- Remittance

- Exchange Rate

- Stock

- Events

- EasyCard

- More

- Download

Behind Qualcomm's Lucrative Earnings: How the Automotive and AI Sectors Will Drive Future Stock Pric

Published on 2024-11-20 Updated on

2024-11-20

Qualcomm (QCOM) recently released its financial report for the fourth quarter of fiscal year 2024, which was full of highlights. Its revenue reached $10.2 billion, a year-on-year increase of 18%, and earnings per share grew by 35%. Behind these figures, Qualcomm is not simply relying on its traditional mobile chip business. Instead, through a diversification strategy, it has extended its growth engines to emerging fields such as automotive, AI, and the Internet of Things. The outstanding performance in these areas is opening a fast lane to the future for Qualcomm.

However, what investors need to focus on is not just the growth figures. Currently, Qualcomm’s price-to-earnings ratio is 14.3 times, significantly lower than the industry average. With such an attractive valuation, combined with the future potential of the automotive and AI sectors, does it indicate that Qualcomm’s stock price will usher in a new round of surges?

The Secrets in Qualcomm’s Financial Report

Qualcomm’s financial performance in the fourth quarter of fiscal year 2024 can be described as a “highlight moment”. This company, once famous for its mobile chips, is now advancing into new fields such as the automotive and Internet of Things through a diversification strategy, and the results of this strategy are clearly visible in the financial data.

Core Financial Data: Steady Growth

Let’s first talk about the most crucial aspect - the financial data. In this quarter, Qualcomm’s total revenue reached $10.2 billion, with a year-on-year increase of 18%. Among them, the Chipset (QCT) business remained the “main force”, contributing $8.7 billion with a growth rate of 17.7%. Such a growth rate is not just about “maintaining”, but rather a strong expansion.

Earnings per share also showed no weakness, growing by 35% year-on-year, fully demonstrating Qualcomm’s profitability. The Licensing Business (QTL) also did not disappoint, contributing $1.5 billion with a year-on-year increase of 21%. More importantly, its earnings before interest and taxes (EBIT) margin was as high as 74%.

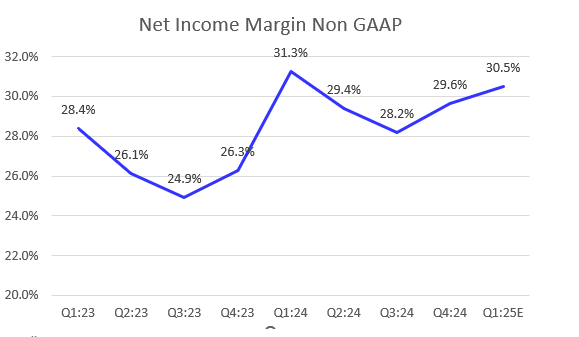

It can be seen from the chart that Qualcomm’s non-GAAP net profit margin has experienced some fluctuations in the past few quarters. However, it rebounded to 29.6% in Q4 and is expected to further rise to 30.5% in the first quarter of fiscal year 2025. This improvement in profitability is attributed to the stable expansion of its diversified businesses and the success in cost control. Whether in terms of revenue growth or profit margin performance, Qualcomm has demonstrated strong operational capabilities.

Just think about it, this is not “gross profit”, but the pure profit margin before interest and taxes! Thanks to its powerful 5G intellectual property portfolio, this part of the business has become a “cash cow” in Qualcomm’s earnings.

Strong Performance in Emerging Markets

Let’s first look at the automotive business, which is like the “Fast & Furious” in Qualcomm’s financial report.

In this quarter, the automotive revenue hit a record high of $899 million, with a year-on-year increase of 68%. You might ask, “Where does this growth come from?” It is mainly contributed by digital cockpits and Advanced Driver Assistance Systems (ADAS). Qualcomm’s Snapdragon Ride Elite platform has joined hands with well-known brands such as Mercedes-Benz and Li Auto, and has successfully “taken a seat” in the brains of luxury and new energy vehicles. Through such cooperation, Qualcomm has further consolidated its position in the automotive chip market.

Looking at the Internet of Things business, its performance is also quite eye-catching. Its revenue increased by 24% month-on-month. The management clearly pointed out that this benefited from the release of new products and the normalization of channel inventory. What’s more interesting is that Qualcomm’s Internet of Things business is no longer limited to “smart homes”, but has also entered the fields of industrial robots and edge computing. The popularization of the Snapdragon platform in these new fields has directly expanded Qualcomm’s coverage in the Internet of Things market. This is not only a game of technology, but also a battle for market occupation, and Qualcomm has obviously gained the upper hand.

