- Remittance

- Exchange Rate

- Stock

- Events

- EasyCard

- More

- Download

Broadcom Still Has Strong Legs In The Next Phase Of The 'AI Bubble'

Published on 2024-08-09 Updated on

2024-11-05

Investment Thesis

Market pundits and technological watchers have used the current conditions of extreme volatility seen playing out globally in the last few days to ramp up their discourse about the AI bubble bursting. Some have even revised their outlook, calling for the AI bubble to burst in “days or weeks from now.”

Such comments have caused immense speculation & concern among stocks that are experiencing high growth, especially those stocks that have run far higher than the markets in H1 FY24. Broadcom (NASDAQ:AVGO) is one of those names in the semiconductor industry that has been subject to similar treatments, with the market falling 21% from its YTD highs after creating record all-time highs in June this year.

However, I think the concerns surrounding the AI bubble are inappropriate.

The recent volatility stems from market conditions unrelated to the artificial intelligence bubble. More importantly, given Broadcom’s strong prospects, this stock price decline has created a good opportunity for investors.

If you want to seize the opportunity to get on board, you can go to BiyaPay to buy. If you want to find a better opportunity, you can also monitor the market trend on the platform. Of course, if you are troubled by deposits and withdrawals, you can also use it as a professional tool for deposits and withdrawals of US and Hong Kong stocks. You can recharge digital currency and exchange it for US dollars or Hong Kong dollars, withdraw it to your bank account, and then deposit it to other securities firms to buy stocks. The arrival speed is fast, there is no limit, and it will not delay the market.

The “AI Bubble” Has Room To Expand & AI Capex Offers Meaningful Proof

The only reason I call this an AI bubble is if I compare the current escalation in market capitalization of many stocks to the U.S. Fed’s definition of asset bubbles in 2015 as “an upward price movement over an extended range that then implodes."

Part of that asset bubble definition suddenly seemed to catch the market’s attention over the past week as global volatility surged over the weekend. Many AI/market pundits were quick to rush in and advertise their respective “pound-the-table” moments where they had been calling for the AI bubble to burst.

However, I believe this is not true, and investors should remember that the source of volatility was rather from global market events unfolding with the Japanese yen (USD:JPY) surging after Japan’s Bank of Japan surprised global markets with their first rate hike in over a decade. The surging Japanese yen caused an unraveling in the Yen carry trade, forcing global investors to scale back their positions, especially in those assets that have massively run up through the year. I have recently explained this in detail in my post on Bitcoin and why I expect the volatility to normalize in the near term.

Having established the fundamental reason for the recent sell-off, which has nothing to do with the AI bubble bursting, I will also reiterate the strength of AI spending, of which Broadcom is a beneficiary.

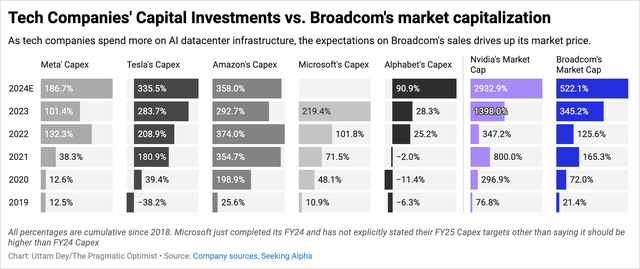

After perusing through many of Big Tech’s earnings calls, I have added a chart below that shows the expected rise in capex since 2018 on a cumulative basis.

As seen above, many large players such as Amazon (AMZN), Alphabet’s Google (GOOG), and Meta Platforms (META) are expected to see significant increases in their capex this year, with Google and Meta Platforms projecting the largest of all increases in 2024. Most of the Big Tech names that I mentioned are large customers of Broadcom and will support the mid-term growth rates of Broadcom’s revenue stream.

How Broadcom Participates In The Next Phase Of The “AI Bubble”

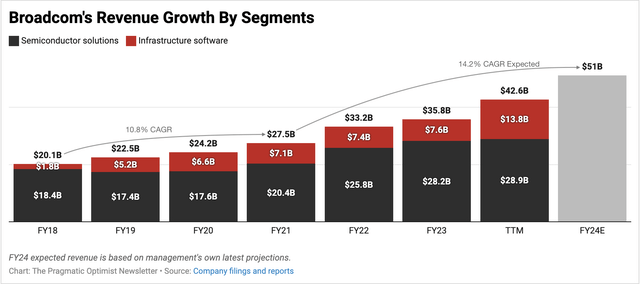

What is clearly visible from Exhibit above is the timing of the increase in capex by the companies I mentioned in the earlier section. All these companies seemed to ramp up their capex spend through 2022, and the timing of these increased investments converges on two things: First is the launch of ChatGPT, launched at the end of 2022. Second is the rising revenue growth seen at Broadcom in Exhibit below.

As seen above, the 10–11% top line growth that Broadcom would consistently deliver before and during the pandemic suddenly increased starting in 2022 and is expected to grow by a CAGR of 14.2%, assuming management’s expectations of the company’s sales this year. While Broadcom has not been the exact beneficiary of AI Capex seen in FY23 as compared to Nvidia (NVDA), I expect the next few years to be stronger for Broadcom as its custom AI chips business helps the company’s hyperscaler customers design their own AI chips and wean off dependency from Nvidia.

Reports of Meta Platforms and Google using Broadcom to scale the v3 and v7 versions of their respective ASICs (application-specific integrated circuits) coincide with the increased capex spend by these two companies, as illustrated in Exhibit B above, as well as with comments from Broadcom’s most recent earnings call, where management said:

For fiscal '24, we expect revenue from AI to be much stronger at over $11 billion. Non-AI semiconductor revenue has bottomed in Q2 and is likely to recover modestly for the second half of fiscal '24. On infrastructure software, we’re making very strong progress in integrating VMware and accelerating its growth. Pulling all these three key factors together, we are raising our fiscal '24 revenue guidance to $51 billion.

