- More

- Download

BiyaPay

Published on Updated on

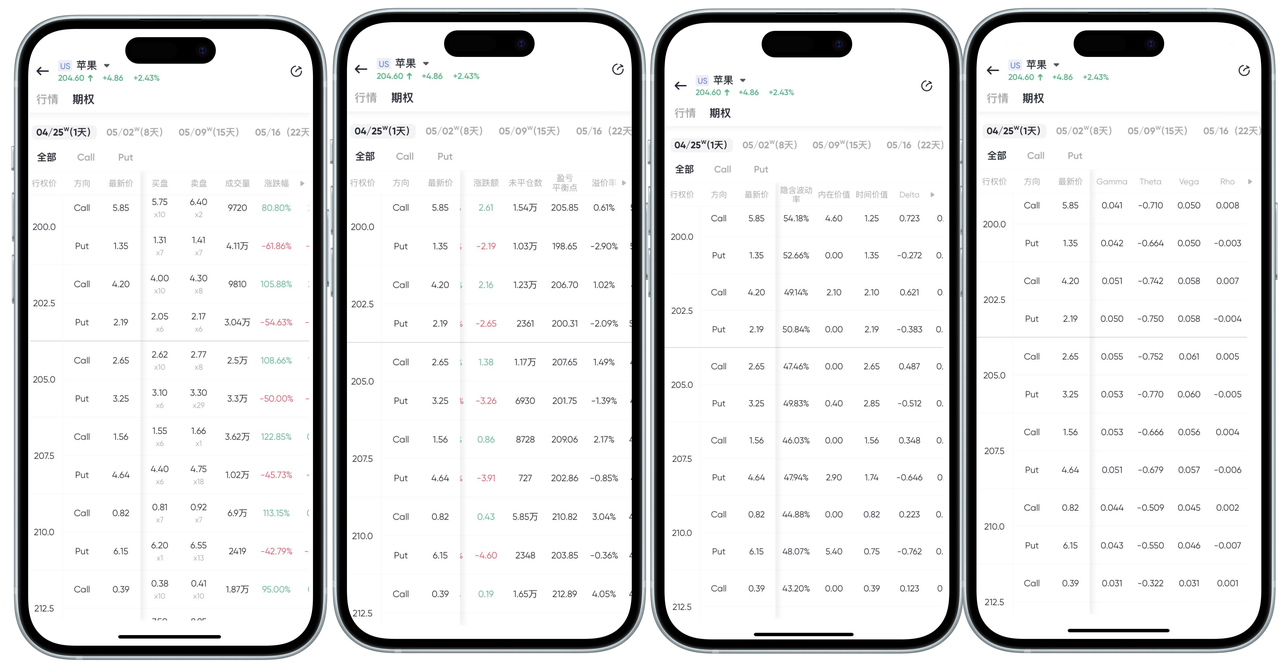

如何在 App 端查看期权链页面及其关键概念:

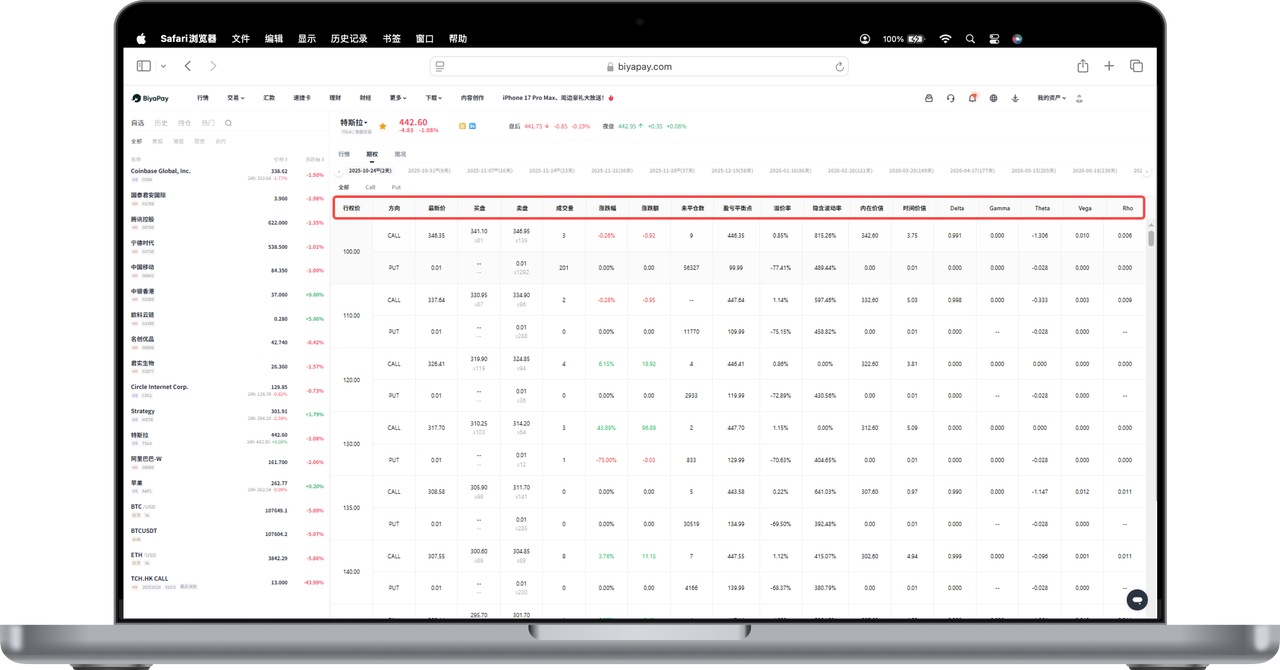

如何在 Web 端查看期权链页面及其关键概念:

以下为期权交易页面中各项数据的通俗说明,帮助您快速读懂期权报价表格,理解期权价格的构成及波动原理。

- 期权类型(Option Type)

Call(看涨期权):购买者有权在未来某时间,以固定价格买入标的资产。适用于看涨行情。

Put(看跌期权):购买者有权在未来某时间,以固定价格卖出标的资产。适用于看跌行情。

- 行权价格(Strike Price)

行权价格是期权约定未来买入或卖出标的资产的价格。例如:

200.0 表示以每股 200.0 美元行使权利。

212.5 表示以每股 212.5 美元行使权利。

- 最新价(Latest Price)

当前市场中该期权的交易价格。例如:

200.0 Call 的最新价为 5.85 美元,即买一张该期权需支付 5.85 美元。

- 买盘(Bid)与卖盘(Ask)

买盘(Bid):市场上买方愿意出的最高价格。如:

200.0 Call 的买盘价为 5.75 美元,数量 x10,表示有 10 手买单等待成交。

卖盘(Ask):市场上卖方愿意接受的最低价格。如:

卖盘价为 6.40 美元,数量 x7,表示有 7 手卖单挂出。

- 成交量(Volume) 当日已成交的期权合约总数,反映市场活跃度。例如:

- 成交量为 9720,表示已成交 9720 手(即 972,000 股)。

- 涨跌幅(Change %) 该期权价格相较于前一交易日的涨跌比例。例如:

- 涨跌幅为 +80.80%,表示价格大幅上涨。

- 隐含波动率(Implied Volatility, IV) 市场预期未来股价波动幅度。值越高,代表预期波动越大。例如:

- 200.0 Call 的隐含波动率为 54.61%,属于波动较大的期权。

- 内在价值(Intrinsic Value) 如果期权立即行使,理论上能赚多少钱。例如:

- 当前股价为 204.60 美元,200.0 Call 的内在价值为 4.60 美元(204.60 - 200.0)。

- 时间价值(Time Value) 期权的总价 - 内在价值。反映市场对未来波动的期待。例如:

- 如果总价是 5.85,内在价值为 4.60,则时间价值为 1.25。

- Delta(Δ) 标的价格每变动 1 美元,期权价格的理论变动值。例如:

- Delta = 0.723,表示股价每涨 1 美元,期权涨 0.723 美元。

- Gamma(Γ) Delta 的变化率,表示 Delta 对股价变动的敏感程度。例如:

- Gamma = 0.041,说明每涨 1 美元,Delta 增加 0.041。

- Theta(Θ) 每天时间流逝导致期权价值变化(通常为负)。例如:

- Theta = -0.710,表示每过一天,期权价格减少 0.71 美元。

- Vega(ν) 隐含波动率每变化 1%,期权价格的变化量。例如:

- Vega = 0.050,意味着 IV 上涨 1%,期权涨 0.05 美元。

- Rho(ρ) 利率变化对期权价格的影响。例如:

- Rho = 0.008,表示利率上升 1%,期权涨 0.008 美元。

期权链页面为您提供了每一组行权价下的 Call 和 Put 的报价信息、交易活跃度、波动率以及风险敏感指标,通过这些数据,您可以更科学地:

- 评估期权的“性价比”(内在+时间价值)

- 判断市场预期(隐含波动率、成交量)

- 控制风险与策略搭配(Delta、Theta、Gamma等)

BiyaPay makes crypto more popular!

Contact Us

Mail: service@biyapay.com

Customer Service Telegram: https://t.me/biyapay001

Telegram Community: https://t.me/biyapay_ch

Digital Asset Community: https://t.me/BiyaPay666

Community

Compliance Entity

Biya Global LLC is a U.S. limited liability company. It has completed federal MSB registration (Registration number 31000218637349) with FinCEN under the Bank Secrecy Act and is subject to FinCEN’s supervision.

Biya Global Limited is a New Zealand registered entity. It holds valid FSP registration (Registration number FSP1007221) on the Financial Service Providers Register (FSPR) under the Financial Service Providers (Registration and Dispute Resolution) Act 2008 and is subject to supervision by the Financial Markets Authority (FMA).

©2019 - 2026 BIYA GLOBAL LIMITED