- Remittance

- Exchange Rate

- Stock

- Events

- EasyCard

- More

- Download

Disney: The Sell-Off Has Gone Too Far

Published on 2024-08-20 Updated on

2024-11-04

Entertainment company Disney (NYSE: DIS) announced a third-quarter financial report that exceeded expectations on August 7, 2024. The profit situation shows that the profitability of its direct-to-consumer business continues to improve. The business reached a turning point in the June quarter and achieved positive operating income for the first time. Disney has added a large number of new users to its Disney + local user base. As Disney continues to return more cash to shareholders and the profit-based stock price is relatively cheap, I believe that for long-term investors, the current risk profile looks much better than at the beginning of the year.

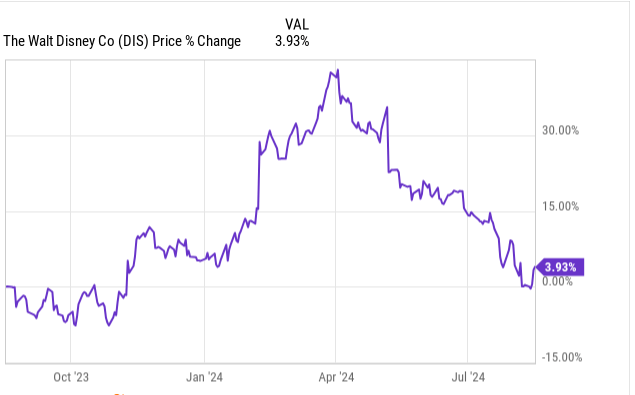

In June, Disney’s investment prospects were good. Since then, the company has announced accelerated capital returns, increased stock buybacks, and increased dividends. Disney also announced a significant cost reduction plan of $7.50 billion, which I believe will greatly support the improvement of profitability. Unfortunately, since June, Disney’s stock price has fallen by 12%, but Disney finally reported its first operating profit from its direct-to-consumer business in the third quarter. I believe the company has made substantial progress in its Streaming Media business, and its stock still has investment prospects after the third quarter.

If you have investment needs, you can consider going to BiyaPay to monitor market trends and wait for the right time to buy. Of course, if you are troubled by deposits and withdrawals, you can also use it as a professional tool for US and Hong Kong stock deposits and withdrawals. Recharge digital currency to exchange for US dollars or Hong Kong dollars, withdraw to your bank account, and then deposit to other securities firms to buy stocks. The arrival speed is fast, there is no limit, and it will not delay the market.

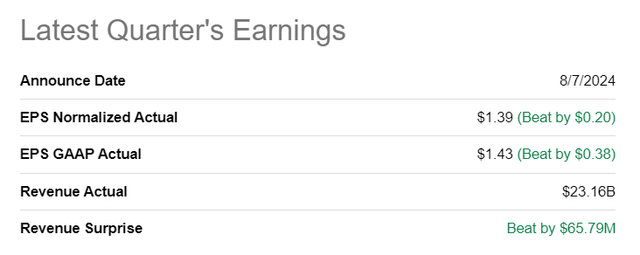

Disney beat estimates, solid subscriber gains in Disney+, inflection point in DTC

Disney beat Wall Street’s expectations for the third fiscal quarter and reported adjusted earnings of $1.39 per share, which surpassed the consensus estimate by $0.20 per-share. The top line also came in ahead of expectations, at $23.2B, topping the consensus estimate by $66M.

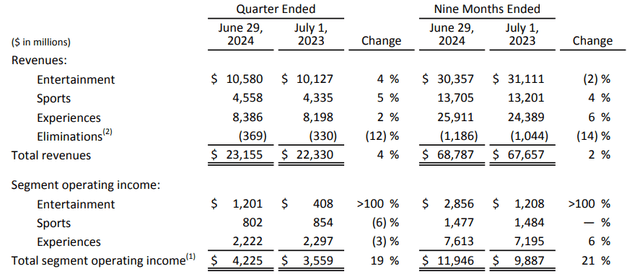

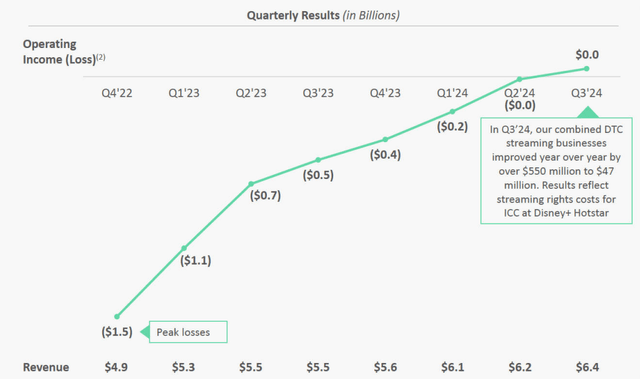

Disney delivered solid results for its third fiscal quarter earlier this month, with the entertainment company posting 4% year-over-year top line growth and revenue of $23.2B. The biggest segment once again was Entertainment, which saw a 4% increase in revenues Y/Y and benefited from a significant boost to its profitability amid a successful turnaround in the streaming business. In Q3’24, Disney reported a 194% increase in Entertainment segment operating income to $1.2B, which was led by Disney’s direct-to-consumer business. All other segments, including Sports and Experiences (which includes the company’s theme parks) reported negative year-over-year operating income growth.

