Cross-Border Tax Refunds & Overseas Returns Payment Challenges: How to Open a Digital Master Account That Receives 30+ Fiat Wire Transfers Globally

Image Source: pexels

When handling overseas shopping tax refunds or international returns, you often face complicated receiving processes, slow arrival times, and high fees. Traditional bank accounts involve cumbersome regulatory procedures in terms of compliance, and cross-border collections are easily restricted by currency conversion and international wire transfer limitations. Digital master accounts, operated by licensed financial institutions, feature more efficient compliance systems and global collection capabilities, allowing you to easily navigate regulatory environments in different countries. You can manage multi-currency funds more conveniently, reduce transaction costs, and improve the cross-border receiving experience.

Key Points

- A digital master account simplifies the collection process for overseas shopping tax refunds and international returns while lowering transaction costs.

- Using a digital master account supports receiving wire transfers in over 30 fiat currencies worldwide, making multi-currency fund management convenient.

- Digital master accounts provide faster arrival times, typically completing wire transfers within 1-2 business days.

- Choose a compliant digital master account platform to ensure fund security and protection of personal information.

- The registration process for a digital master account is simple: provide identity proof and link a bank card to ensure compliance.

Analysis of Overseas Shopping Tax Refund Collection Challenges

Image Source: unsplash

Wire Transfer Barriers

When applying for overseas shopping tax refunds or international returns, you often need to receive funds via wire transfer. In practice, wire transfers face many obstacles. For example, the U.S. tax authority (IRS) only supports interaction with U.S. domestic bank accounts, requiring an account with a 9-digit ABA routing number. Even if you have a foreign bank account with an IBAN or SWIFT code, you cannot directly receive U.S. tax refund payments. The identity verification process is complex and prone to delays. If you fail to provide valid U.S. banking information, refunds will be frozen until verification is completed. Common barriers include:

- You need an electronic account compatible with the United States.

- Foreign bank accounts cannot be used directly for receipt.

- Identity verification may cause arrival delays.

- New IRS policies increase the complexity of electronic payments.

- When a declaration is flagged, refunds are frozen and require additional verification.

Bank Limitations

Traditional banks have obvious limitations in efficiency and cost when handling overseas shopping tax refunds and international return collections. Taking Hong Kong licensed banks as an example, cross-border wire transfer processes are constrained by national regulations, operational silos, and legacy systems. Different banks operate on their own schedules, causing payment delays. Regulatory compliance requirements are complex and processing times are long. Legacy systems restrict speed and increase costs. Language and character barriers affect information transmission, and inconsistent currency cut-off times also cause slow arrivals. Banks prioritize security, while correspondent banks charge management fees but lack incentive to simplify processes. The table below shows the main limitations:

| Barrier Type | Description |

|---|---|

| Operational Silos | Banks operate on different schedules, causing delays in cross-border payments. |

| Regulatory Compliance | Different countries have varying transaction requirements, increasing processing time and complexity. |

| Legacy Systems | Old systems limit speed and increase costs. |

| Language Barriers | Language and character restrictions cause information ambiguity and affect transaction clarity. |

| Inconsistent Currency Cut-off Times | Different systems have inconsistent currency clearing times, leading to payment delays. |

| Security Priority | Banks prioritize security over speed, resulting in delays. |

| Insufficient Incentives for Charging Banks | Correspondent banks charge management fees but lack motivation to simplify processes. |

User Pain Points

When actually handling overseas shopping tax refunds and international return collections, you will encounter multiple pain points. Integration of payment solutions and regulatory systems across different countries is complex, lacking a unified platform and resulting in low efficiency. Large one-time transfers easily cause account imbalances, requiring additional capital management. Cross-border payments are slow, lack transparency, and arrival times are difficult to predict. Multiple intermediaries lead to high fees, including foreign exchange and tax costs. Different regulatory authorities in each country impose varying requirements, making compliance extremely complex. The table below summarizes the main pain points:

| Challenge Area | Description |

|---|---|

| Integration Complexity | Difficulty integrating payment schemes and regulatory systems across countries; lack of a unified global platform results in low efficiency. |

| Liquidity Management | Large one-time transfers cause account imbalances, requiring extra capital to balance accounts. |

| Speed and Transparency | Cross-border payments are slow, lack transparency, and fund arrival times are uncertain. |

| Cost Factors | Multiple intermediaries increase fees, including foreign exchange and tax costs. |

| Regulatory Complexity | Multiple regulatory bodies in different jurisdictions have varying compliance requirements, greatly increasing complexity. |

