Sports Betting Legalization Dividend: Is Now the Time to Enter DraftKings (DKNG) Stock?

Image Source: unsplash

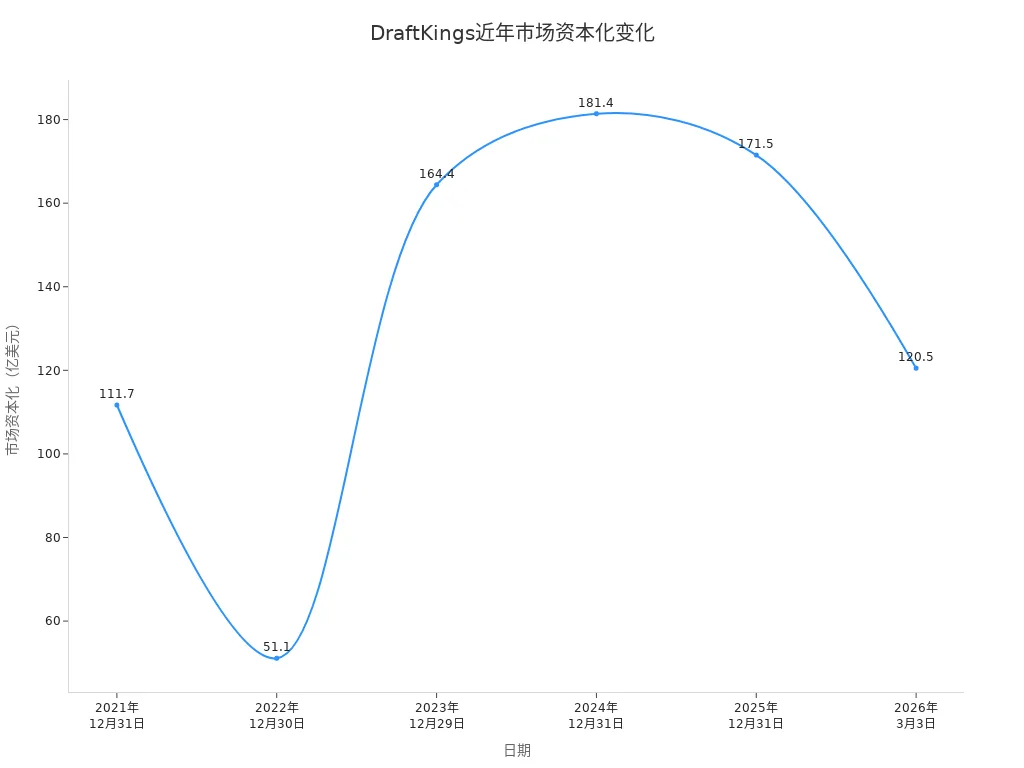

DraftKings’ current investment appeal has significantly increased. The sports betting legalization dividend has not yet been fully digested by the market, while new market openings in Missouri and legislative progress in California bring fresh growth drivers for the company. The Super App strategy continues to advance, strengthening user stickiness. The recent notable pullback in market cap provides investors with a more attractive entry timing.

Key Takeaways

- Sports betting legalization brings new market opportunities to DraftKings, with more than 35 states having chosen to legalize it, continuously expanding the user base and revenue sources.

- Legislative progress in Missouri and California will drive DraftKings’ market growth, with Missouri’s market size (GGR) expected to reach $500 million.

- DraftKings’ Super App strategy enhances user stickiness through personalized services and social features, improving user engagement and retention rates.

- The company achieved significant revenue growth in 2024 and recorded positive GAAP net income for the first time, demonstrating improved profitability.

- Despite facing competition and regulatory risks, DraftKings’ long-term growth potential remains strong, and investors should pay attention to market catalysts.

Sports Betting Legalization Dividend and Market Catalysts

Image Source: pexels

Opportunities from New Market Openings

The sports betting legalization dividend continues to be released, bringing significant growth momentum to leading platforms like DraftKings. As of 2024, more than 35 states in the United States have chosen to legalize or expand sports betting options. The continuous opening of new markets means DraftKings can steadily expand its user base and revenue sources.

| Number of States | Description |

|---|---|

| 35+ | More than 35 states have chosen to legalize or expand sports betting options. |

The opening of new markets not only increases the number of users but also drives the overall industry scale expansion. Taking Missouri as an example, the expected market size (GGR) can reach $500 million. As the most populous state, California holds even greater market potential if legalization is achieved. With its first-mover advantage and technological accumulation, DraftKings is poised to quickly secure a leading position in new markets.

For Chinese-speaking users, choosing payment platforms like Biyapay that support multiple currencies and convenient deposits can better meet the funding needs of cross-border sports betting and enhance the overall experience.