I expect Broadcom to sell strongly into the demand for its custom AI semiconductor solutions, which should stay elevated over the next few years, implying at least 23% compounded growth through FY26. Selling strongly into demand also means that Broadcom can pursue its higher pricing strategy, implying either sustaining current adj. EBITDA margins or expanding them.

Valuation Suggests Strong Upside for Broadcom

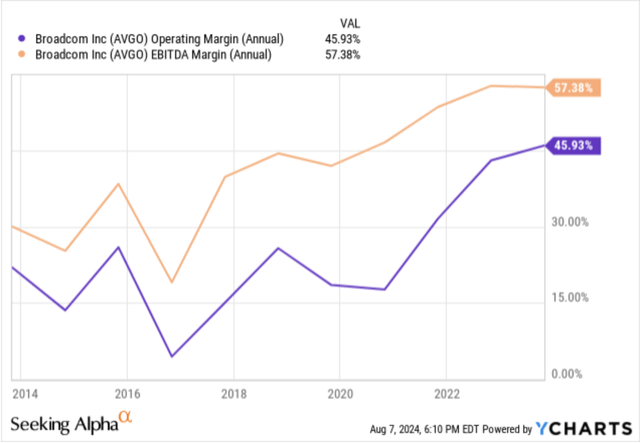

In addition to the strong +23% CAGR top-line growth that I expect for Broadcom, I also believe the company will be able to deliver robust earnings growth. As can be seen in Exhibit below, Broadcom has been expanding its margins by massive levels since the pre-pandemic. These margin expansions reflect strong pricing power and will continue to support the margin expansion in the coming years.

Broadcom’s management expects they will deliver 61% adjusted EBITDA margins in FY24, and I believe the company can continue to sustain these margins through FY26. What further gives me confidence in Broadcom to maintain these margins is the recent credit upgrade from Fitch Ratings this week, who also believe Broadcom can sustain adj. EBITDA margins “in the low-60%.”

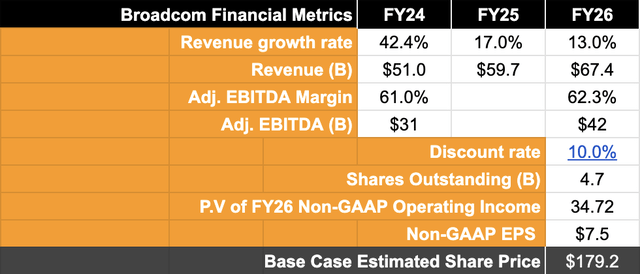

Based on these assumptions, I expect Broadcom to deliver a 22-23% CAGR in adj. EBITDA through FY26, as illustrated in Exhibit . My valuation model below assumes a discount rate of 10%.

Based on this valuation and expectation of 22-23% CAGR EBITDA growth, I believe a forward PE of 30-31x would have been warranted.

Note on Broadcom’s Debt: However, since the company holds large amounts of debt, it would impact the valuation multiple. Per the 10-Q, Broadcom carries $71.6 billion of debt and ~$9.8 billion in cash and equivalents. This does seem like a substantial volume of debt for Broadcom to carry, but taking into account its estimated FY24 adj. EBITDA margin of ~61%, that implies an adj. leverage ratio of ~2x, which is reasonably manageable in my opinion. Still, such substantial volumes of debt will mean Broadcom incurs interest expenses of ~$2.8 billion per year.

If I factor in these interest expenses, I believe Broadcom should be valued at ~24x forward earnings, which implies 31–32% upside from current levels.

Risks & Other Factors To Consider

One of the primary attractive qualities of Broadcom’s stock is its industry-leading adj. EBITDA margins. Hence, any threat to those margins would directly diminish the valuation multiple that my model applies.

At the moment, an unknown factor is the extent to which Taiwan Semiconductor’s (NYSE:TSM) reported price hikes may impact Broadcom’s handsome margins. ~90% of Broadcom’s chip production is managed by Taiwan Semi. The details of the capacity contracts that Taiwan Semi’s price increases impact are still unknown. I do not expect a significant impact yet, at least not until next year.

In terms of market volatility, I expect this to normalize in the immediate term which should restore stability in markets soon. BoJ has recently issued another clarification stating its intention to abstain from raising interest rates amid unstable financial market conditions.

Takeaway

After the recent volatile pullback in markets, Broadcom looks all set to begin another rally as its valuation appears attractive once again. The demand for custom AI chips being led by Broadcom’s hyperscaler customers will lead to strong revenue growth for the San Jose, CA-headquartered company and allow Broadcom to sustain its industry-leading +60% adj. EBITDA margins.

I believe the next phase of AI is still underway, and Broadcom will be a strong beneficiary.

BiyaPay makes crypto more popular!

Contact Us

Company and Team

BiyaPay Products

Customer Services

Resources

Telegram digital currency community:

https://t.me/BiyaPay666

Community

Sign In

Sign Up

Sign In

Sign Up

Regulation Subject

BIYA GLOBAL LIMITED registered as Financial Service Provider (FSP number: FSP1007221) in New Zealand, and is a member of the Financial Dispute Resolution Scheme, a New Zealand independent dispute resolution service provider.

BIYA GLOBAL LLC registered with the US Financial Crimes Enforcement Network (FinCEN), as a Money Services Business (MSB), registration number: 31000274115551, and regulated by FinCEN.

BIYA GLOBAL LLC To enhance investor protection, BIYA GLOBAL LLC is expediting its Broker-Dealer license application process in full compliance with U.S. SEC and relevant regulatory requirements.

©2019 - 2025 BIYA GLOBAL LIMITED