If you want to successfully complete overseas shopping tax refund collections, you must face these barriers and pain points. Traditional banks and platforms struggle to meet the demand for efficient, low-cost, and transparent cross-border receiving. The emergence of digital master accounts provides you with a new solution.

Advantages & Features of Digital Master Accounts

Compliance & Security

When choosing a digital master account, what you care about most is compliance and fund security. Mainstream digital master accounts are operated by licensed payment companies or overseas financial institutions and strictly comply with international regulatory standards. Taking BiyaPay as an example, the platform passes multiple international certifications to ensure the security of your funds and personal information. You can refer to the table below to understand common compliance certifications for digital master accounts:

| Certification / Compliance | Description |

|---|---|

| FTC Consent Order | Conducts privacy and security program assessments, demonstrating commitment to consumer protection and compliance obligations. |

| DoD IL6 | Ensures cloud environments meet the highest security requirements for handling confidential data. |

| HITRUST Certification | Assesses organizational alignment with HITRUST requirements and supports best-practice frameworks. |

| HIPAA Compliance | Ensures compliance with HIPAA security and privacy protection measures. |

| FedRAMP® | Allows cloud service providers to meet security requirements so agencies can confidently outsource. |

| CMMC / NIST SP 800-171 | Conducts CMMC assessments to ensure compliance with security standards. |

When using a digital master account, the platform employs multiple encryption layers and tiered risk control systems to safeguard every fund transfer. Compared with traditional banks, digital master accounts differ in fund storage and insurance mechanisms. Traditional banks are usually subject to strict regulation, with user deposits insured up to $250,000 by FDIC. Some fintech companies require additional technical measures to ensure fund security. For example, BiyaPay stores user funds in protected accounts, using segregated custody and multi-factor authentication to reduce the risk of misappropriation or loss. When handling overseas shopping tax refunds or international return collections, you can obtain security equivalent to—or even higher than—mainstream banks.

Tip: When registering and using a digital master account, be sure to verify the platform’s compliance qualifications and fund custody method to protect your rights.