Latest Developments in Missouri and California

Legislative progress in Missouri and California has become a key catalyst for the 2024 sports betting legalization dividend. In November 2024, Missouri voters passed Amendment 2 to legalize sports betting with a narrow 50.1% majority. The amendment is expected to take effect on December 5, with the gaming commission completing rulemaking and approvals in early 2025, and sports betting operations officially launching in March 2025, coinciding with the NCAA March Madness events.

Missouri’s total handle in the first month has already exceeded $543 million, though actual tax revenue was only $521,000 after promotional deductions; as the market matures, tax revenue is expected to rise to $28.9 million.

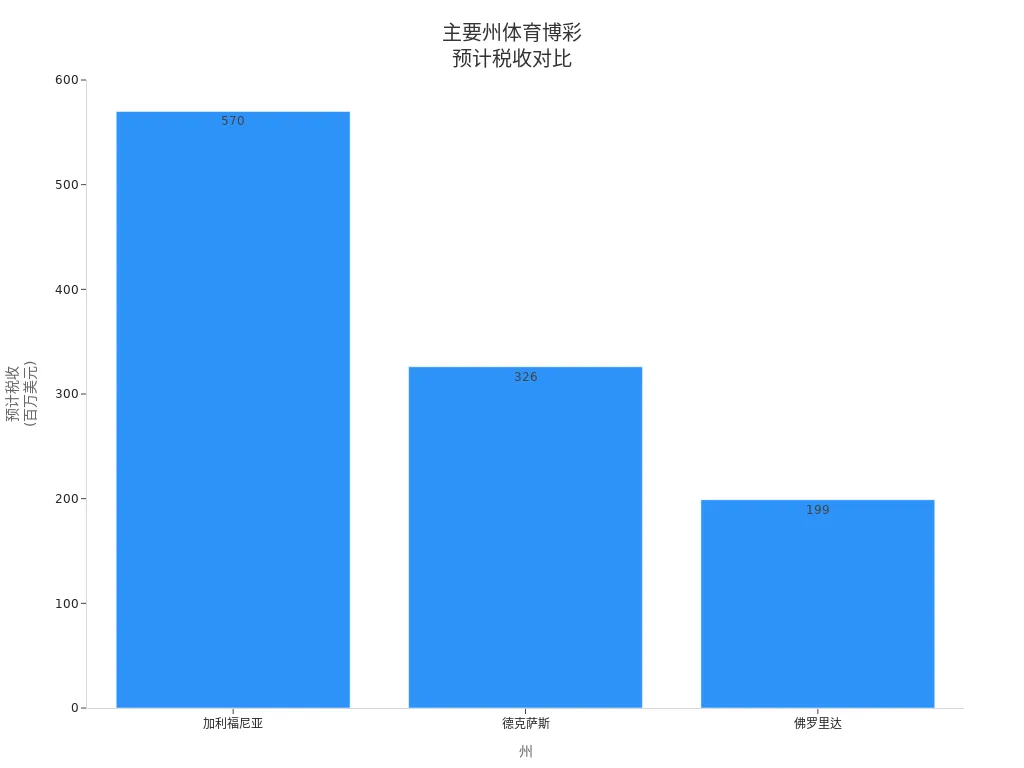

As the most populous state in the U.S., California’s economic impact from sports betting legalization would be extremely significant, with an estimated annual tax revenue of up to $570 million for the state government.

| State | Expected Tax Revenue (million USD) |

|---|---|

| California | 570 |

| Texas | 326 |

| Florida | 199 |

The legislative progress in Missouri and California not only brings new market space to DraftKings but also further reinforces the sustainability of the sports betting legalization dividend.

Super App Strategic Layout

DraftKings is actively advancing its Super App strategy, aiming to build a comprehensive entertainment platform integrating sports betting, online casino, daily fantasy sports, and other diversified services. This strategy leverages data infrastructure and artificial intelligence technology to deliver personalized promotions and precise recommendations, significantly enhancing user engagement and retention rates.

| Evidence Point | Description |

|---|---|

| Personalized Promotions | DraftKings utilizes data infrastructure and AI to provide highly personalized user experiences, improving participation and retention rates. |

| Loyalty Program | The DraftKings Dynasty Rewards program enhances retention by rewarding high-value players. |

| Social Features | Social features are seen as a key pillar in driving user engagement, promoting interactions among users. |

The Super App strategy not only increases platform user stickiness but also enhances user lifetime value. For Chinese users, choosing platforms like Biyapay that support multilingual interfaces, cross-border payments, and localized services can better meet diverse needs and improve the overall experience. Through continuous optimization of product structure and service system, DraftKings has further solidified its leading position in the industry.

