increase your actual expenditure. Common hidden fees include:

| Hidden Fee Type | Description |

|---|---|

| One-time fees vs. recurring fees | If you need to remit regularly, setting up recurring deductions may save some costs. |

| Transaction initiation fees | Depending on how you initiate the transaction, nominal fees may apply. |

| Intermediary bank fees | When sending or receiving remittances internationally, any intermediary bank involved will charge its own fee. |

| Tracing fees | If you need to trace the funds, additional fees may be charged depending on the financial institution used. |

| Exchange rate | Different institutions offer different rates, which may include markups or conversion fees. |

In actual operations, you often only see the publicly announced cable fee from the bank, while overlooking hidden costs such as intermediary bank fees and exchange rate markups. Banks usually do not proactively disclose the exact amounts of these fees, making it difficult for you to accurately calculate the real cost.

Impact on Users

When making international transfers, rejecting banks’ high hidden cable fees becomes especially important. High fees and hidden charges have long been major barriers to international transactions. You may end up paying more due to banks marking up the market exchange rate. Many times, you have no idea how much extra cost you are paying for international transfers.

| Fee Type | Description |

|---|---|

| Hidden fees | Many people are surprised by the fees charged by banks and other service providers; these hidden fees can significantly increase the total cost of international transfers. |

| Exchange rate markup | Many banks add a markup to the mid-market rate, causing you to pay extra when making international transfers. |

If you frequently make international remittances, these accumulated fees can become a considerable expense. When choosing traditional bank transfers, it is often difficult to obtain a detailed fee breakdown, making budgeting hard to control. In recent years, innovations from digital banks and fintech companies are challenging the traditional model, helping you better reject banks’ high hidden cable fees and achieve transparent and low-cost fund flows.

Advantages of Multi-Asset Wallets

Multi-Asset Integration

When choosing a multi-asset wallet, you can manage multiple digital assets simultaneously. Digital wallets not only support tokenized currencies but can also handle deposits and securities. You will find that some wallets are designed specifically for Ethereum and its ERC-20 tokens, while others support major networks like Solana or Bitcoin.

Multi-asset wallets such as BiyaPay help you consolidate different types of assets on a single platform, improving management efficiency. You no longer need to open separate accounts for each asset type, nor worry about management difficulties caused by asset dispersion.

You can refer to the table below to understand the main differences between multi-asset wallets and traditional bank accounts:

| Feature | Multi-Asset Wallet | Traditional Bank Account |

|---|---|---|

| Convenience | Instant payments and cross-border transactions | Longer processing time |

| Flexibility | Supports multiple digital assets and currencies | Usually supports only fiat currency |

| Integration capability | Seamless blockchain integration, efficient payment experience | No blockchain integration |

| Transaction speed | Distributed ledger technology enables instant settlement | Slower transaction processing |

Reduced Transaction Costs

When using a multi-asset wallet for cross-border transfers, you can significantly reduce transaction costs. Data shows that the average transaction cost for traditional banks is as high as 6.2%, while the Bitcoin network averages only 1.175%. Some digital wallet platforms charge processing fees as low as 0.2–0.7%.

Multi-asset wallets help you reduce costs through various technical methods:

- Batch transactions: Combine multiple transactions to reduce total network fees.

- Transact during off-peak hours: Choose periods of lower network traffic to further reduce fees.

- Use Layer 2 scaling solutions: Such as Bitcoin’s Lightning Network, Ethereum’s Optimism and Arbitrum, which process transactions off the main chain and batch settle, greatly reducing per-transaction costs.

Through these methods, you can effectively reject banks’ high hidden cable fees and enjoy lower fund circulation costs.

Transparent Fee Structure

When operating on a multi-asset wallet platform, all fees are displayed in detail. You can clearly see the specific costs for each transfer, exchange, or withdrawal, avoiding additional expenses due to lack of transparency.

Multi-asset wallets usually adopt blockchain technology, making all transaction records publicly verifiable and the fee structure crystal clear. You can flexibly choose the most optimal fund flow path according to your needs, enhancing initiative and security in fund management.

If your priority is to understand the cost before funds move, the practical value of this type of tool is that it breaks the charge down into visible parts.Using the BiyaPay website as an example, users can first use its exchange rate comparison tool to estimate conversion costs, then arrange cross-border transfers through its remittance service, instead of looking only at the surface fee while missing the FX spread.In practice, it functions more like a multi-asset trading wallet covering cross-border payments, FX conversion, and fund management, with relevant registrations and licenses in jurisdictions such as the United States and New Zealand, adding compliance and traceability alongside fee transparency.

In actual operations, you will experience the advantages of transparent fees and efficient processes. This model not only improves user experience but also brings you greater freedom in fund flows.