Multi-Currency Receiving

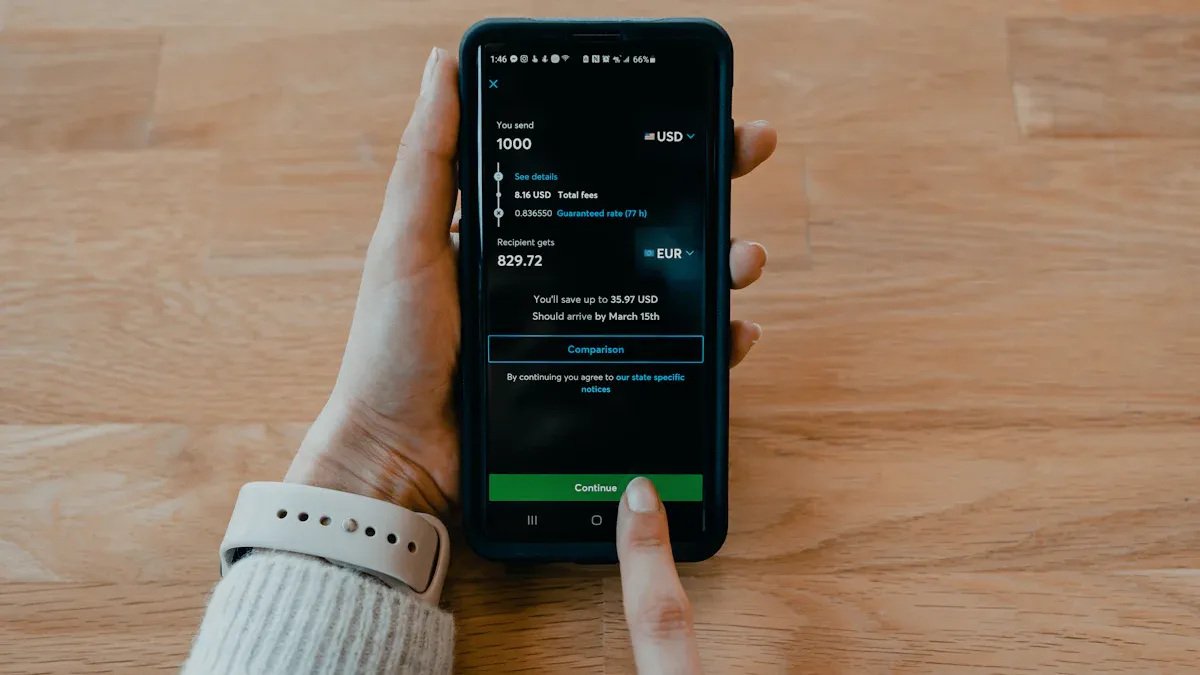

When conducting overseas shopping tax refunds or international return collections globally, you often face challenges with multi-currency arrivals and exchange rate fluctuations. Digital master accounts support receiving wire transfers in over 30 fiat currencies worldwide, covering major currencies such as USD, EUR, GBP, HKD, JPY, etc. With just one account, you can efficiently manage multi-currency funds and greatly simplify cross-border receiving processes.

- Multi-currency accounting systems can record, report, and analyze transactions in multiple currencies, helping you flexibly convert between foreign and local currencies.

- Real-time currency conversion reduces risks from exchange rate fluctuations, allowing you to lock in better rates at the time of receipt.

- You can rely on global transaction data and applicable exchange rates to improve financial management efficiency.

Taking BiyaPay as an example, the platform supports multi-currency receiving and real-time exchange. You can have wire transfers from overseas platforms or merchants sent directly to your digital master account without frequently switching banks or waiting for complicated clearing processes. When managing overseas shopping tax refund funds, you can flexibly exchange according to market conditions to minimize exchange losses.

If your use case does not end with receiving one refund, but also involves later FX conversion, fund retention, or another cross-border transfer, it becomes more important to use an account tool that keeps receiving and fund management in the same workflow. Through the BiyaPay website, you can view multi-currency fund movements in one place and use its exchange rate comparison tool to estimate the real conversion cost between fiat currencies; if the funds need to be sent onward, its remittance service can also be used directly. In practice, this makes it closer to a multi-asset trading wallet covering cross-border payments and fund management, with relevant registrations and licenses in jurisdictions such as the United States and New Zealand.

Reducing Transaction Costs

When handling cross-border collections through traditional banks, you often need to pay high handling fees and intermediary charges. Digital master accounts significantly reduce transaction costs by optimizing global payment networks. Platforms like BiyaPay use direct clearing and localized settlement to reduce intermediate steps and improve arrival speed.

- You can enjoy lower wire transfer fees; some currencies even support zero-fee incoming transfers.

- Fund arrival time is greatly shortened, usually completed within 1-2 business days—much faster than the 3-7 days of traditional banks.

- You can view arrival progress and fee details in real time, improving fund liquidity and transparency.

During overseas shopping tax refunds or international return collections, digital master accounts help you save significant time and costs. You can focus more energy on fund management and business expansion rather than cumbersome cross-border payment processes.

Digital Master Account Opening Process

Image Source: unsplash

When opening a digital master account, you can experience a far more efficient and convenient process than with traditional banks. The entire process mainly includes four steps: registration, identity verification, bank card binding, and obtaining receiving information. Each step undergoes compliance review to ensure fund security and account legitimacy. Below is a detailed breakdown of each step’s specific operations and precautions.

Registration Steps

You can register through the official website or app of mainstream digital master account platforms such as BiyaPay. The registration process is usually very simple and can be completed in minutes. You need to prepare personal identity documents and a phone capable of taking photos.