The sports betting legalization dividend, the opening of new markets in Missouri and California, and the synergistic effect of the Super App strategy collectively propel DraftKings toward broader growth space.

DraftKings Fundamental Analysis

Latest Performance Results

DraftKings delivered impressive results in 2024. The company’s latest quarterly revenue approached $2 billion, up 43% year-over-year. Management achieved positive GAAP net income for the first time, marking a qualitative leap in profitability. The table below shows DraftKings’ latest financial performance:

| Metric | Value |

|---|---|

| Revenue | Approaching $2 billion, with 43% annual growth |

| Net Income | Achieved positive GAAP net income for the first time |

The simultaneous improvement in revenue and net profit reflects DraftKings’ effective execution in new market expansion and product innovation. By optimizing operational efficiency and enhancing user value, the company successfully balanced scale expansion with profitability.

User Growth and Market Share

DraftKings continues to expand its user base and consolidate its leading position in the U.S. sports betting market. According to industry data, DraftKings holds a 34% share of the U.S. online sports betting market. This market share ranks only behind the industry leader, demonstrating the company’s strong brand influence and user appeal.

| Company | Market Share |

|---|---|

| DraftKings | 34% |

DraftKings continuously improves user activity through diversified product layouts and precise marketing strategies. For Chinese-speaking users, choosing payment platforms like Biyapay that support multiple currencies and convenient deposits helps lower funding circulation barriers and enhance the overall experience. DraftKings’ rapid penetration capability in new markets lays a solid foundation for subsequent growth.

Profitability and Balance Sheet

DraftKings’ profitability continues to improve. In 2023, the company’s adjusted earnings were -$151 million; in 2024, it achieved $181.3 million in profit, completing a key turnaround from loss to profit. The table below shows the profitability changes over the past two years:

| Year | Adjusted Earnings (million USD) | Profit Change |

|---|---|---|

| 2023 | -151 | Loss |

| 2024 | 181.3 | Profit |

The company’s balance sheet structure is healthy, with ample cash flow, providing strong support for subsequent market expansion and product innovation. Management continues to optimize cost structure and improve operating leverage, ensuring financial soundness amid fierce competition. The improvement in profitability and balance sheet optimization further boosts investor confidence.

Industry Growth Space and Competitive Landscape

U.S. Sports Betting Market Outlook

The U.S. sports betting market demonstrates strong growth momentum. Multiple research institutions predict that the U.S. sports betting market will grow at an annual rate of approximately 12% over the next five years. By 2030, the total gross gaming revenue (GGR) is expected to reach $33.3 billion, far exceeding the $12.6 billion in 2024.

- Expected compound annual growth rate of approximately 12%

- Market size expected to reach $33.3 billion by 2030

The U.S. market maintains a leading position globally. Although the Latin American market is growing faster and is expected to reach $54 billion by 2026, the U.S. market still possesses long-term expansion potential thanks to gradual policy liberalization and the sports betting legalization dividend.

| Market | 2024 Total Revenue (GGR) | Projected 2026 Market Size | Growth Rate |

|---|---|---|---|

| United States | $12.7 billion | N/A | N/A |

| Latin America | N/A | $54 billion | 150% (from 2023) |

Industry Competition and DraftKings’ Position

The U.S. sports betting industry is highly competitive. Major players include FanDuel, Barstool Sportsbook, Bet365, PointsBet, William Hill, FoxBet, and BetMGM. DraftKings occupies a leading position in the market thanks to its strong brand recognition and technology investments. Through the acquisition of SB Technology, the company gained independent R&D capabilities, enabling rapid launch of new products based on customer data.

DraftKings holds clear advantages in the North American sports betting and iGaming markets, particularly excelling in the daily fantasy sports sector. The company’s financial condition is solid, with the capacity for sustained investment in market and brand building.

Marketing and customer acquisition strategies have driven DraftKings’ short-term performance growth, but the industry generally faces challenges of promotional dependency and insufficient customer loyalty. Some competitors like BetMGM aggressively promote to seize market share, and the industry landscape continues to evolve dynamically. With the sports betting legalization dividend continuing to be released, leading companies are expected to consolidate their leading positions in the new round of expansion.

Valuation and Market Expectations

Current Valuation Level

DraftKings’ current valuation shows certain volatility. The company’s latest price-to-earnings (P/E) ratio is -47.77, reflecting that profitability is still in a transition phase. The negative P/E is mainly due to past years’ losses, but as profitability improves, future valuation is expected to return to a reasonable range. The PEG ratio is 0.46, indicating high growth potential. The Beta value is 1.67, suggesting relatively large stock price fluctuations, so investors need to monitor market risks.