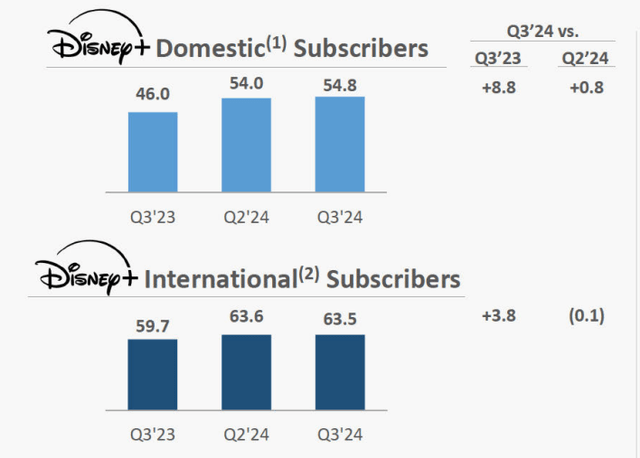

There were two major takeaways from Disney’s third-quarter earnings report earlier this month: 1) Disney continued to grow its domestic subscriber base in the core Disney+ plan, which is where the amount of paying subscribers increased by 800,000 quarter-over-quarter to 54.8M. This positive growth in the domestic market, however, was slightly offset by a decline of 100,000 subscribers in the international Disney+ business.

Disney has been able in the last year to significantly narrow its losses in the streaming business, in part due to growth in (Disney+) subscribers, increases in subscription prices as well as a stricter focus on cost reductions. As a result, Disney finally achieved positive operating income in the amount of $47M. With this inflection point reached, investors can look forward to the direct-to-consumer business reporting positive operating income going forward and making more significant earnings contributions in FY 2025.

Disney’s valuation

Disney’s valuation has suffered greatly in the last couple of months, in part due to concerns about the streaming company’s profitability trajectory as well as fears over a recession which would negatively impact the company’s theme park business.

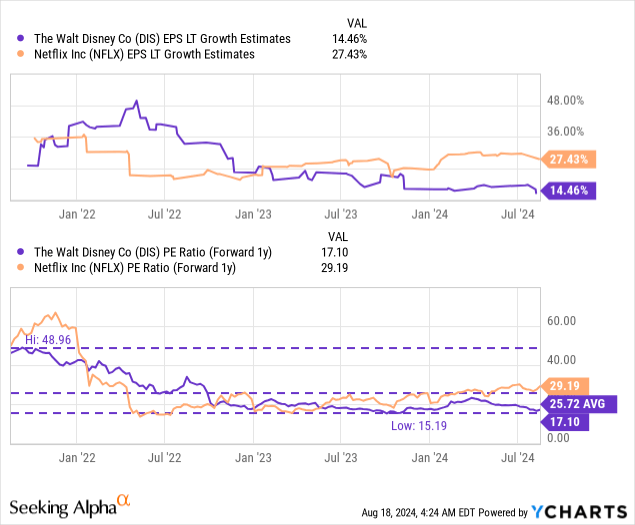

Disney’s shares are currently priced at a P/E ratio of 17.1X, which is 34% below the company’s longer-term average P/E ratio of 25.7X. Netflix’s (NFLX) shares are trading at a 29.2X price-to-earnings ratio and are therefore significantly more expensive. However, Netflix is also expected to grow its EPS about twice as fast as Disney in the future and Netflix has been widely successful in cracking down on password-sharing practices that led to a boost in revenue lately.

In my last work on Disney, I stated that I saw a fair value P/E ratio of 30X (or higher) for the entertainment company in case it managed to grow to profitability in the streaming segment… which is something that I continue to consider a reasonable assumption. A 30X P/E ratio implies a fair value of $157 per-share (based off of a consensus estimate of $5.22 per-share). I believe this fair value could be reached under the conditions that the streaming company achieves significant operating income growth in DTC going forward, realizes estimated cost reductions of $7.5B by year-end (as per guidance) and continues to add profitable subscribers in its Disney+ core subscription offer.

Risks with Disney

The biggest risk for Disney would be a potential contraction in the Disney+ domestic subscriber base, as well as a recession that would surely lower the company’s earnings prospects in the theme park segment. A decline in theme park visitors is highly likely in the event of a recession, which is when consumers are likely to cut back on discretionary spending items. What would change my mind about Disney is if the company were to see a contracting Disney+ subscriber base or failed to build on recent DTC momentum and again reported operating losses in its streaming business in the coming quarters.

Final thoughts

Disney reported a better than expected third fiscal quarter on August 7, 2024, and I don’t believe that the sell-off here is really justified. The streaming company has made fundamental progress in the profitability of its direct-to- consumer business, whose losses weighed on Disney’s shares before. Now that the operating income picture has drastically improved and Disney has a lever to grow its operating income due to subscription price increases and Disney+ domestic subscriber momentum, I believe the risk profile is fundamentally skewed to the upside. In my opinion, the value proposition for Disney has considerably improved after the company’s third-quarter earnings scorecard, and I am confirming my strong buy rating.

BiyaPay makes crypto more popular!

Contact Us

Company and Team

BiyaPay Products

Customer Services

Resources

Telegram digital currency community:

https://t.me/BiyaPay666

Community

Sign In

Sign Up

Sign In

Sign Up

Regulation Subject

BIYA GLOBAL LIMITED registered as Financial Service Provider (FSP number: FSP1007221) in New Zealand, and is a member of the Financial Dispute Resolution Scheme, a New Zealand independent dispute resolution service provider.

BIYA GLOBAL LLC registered with the US Financial Crimes Enforcement Network (FinCEN), as a Money Services Business (MSB), registration number: 31000274115551, and regulated by FinCEN.

BIYA GLOBAL LLC To enhance investor protection, BIYA GLOBAL LLC is expediting its Broker-Dealer license application process in full compliance with U.S. SEC and relevant regulatory requirements.

©2019 - 2025 BIYA GLOBAL LIMITED