During registration, you need to fill in basic information including name, date of birth, nationality, contact information, and commonly used email. Some platforms require you to set a strong password and agree to the relevant service terms.

If you are a Chinese-speaking user, it is recommended to choose a service provider that supports a Chinese interface to reduce communication barriers and improve registration efficiency.

During registration, the platform will automatically guide you to the identity verification step to ensure account compliance.

Tip: Before registering, be sure to confirm that the selected platform holds a legitimate financial license and carefully read the user agreement to protect your rights.

Identity Verification

Identity verification is the core compliance review step for digital master accounts. You need to pass multiple verification methods to ensure account security and legitimacy. Mainstream platforms usually use video verification, database verification, and document verification in various ways, as shown in the table below:

| Identity Verification Method | Advantages | Disadvantages |

|---|---|---|

| Video Verification | Allows face-to-face interaction, enhances security, real-time document check and facial comparison. | May lead to poor customer experience, subject to technical limitations, data privacy concerns, higher cost. |

| Database Verification | Cross-checks client-provided information, supports AML and KYC compliance. | Effectiveness varies by region, may contain errors or outdated information, requires careful handling of sensitive data. |

| Document Verification | Widely used, provides high accuracy, automated processing reduces human error. | Requires regular updates for new document types, affected by image quality, cannot verify document holder identity. |

During identity verification, you usually need to upload photo-bearing documents such as ID card, passport, or residence permit, and perform facial recognition. Some platforms require video calls to verify identity authenticity.

If you are a minor, registration requires assistance from parents or guardians, along with proof of legal guardianship. Both you and the guardian need to prepare relevant documents and ensure the device supports NFC and camera functions.

The compliance team uses various technical means to conduct KYC (Know Your Customer) review, including identity verification, screening against regulatory lists, assigning risk scores, and establishing audit trails. The platform continuously monitors accounts to ensure legitimate and compliant fund flows.

Binding a Bank Card

After completing identity verification, you need to bind a bank card in your own name. You can choose to bind mainstream bank accounts in Hong Kong, the United States, Europe, etc. Binding a bank card helps with subsequent fund top-ups, withdrawals, and collections.

When binding, you need to enter the bank card number, bank name, account holder name, etc. Some platforms require you to upload a photo of the bank card or bank statements to verify account ownership.

After binding, the platform performs a small-amount verification to ensure account security. You need to complete the verification within the specified time to avoid affecting subsequent use.

You can manage bound bank cards at any time in the account backend, supporting addition, deletion, or replacement.

Note: Ensure the bound bank card information is true and valid to avoid collection failures or fund freezes due to incorrect information.

Obtaining Receiving Information

After completing registration and verification, you can obtain exclusive receiving information in the digital master account backend. You should pay attention to the following key points:

- You should find and copy the IBAN number and SWIFT BIC code in the account backend—these are key for international wire transfer receipt.

- You also need to provide the account holder name, account address, and the country where the opening bank is located.

- If receiving within the SEPA area, IBAN is usually sufficient; for international payments outside the SEPA area, both IBAN and SWIFT are required.

- You can send this information to overseas merchants, platforms, or tax authorities that need to remit funds to you, ensuring they fill it out accurately to avoid remittance failures due to missing information.

When handling overseas shopping tax refunds or international return collections, simply provide the above receiving information to the other party to successfully complete international wire transfers. Platforms like BiyaPay display arrival progress and historical records in real time in the backend, making it easy for you to query and manage multi-currency funds at any time.

Tip: Regularly check whether receiving information has changed to avoid affecting the collection process due to bank policy adjustments.

Through the above four steps, you can efficiently and securely open a digital master account to meet global receiving needs. The entire process is simple and transparent, with strict compliance reviews, greatly improving your fund management efficiency in cross-border scenarios such as overseas shopping tax refunds.

Practical Collection Guide

Providing Receiving Information

When actually handling overseas shopping tax refunds or international return collections, you first need to accurately provide the digital master account’s receiving information to overseas merchants, platforms, or tax authorities. Taking BiyaPay as an example, you can find exclusive IBAN, SWIFT BIC, account holder name, bank address, and other information in the account backend. You should copy this information completely and send it to the other party via email or platform message.