You might be curious: “With Qualcomm growing so fast, are its costs also ‘running’?” The answer is no. While achieving growth in revenue and profitability, Qualcomm has successfully maintained the stability of its operating expenses. This cost control ability not only illustrates the high efficiency of Qualcomm’s internal management but also proves its strong execution ability in a complex market environment.

For investors, this stable operating model sends a clear signal: Qualcomm’s growth is not a flash in the pan but is based on strict financial discipline and resource allocation. The dual strategy of controlling costs and expanding profits has provided a solid “foundation” for Qualcomm’s stock price.

The financial data clearly shows that Qualcomm’s dual layout in traditional businesses and emerging fields has begun to bear fruit. For investors, these highlights in the financial report are a clear signal. Qualcomm has achieved steady expansion through a diversification strategy and has gained a firm foothold in multiple high-growth markets.

This multi-faceted layout not only provides strong support for the current stock price but also lays the groundwork for future stock price increases.

Automotive and AI: Qualcomm’s Next Profit Growth Points?

When it comes to Qualcomm’s automotive and Artificial Intelligence (AI) businesses, you might think, “Isn’t this company always synonymous with mobile chips?” Indeed, in the past, Qualcomm’s strength has always been in mobile devices. But now, it is turning its attention to the larger “profit prospects” of the automotive and AI sectors.

Simply put, mobile chips are just the starting point, and automotive and AI are the keys to Qualcomm’s new revenue curve.

Automotive Market: The “Accelerator” for Growth

Let’s first look at the automotive market, which can be regarded as a highlight moment in Qualcomm’s financial report. In the fourth quarter of fiscal year 2024, Qualcomm’s automotive revenue reached $899 million, a year-on-year increase of 68%, directly breaking the historical record. Doesn’t this growth rate feel like Tesla accelerating? Don’t think it’s just good luck. Behind this is Qualcomm’s in-depth cultivation in the automotive industry.

For example, Qualcomm’s Snapdragon Ride Elite platform, designed specifically for Advanced Driver Assistance Systems (ADAS) and digital cockpits, has become the first choice for first-tier automotive brands. Whether it’s a luxury brand like Mercedes-Benz or a new energy rising star like Li Auto, the Snapdragon platform has played the role of an “intelligent brain”. Don’t underestimate this platform. It not only makes cars “smarter” but also increases Qualcomm’s revenue share in the automotive chip field from 8.2% to 9.6%, achieving record growth for five consecutive quarters.

Looking to the future, the management is full of confidence in the automotive business and expects that the automotive revenue can still increase by 50% in the near future. This is not just about numbers but also the continuous demand for intelligent upgrades in the automotive industry, which is constantly opening up new opportunities for Qualcomm.

AI Technology: The Core Driving Force in the Market Wave

Now let’s talk about AI. You might think that the competition in the AI field is so fierce now. Why can Qualcomm stand out? The answer lies in its Snapdragon platform. This platform is not only powerful but also particularly “intelligent”. For example, the latest Snapdragon 8 Elite platform is equipped with the second-generation Oryon CPU, with a 30% performance improvement, a 57% power consumption reduction, and a 45% direct improvement in AI performance.

Such hard power has also attracted many “luxury teammates”. For example, Qualcomm has cooperated with Meta to support the Llama 3.2 model on Snapdragon devices and has also joined hands with Amazon to launch the AI Hub to meet the computing needs from the cloud to the edge. It is worth mentioning that these cooperations directly drove the related revenue to increase by more than 50% month-on-month in the fourth quarter, opening up a broader territory for Qualcomm in the AI market.

More importantly, Qualcomm’s Hexagon NPU can handle AI tasks locally on devices. This is particularly important for scenarios that require real-time responses, such as industrial robots and intelligent monitoring systems. In simple terms, Qualcomm is not aiming to do “AI in the cloud” but to achieve a more efficient and intelligent experience on the devices at your fingertips.

The booming of the automotive and AI markets is not a flash in the pan but a microcosm of the global technological trend. It is estimated that by 2029, the global automotive AI market size will reach $8 billion, with a compound annual growth rate of over 37%. Qualcomm’s “first-mover” layout in these two fields has already enabled it to occupy an advantageous position in the competition.