Underlying Logic of Zero Exchange Rate Hidden Costs

Image Source: pexels

Technical Implementation

When using a multi-asset wallet, you can experience the transparency and efficiency brought by blockchain technology. Blockchain networks publicly disclose all transaction fees on a public ledger. You can clearly see the specific cost of each transfer. Taking mainstream blockchains as an example, single transaction fees typically range from $2 to $15, far lower than the average $45 international transfer fee of traditional banks. This transparent mechanism allows you to directly compare costs across different channels and reject banks’ high hidden cable fees.

If you choose stablecoins (such as USDC, USDT) for cross-border transfers, you can completely eliminate currency conversion spreads. Stablecoins maintain consistent value during transfers, unlike banks that add 3% to 6% on exchange rates. On multi-asset wallet platforms like BiyaPay, you can settle directly with stablecoins, avoiding the exchange rate hidden costs of traditional banks.

| Evidence Source | Evidence Content |

|---|---|

| Blockchain networks | Blockchain networks publicly disclose transaction fees on a public ledger, with typical fees ranging from $2-15 per transaction, a 90% reduction compared to the average $45 fee of traditional bank transfers. |

| Stablecoin payments | Stablecoin payments completely eliminate currency conversion spreads because USDC or USDT transfers maintain consistent value, avoiding the 3-6% exchange rate markup imposed by banks in international transactions. |

You can also obtain transparent transaction costs through blockchain payment networks like Flexa. Blockchain technology enables near-instant forex settlement, greatly reducing costs for global trade and personal cross-border payments.

Process Optimization

When performing cross-border transfers on a multi-asset wallet platform, you can experience significant process optimization. Traditional bank transfers usually take 3 to 5 business days, involve multiple intermediaries, and are cumbersome and expensive. Multi-asset wallets use blockchain technology to achieve near-instant arrival and 24/7 availability. You are no longer limited by bank business hours and do not need to wait for complex clearing processes.

Multi-asset wallets also support batch transfer functions. You can consolidate multiple transfers into one operation, significantly reducing overall costs. Blockchain network fees usually depend on data size rather than the number of recipients. By batch processing, you can optimize network resource usage and further reduce costs. You can also use tools like ETH Gas Station or Mempool.space to monitor network congestion in real time and choose lower-fee periods for transfers.

- You can manually set transfer speed; platforms usually offer fast, medium, or slow options. If arrival time is not critical, choosing a slower speed can further save costs.

- On platforms like BiyaPay, you can hold and manage multiple currencies simultaneously, including fiat and stablecoins, simplifying operations and increasing fund flow flexibility.

By eliminating intermediary links, multi-asset wallets can reduce overall transaction costs by 60% to 80%. You can achieve local payments in over 80 markets, solving the reliability and timeliness issues of traditional bank cross-border payments.

Improved User Experience

On multi-asset wallet platforms, you can enjoy a user experience far superior to traditional banks. You can initiate and receive transfers anytime, anywhere via mobile phone, without visiting a bank branch. Wallets use encryption, two-factor authentication, and other security technologies to protect your funds at a level far higher than cash or bank card transactions.

As digital platforms, multi-asset wallets can seamlessly integrate with other business systems. In corporate or personal financial management, you can easily connect to accounting systems, simplifying transaction management and monitoring. You can also view all fee details in real time, avoiding additional expenses due to lack of transparency.

- You can experience extremely high convenience and accessibility, with fund flows unrestricted by geography and time.

- On multi-asset wallet platforms, you can manage multiple currencies simultaneously to meet diverse needs for cross-border payments and asset allocation.

- Through blockchain technology, you enjoy tamper-proof and transparent tracking advantages, eliminating risks such as chargeback fraud.

If you frequently make international remittances or cross-border payments, multi-asset wallets can help you completely break free from the process limitations and high fees of traditional banks. You can manage funds more efficiently and achieve true global asset flows.

Practical Operation Guide

Wallet Selection and Registration

When choosing a multi-asset wallet, you need to focus on several key criteria. First, ensure the wallet provides clear address traceability for compliance and fund security. You should prioritize platforms that support major blockchain networks with reliable performance to reduce transfer costs and improve arrival speed. Multi-user access control is also important, especially for enterprise users; role permissions and multi-signature features can enhance security. You also need to pay attention to the wallet’s transaction history records and documentation support for subsequent auditing and fund tracking. Some platforms are compatible with regulated off-ramp channels, offering higher compliance assurance.

BiyaPay provides a convenient registration process for Chinese-speaking users. You only need to download the app, enter your phone number and email, set a strong password, and complete identity verification to activate your account. After registration, you can immediately experience multi-asset management and cross-border payment services.