If your focus with this kind of high-volatility growth stock is ongoing tracking efficiency, it may also be practical to use BiyaPay’s stock information page to check the ticker, basic market data, and related company details without switching across multiple sites. For users who also need to coordinate cross-border fund management with portfolio allocation, the broader service path on the BiyaPay official website may also be relevant. BiyaPay is positioned as a multi-asset wallet covering cross-border remittance, U.S. and Hong Kong stock trading, and digital-asset spot and contract scenarios, so the mention here works best as a supporting tool for investment lookup and account management rather than a substitute for the investment case on DraftKings itself.

The table below summarizes DraftKings’ main valuation metrics:

| Metric | Value |

|---|---|

| P/E Ratio | -47.77 |

| PEG Ratio | 0.46 |

| Beta | 1.67 |

Recently, DraftKings’ stock price fell about 8% due to NFL playoff results, significantly below the 52-week high of USD 53.61. The company has authorized a USD 2.0 billion stock repurchase program to enhance earnings per share. There is currently a disconnect between the valuation level and long-term growth potential, so investors need to make comprehensive judgments in combination with market catalysts.

Analyst Target Prices and Market Consensus Expectations

Market analysts are generally optimistic about DraftKings’ future performance. The average target price is USD 47.10, offering about 46% upside from the current price. Morgan Stanley raised its 2026 target price to USD 53, emphasizing the company’s cash flow potential. Ratings from multiple institutions are as follows:

| Source | Target Price | Consensus Rating |

|---|---|---|

| TradingView | USD 57.57 | Strong Buy |

| MarketBeat | USD 46.10 | Moderate Buy |

| Public.com | N/A | Buy |

Analysts unanimously believe DraftKings has shown significant growth in online sports betting, with annual growth reaching 10% and accelerating to 17% in October. Fourth-quarter 2024 revenue is expected to reach USD 2.043 billion, with EBITDA forecast at USD 300 million. The company holds an 80% share of monthly active users, with substantial expansion opportunities and gross margin improvement potential. Although the 2025 EBITDA expectation was lowered to USD 450–550 million due to rising marketing expenses and underperforming sports events, the market consensus expects DraftKings to maintain strong long-term growth potential.

Major Risk Factors

Intensified Competition and Regulatory Changes

DraftKings continues to expand in the U.S. sports betting market, but the constantly changing regulatory environment and competitive landscape bring risks that cannot be ignored. On the regulatory side, policy adjustments may directly affect DraftKings’ business compliance and market access:

- The CFTC plans to establish clear rules for prediction markets, which may reshape the industry competitive landscape.

- Withdrawal of the proposal to prohibit sports and politics-related contracts may introduce new competitors like Robinhood, increasing market pressure.

- The Massachusetts ruling requiring Kalshi to suspend sports contracts in the state highlights local regulatory uncertainty, increasing DraftKings’ operational risks.

In terms of industry competition, although DraftKings has increased market share and profitability through innovative customer acquisition strategies and risk management tools, intense competition from new entrants and existing rivals may still compress profit margins. The company needs to continuously invest in product innovation and marketing to consolidate its leading position.

Customer Acquisition Costs and Profit Realization

Customer acquisition costs and profit realization capabilities directly affect DraftKings’ long-term growth. Data shows that in 2024, the company added 3.5 million customers, bringing the total user count to 10.1 million, with customer acquisition costs declining 26% year-over-year. Revenue growth was strong, with first-quarter 2024 revenue up 53% year-over-year and structural sports betting hold rate reaching 9.8%. Monthly user growth was 37%, and earnings per share loss improved from 87 cents to 30 cents, reflecting continuous profitability improvement.

| Key Metric | Data |

|---|---|

| Customer Growth | 3.5 million added in 2024, reaching 10.1 million |

| Customer Acquisition Cost Decline | 26% decline in 2024 |

| Revenue Growth | 53% year-over-year in Q1 2024 |

| Monthly User Growth | 37% growth in 2024 |

| EPS Loss Improvement | From 87 cents to 30 cents |

Nevertheless, the industry’s high reliance on promotions and fluctuating user loyalty create uncertainty in acquisition costs and profit realization. DraftKings must continue optimizing operational efficiency and enhancing user lifetime value to achieve sustainable profitability amid fierce competition and regulatory changes.