Meanwhile, the edge computing applications of AI are also expanding rapidly. It is estimated that by 2025, the edge computing market size will exceed $50 billion, and the Snapdragon platform is an important driver in this market. The management expects that in the next three years, AI and edge computing will contribute more than 15% of Qualcomm’s total revenue, further optimizing the revenue structure.

After reading this, some people might think: These all seem very impressive, but what does it mean for the stock price? In fact, the answer is simple: The rapid rise of the automotive and AI sectors is redefining Qualcomm’s revenue sources. And the continuous growth of the Snapdragon platform and the automotive business has already formed a new “dual-wheel drive” model. For investors, this is not only a new growth story but also the foundation of Qualcomm’s stock price potential.

So, currently, Qualcomm not only has solid financial report data but also has clear goals for the future. Isn’t this “steady progress” state exactly what many people consider as a “high-quality investment target”?

Future Market Environment and Qualcomm’s Growth Potential

The popularization of 5G is paving a broad road for Qualcomm’s continuous profitability. In the fourth quarter of fiscal year 2024, Qualcomm’s licensing business revenue increased by 21% year-on-year, with a profit margin as high as 74%, fully demonstrating the advantages of its 5G patent portfolio. In the next five years, the global 5G network penetration rate is expected to increase from the current 42% to over 70%, and the appearance of each new device will further consolidate Qualcomm’s position in this field.

At the same time, intelligent vehicles have become an important growth engine for Qualcomm. The global automotive market is accelerating its transformation from traditional models to intelligent and connected ones. It is estimated that by 2029, the automotive AI market size will reach $8 billion, with a compound annual growth rate of over 37%. In this field, Qualcomm has not only seized the opportunity with technology, but its Snapdragon Ride platform is also widely used in major automotive brands, successfully expanding the revenue space. In 2024, the automotive business revenue increased by 68% year-on-year, setting a new record of $899 million.

AI and edge computing are another high ground. The Snapdragon 8 Elite platform, with a 45% improvement in AI performance and a 57% reduction in power consumption, has enabled Qualcomm to occupy a leading position in the fields of mobile devices and industrial Internet of Things. By 2025, the edge computing market size is expected to exceed $50 billion. Qualcomm is using Hexagon NPU and AI Hub technologies to expand into scenarios such as smart homes and industrial robots.

Qualcomm’s Future Path: From Diversification to Risk Resistance

Qualcomm’s diversification strategy is not only to expand revenue sources but also to resist the risks of market fluctuations. Although the global mobile phone market has slowed down in recent years, Qualcomm has effectively balanced the fluctuations in overall revenue through the growth of its automotive, Internet of Things, and AI businesses. Such a revenue structure has not only enhanced Qualcomm’s risk resistance ability but also ensured its stable expansion in an uncertain market environment.

Qualcomm is gradually transforming from a traditional chip manufacturer into a cross-domain technology ecosystem enterprise. This transformation has not only opened up new growth space but also made Qualcomm’s long-term investment value more attractive.

Qualcomm is standing at a critical moment of diversified transformation. From financial report data to market trends, whether it is the traditional 5G patent business or the rise in the automotive, AI, and Internet of Things fields, Qualcomm has demonstrated strong growth potential. The licensing business provides a stable “cash cow”, while the automotive and AI sectors are becoming its “new engines”, injecting more momentum into the future.

For investors, Qualcomm is not only a stable participant in the technology industry but also a driver in multiple high-growth markets. Its diversification strategy effectively reduces the risks brought by fluctuations in a single market, and at the same time, it seizes important tracks in the future through innovative products and technologies. This “steady progress” model not only provides support for the current stock price but also injects more possibilities into the long-term investment value.

BiyaPay makes crypto more popular!

Contact Us

Company and Team

BiyaPay Products

Customer Services

Resources

Telegram digital currency community:

https://t.me/BiyaPay666

Community

Sign In

Sign Up

Sign In

Sign Up

Regulation Subject

BIYA GLOBAL LIMITED registered as Financial Service Provider (FSP number: FSP1007221) in New Zealand, and is a member of the Financial Dispute Resolution Scheme, a New Zealand independent dispute resolution service provider.

BIYA GLOBAL LLC registered with the US Financial Crimes Enforcement Network (FinCEN), as a Money Services Business (MSB), registration number: 31000274115551, and regulated by FinCEN.

BIYA GLOBAL LLC To enhance investor protection, BIYA GLOBAL LLC is expediting its Broker-Dealer license application process in full compliance with U.S. SEC and relevant regulatory requirements.

©2019 - 2025 BIYA GLOBAL LIMITED