Fund Deposit and Exchange

When depositing funds in BiyaPay, first log in to your account and select the “Deposit” function. The platform supports multiple methods, including bank transfers and digital currency deposits. After selecting the deposit currency and amount, follow the instructions to complete the operation. Once the deposit arrives, you can directly perform currency exchange within the wallet. Simply go to the “Exchange” page, select the currency to exchange from and to, enter the amount, confirm the rate and fees, then submit. BiyaPay uses real-time on-chain exchange, usually completing in a few minutes, greatly improving fund flow efficiency.

Transfer Process

When initiating a transfer in BiyaPay, go to the “Transfer” function, fill in the recipient’s wallet address and transfer amount. The platform will automatically display the estimated arrival time and fees. After confirming the information is correct, submit; the system will automatically select the optimal routing based on network conditions. Most transfers complete within a few minutes, though peak periods may take longer. You can track progress in real time in the transaction history to ensure funds arrive safely.

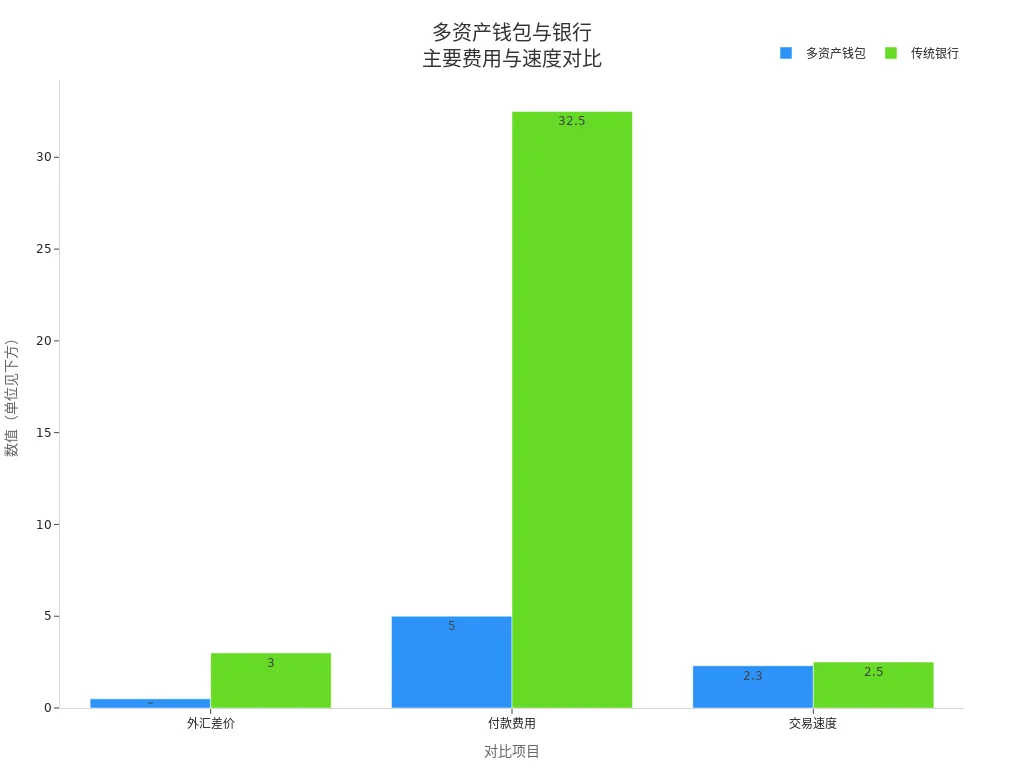

The table below shows a comparison between multi-asset wallets and traditional banks in terms of forex spread, payment fees, and transaction speed:

| Feature | Multi-Asset Wallet | Traditional Bank |

|---|---|---|

| Forex Spread | 0.5% | 2-4% |

| Payment Fee | $5 | $25-40 |

| Transaction Speed | 2.3 seconds | 2-3 days |

| Annual Savings | $30,840 | N/A |

| Real-time Visibility | Provided | Not provided |

| Logistics Tracking | Free | Not provided |

Precautions

When using a multi-asset wallet, pay attention to the following risks and security points:

- Keep your private keys secure; avoid leakage or loss, as funds cannot be recovered otherwise.

- Choose wallets that support multi-signature and audit features to improve transaction transparency and compliance.

- Pay attention to the platform’s regulatory compliance status; prioritize wallets that cooperate with regulated financial institutions.

- Understand network congestion on different chains and schedule transfers reasonably to avoid peak-hour delays.

- Non-custodial wallets are complex to operate; for first-time use, carefully read the official guide to avoid mistakes.