Investment Returns and Risk Trade-off

Image Source: unsplash

Investment Advantages

DraftKings demonstrates multiple investment advantages. The company continues to invest in product innovation; in the first quarter of 2025, more than 50% of total bets came from live/in-play betting. The integration of SimpleBet and Sports IQ acquisitions greatly enhanced the live betting experience, driving user activity and platform stickiness. DraftKings excels in customer acquisition and retention, with effective user growth strategies, optimized marketing costs, and continuously expanding brand influence.

In terms of market share, DraftKings firmly ranks among the industry leaders, ahead of major competitors. The table below compares market shares of major sports betting platforms:

| Competitor | Market Share |

|---|---|

| DraftKings | >30% |

| FanDuel | 20%-25% |

| Caesars | Medium |

| BetRivers | Medium |

| Golden Nugget | Medium |

Through technological innovation and data-driven operational strategies, DraftKings has consolidated its leading position in the U.S. sports betting market. For Chinese-speaking users, choosing payment platforms like Biyapay that support multiple currencies and convenient deposits helps improve capital circulation efficiency, meet diverse needs, and further enhance the overall investment experience.

Main Disadvantages and Suitable Investor Profile

DraftKings’ investment also has certain disadvantages. Although profitability has improved, it remains affected by ongoing investments and market expansion in the short term, leading to large profit fluctuations. The industry faces fierce competition and frequent regulatory policy changes, which may create uncertainty for company performance. Although customer acquisition costs have declined, high promotional dependency and the need for further improvement in user loyalty remain challenges.

DraftKings is more suitable for investors with longer investment horizons who can tolerate higher volatility. Investors should focus on the company’s continuous innovation capabilities and market risks, allocate assets rationally, and avoid emotional impacts from short-term performance fluctuations. For investors seeking stable returns with lower risk tolerance, DraftKings may not be the best choice.

DraftKings currently offers high investment value. The sports betting legalization dividend has not yet been fully reflected in the stock price. Company fundamentals continue to improve, and the industry growth space is vast. Although valuation shows fluctuations, long-term potential stands out. Investors should focus on the following key variables:

| Key Variable | Description |

|---|---|

| Average Revenue Per User | Reflects user engagement and monetization capabilities |

| Regulatory Transparency | Affects market access and competitive landscape |

| Returns from New Products and Locations | Core drivers for company valuation re-rating |

Continuously tracking these variables helps capture DraftKings’ future performance.

FAQ

What are DraftKings’ main revenue sources?

DraftKings primarily generates revenue from sports betting, online casino, and daily fantasy sports businesses. The company collects betting commissions and service fees through its technology platform and continuously optimizes product structure to improve overall revenue levels.

What impact does sports betting legalization have on DraftKings?

Sports betting legalization significantly expands DraftKings’ market space. After new states open up, the company can quickly enter and acquire new users, enhancing market share and revenue growth speed.

How does DraftKings respond to industry competition?

DraftKings continues to increase investment in technology R&D and optimize user experience. Through data-driven marketing strategies and product innovation, the company enhances user stickiness and consolidates its leading market position.

Is the current valuation reasonable?

DraftKings’ current valuation reflects market expectations for its growth potential. After profitability improves, valuation is expected to gradually return to a reasonable range. Investors need to make comprehensive judgments combining industry catalysts and company fundamentals.

What are the main risks of investing in DraftKings?

The main risks include changes in industry regulatory policies, intensified competition, and fluctuations in customer acquisition costs. The company needs to continuously optimize operational efficiency and enhance profitability to address external challenges.

*This article is provided for general information purposes and does not constitute legal, tax or other professional advice from BiyaPay or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or warranties, express or implied, as to the accuracy, completeness or timeliness of the contents of this publication.

Related Blogs of

Why Is Enterprise SSD Supply Tightening? NAND Capacity Allocation, Cloud Orders, and the Pricing Cycle

Pure Storage PSTG vs NetApp NTAP: Which Enterprise Storage Brand Has Greater AI Growth Elasticity?

How Should You Evaluate Pure Storage’s Storage-as-a-Service Model? Revenue Quality and Key Risks

How to Distinguish A-Share and Hong Kong Stock Memory-Related Companies? H-Shares, A-Shares, and Business Classification Explained

Choose Country or Region to Read Local Blog

Contact Us

BIYA GLOBAL LLC is registered with the Financial Crimes Enforcement Network (FinCEN), an agency under the U.S. Department of the Treasury, as a Money Services Business (MSB), with registration number 31000218637349, and regulated by the Financial Crimes Enforcement Network (FinCEN).

BIYA GLOBAL LIMITED is a registered Financial Service Provider (FSP) in New Zealand, with registration number FSP1007221, and is also a registered member of the Financial Services Complaints Limited (FSCL), an independent dispute resolution scheme in New Zealand.