If the other party requires filling out a receiving form, ensure all fields match exactly what is displayed in the BiyaPay backend to avoid remittance failures due to inconsistencies. You can also view collection progress in real time in the BiyaPay backend and promptly confirm fund arrival.

Tip: Regularly check whether receiving information has changed, especially when international wire transfer policies are adjusted, to ensure the information remains valid.

Collection Process Demonstration

After providing the receiving information, overseas merchants or platforms will wire the funds to your digital master account via international transfer. Taking the U.S. tax authority as an example, if you apply for an overseas shopping tax refund, you need to provide receiving information that meets U.S. banking standards. BiyaPay supports wire transfers in over 30 fiat currencies worldwide, covering major currencies such as USD, EUR, HKD, etc.

You can follow these steps:

- Log in to your BiyaPay account and obtain the latest receiving information.

- Send the IBAN, SWIFT, account name, and other information to the overseas merchant or tax authority.

- After the other party completes the wire transfer, view the arrival progress in real time in the BiyaPay backend.

- Once funds arrive, you can choose to withdraw to your bound bank card or directly perform currency exchange and fund management.

Throughout the process, you do not need to frequently switch bank accounts, making fund management more efficient and transparent.

Multi-Currency Arrival Recommendations

You often encounter multi-currency arrival issues during collection. BiyaPay supports receiving in multiple currencies such as USD, EUR, HKD, and provides real-time exchange rate conversion services. You can choose the optimal exchange rate based on market conditions to convert foreign currencies into USD and reduce exchange losses.

It is recommended to monitor exchange rate fluctuations before receiving funds and arrange conversion timing reasonably. The BiyaPay backend displays real-time rates and arrival amounts to help you make decisions. You can also use the platform’s fund management tools for batch conversions or regular settlements to improve liquidity.

If you need the funds for investment or consumption in the U.S. market, it is recommended to prioritize USD receipt to minimize multiple conversion costs.

Note: Pay attention to platform handling fees and arrival times, plan fund usage reasonably, and ensure every overseas shopping tax refund arrives efficiently.

Precautions & Frequently Asked Questions

Handling Fee Explanation

When using BiyaPay and similar digital master accounts to receive international wire transfers, handling fees vary by currency. The platform clearly displays the fee for each transaction before receipt to help you plan funds reasonably. The table below shows receiving fees for some major currencies:

| Currency | Receiving Fee |

|---|---|

| USD | 6.11 USD |

| GBP | 2.16 GBP |

| EUR | 2.39 USD |

| Other 20 currencies | See platform fee details |

You can check the latest fee standards for all currencies in real time in the BiyaPay backend. Compared with traditional banks, digital master accounts usually offer more competitive rates, especially suitable for users who frequently handle overseas shopping tax refunds or international return collections.

Arrival Time

Arrival speed is one of your biggest concerns. Digital service platforms like BiyaPay can usually complete international wire transfers within 1-2 business days—much faster than the 3-5 business days of traditional banks. The table below compares arrival times and fee ranges across different channels:

| Type | Processing Time | Fee Range |

|---|---|---|

| Traditional Bank | 3-5 business days | 25-50 USD |

| Digital Service | Usually faster | More competitive |

You can track arrival progress in real time through the BiyaPay backend to improve fund management efficiency. Certain special currencies or holidays may affect arrival time; it is recommended to plan fund arrangements in advance.

Compliance & Security

When using a digital master account, fund security and compliance are critical. Platforms like BiyaPay adopt multiple security measures to protect your account:

- It is recommended to use a password manager to generate and store complex passwords to prevent password leaks.

- Enable two-factor authentication to add an extra security layer to your account.

- Regularly check and update privacy settings to prevent misuse of personal information.

- Use one-time verification codes to prevent unauthorized access.

The platform continuously monitors abnormal account behavior to ensure every fund transfer is legal and compliant. During registration and use, you should proactively verify the platform’s compliance qualifications and fund custody method to protect your rights.