Through scientific selection and standardized operations, you can effectively improve fund security and liquidity efficiency, truly achieving transparent fees and efficient cross-border payments.

Market Competition and Regulatory Role

Impact of Market Competition

When choosing cross-border transfer services, you will find that market competition has significantly influenced fee structures. With the rise of fintech companies and multi-asset wallets, traditional banks are no longer the only option. You can compare fees and services across platforms and choose more efficient and transparent channels.

For example, Hong Kong licensed banks and some digital wallet platforms have lowered the threshold for international transfers through technological innovation. On these platforms, you can usually enjoy lower fees and faster arrival times. Market competition forces service providers to continuously optimize processes and improve user experience. As a user, you have more bargaining power and can actively reject banks’ high hidden cable fees, driving the entire industry toward transparency and low costs.

Market competition gives you more choices and forces traditional banks to improve service quality and reduce fees.

Regulatory Measures

During cross-border transfers, you are also protected by regulatory policies. Regulatory authorities in various countries continue to improve regulations, requiring financial institutions to disclose fee structures and prevent unreasonable charges. On compliant platforms, you can clearly see all fee details and avoid bearing extra costs due to information asymmetry.

Regulatory bodies in the United States, Hong Kong, and elsewhere promote financial service transparency, requiring banks and payment institutions to disclose all relevant fees. When choosing services, you can refer to fee standards published by regulators to rationally judge the pros and cons of different platforms.

Regulatory measures also include strict requirements for fund security and anti-money laundering. Operating on compliant platforms offers higher fund security and greater protection during transactions. By understanding regulatory policies, you can better safeguard your rights and reduce cross-border transfer risks.

You can achieve transparent fund management through multi-asset wallets. You will find cross-border payments become efficient and low-cost. You can track every transaction in real time and clearly understand all fees. When choosing new wallet tools, it is recommended to focus on security and compliance. You should reasonably evaluate platform qualifications to protect fund safety. You can try multi-asset wallets to enjoy the convenience of global fund flows. During operations, maintain rational judgment and avoid risks.

Choosing transparent and low-cost cross-border payment methods will effectively improve fund flow efficiency.

- Pay attention to secure operations to ensure funds are not lost.

- Actively understand fee structures to avoid unnecessary expenses.

FAQ

How does a multi-asset wallet protect your fund security?

You can protect funds through private key management, multi-signature, and identity verification. The platform uses encryption technology to ensure every transaction is secure and transparent. You can also view transaction records at any time to promptly detect anomalies.

How long does a transfer take using a multi-asset wallet?

Transfers are usually completed within a few minutes. Blockchain networks operate 24/7 and are not restricted by bank business hours. You can track arrival progress in real time, improving fund flow efficiency.

Is the fee structure of multi-asset wallets transparent?

On the platform, you can clearly see all fee details, including transfers, exchanges, and withdrawals. Blockchain technology makes every fee publicly verifiable, avoiding hidden costs.

How do you choose a suitable wallet platform?

You should focus on the platform’s security, compliance, and user reviews. Prioritize wallets that support major blockchain networks, offer multi-factor authentication, and have audit features. Also check whether the platform cooperates with regulated financial institutions.

Is a multi-asset wallet suitable for enterprise users?

You can use multi-asset wallets to implement multi-user permission management and batch transfers. Enterprise users can improve fund management efficiency, reduce cross-border payment costs, and meet global business needs.

*This article is provided for general information purposes and does not constitute legal, tax or other professional advice from BiyaPay or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or warranties, express or implied, as to the accuracy, completeness or timeliness of the contents of this publication.

Related Blogs of

What Is the Relationship Between ASMPT 0522.HK and HBM? The Role of Advanced Packaging Equipment in the AI Memory Supply Chain

What Is the Difference Between DRAM Contract Price and Spot Price? Which Indicator Should Investors Watch?

What Is the Difference Between HBM3E and HBM4? What Do They Mean for Micron and AI Servers?

Why Is HDD Supply and Demand Tightening? AI Data Centers, Long-Term Agreements, and Western Digital/Seagate Pricing Power

Choose Country or Region to Read Local Blog

Contact Us

BIYA GLOBAL LLC is registered with the Financial Crimes Enforcement Network (FinCEN), an agency under the U.S. Department of the Treasury, as a Money Services Business (MSB), with registration number 31000218637349, and regulated by the Financial Crimes Enforcement Network (FinCEN).

BIYA GLOBAL LIMITED is a registered Financial Service Provider (FSP) in New Zealand, with registration number FSP1007221, and is also a registered member of the Financial Services Complaints Limited (FSCL), an independent dispute resolution scheme in New Zealand.