Tip: When handling cross-border collections such as overseas shopping tax refunds, be sure to properly safeguard account information to avoid fund risks due to information leakage.

Reasons for Collection Failure

You may encounter failed arrivals during collection. Common reasons include:

- Incorrect receiving information, such as mismatched IBAN, SWIFT, or account name.

- The payer’s bank does not support the relevant currency or region.

- The account has not completed identity verification or compliance review.

- Fund source does not comply with platform policy, triggering risk control interception.

- Holidays or special periods cause clearing delays.

Before receiving funds, carefully verify all information and ensure the account status is normal. If you encounter abnormalities, promptly contact BiyaPay customer service or refer to the platform’s help center for professional support.

Through a digital master account, you can efficiently solve the challenges of overseas shopping tax refunds and international return collections. With the continuous growth of global trade and digital commerce, financial technology innovation is driving changes in cross-border payments. The table below shows industry trends:

| Trend | Description |

|---|---|

| Growth of Global Trade and Digital Commerce | The market grows due to increased global trade and digital commerce. |

| Consumer Expectations for Instant and Low-Cost Transactions | Consumers expect fast and low-cost transactions, driving adoption of digital master accounts. |

| Development of Fintech Solutions | Fintech innovation and development provide better payment solutions for cross-border e-commerce. |

You should focus on account security and compliance, follow the steps carefully, and avoid common issues. Choose a digital master account to enjoy a convenient and transparent global collection experience.

FAQ

How to ensure the digital master account receiving information is filled out correctly?

You need to carefully verify the IBAN, SWIFT BIC, account name, and bank address. It is recommended to directly copy the information displayed in the BiyaPay backend to avoid manual input errors. Send it to overseas merchants or tax authorities via email or platform message.

What are the common handling fees when receiving with a digital master account?

When using BiyaPay to receive international wire transfers, fees vary by currency. For example, the USD receiving fee is 6.11 USD. You can check the latest fee standards for all currencies in real time in the platform backend.

Why is there a difference in arrival time?

During receipt, arrival speed is affected by currency, payer’s bank, holidays, and clearing processes. BiyaPay usually completes wire transfers within 1-2 business days. Special circumstances may cause delays; it is recommended to plan fund arrangements in advance.

How to ensure the security of account funds?

You can enable two-factor authentication, set complex passwords, and regularly check privacy settings. BiyaPay uses multiple encryption and risk control systems, continuously monitoring abnormal account behavior to ensure safe and compliant fund flows.

What to do if collection fails?

If collection fails, check whether the receiving information was filled out correctly and confirm that identity verification has been completed. You can contact BiyaPay customer service, provide detailed transaction information, and obtain professional support and solutions.

*This article is provided for general information purposes and does not constitute legal, tax or other professional advice from BiyaPay or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or warranties, express or implied, as to the accuracy, completeness or timeliness of the contents of this publication.

Related Blogs of

How Should SSDs and HDDs Work Together in AI Data Centers? Performance, Capacity, Cost, and Hot vs. Cold Data Compared

What Are NOR Flash, SLC NAND, and EEPROM? Why They Help Explain Hong Kong-Listed Memory-Related Stocks

Why Is HDD Supply and Demand Tightening? AI Data Centers, Long-Term Agreements, and Western Digital/Seagate Pricing Power

How Do AI Servers Drive Storage Demand? The Roles of HBM, Server DRAM, Enterprise SSDs, and HDDs

Choose Country or Region to Read Local Blog

Contact Us

BIYA GLOBAL LLC is registered with the Financial Crimes Enforcement Network (FinCEN), an agency under the U.S. Department of the Treasury, as a Money Services Business (MSB), with registration number 31000218637349, and regulated by the Financial Crimes Enforcement Network (FinCEN).

BIYA GLOBAL LIMITED is a registered Financial Service Provider (FSP) in New Zealand, with registration number FSP1007221, and is also a registered member of the Financial Services Complaints Limited (FSCL), an independent dispute resolution scheme in New Zealand.