- Remittance

- Exchange Rate

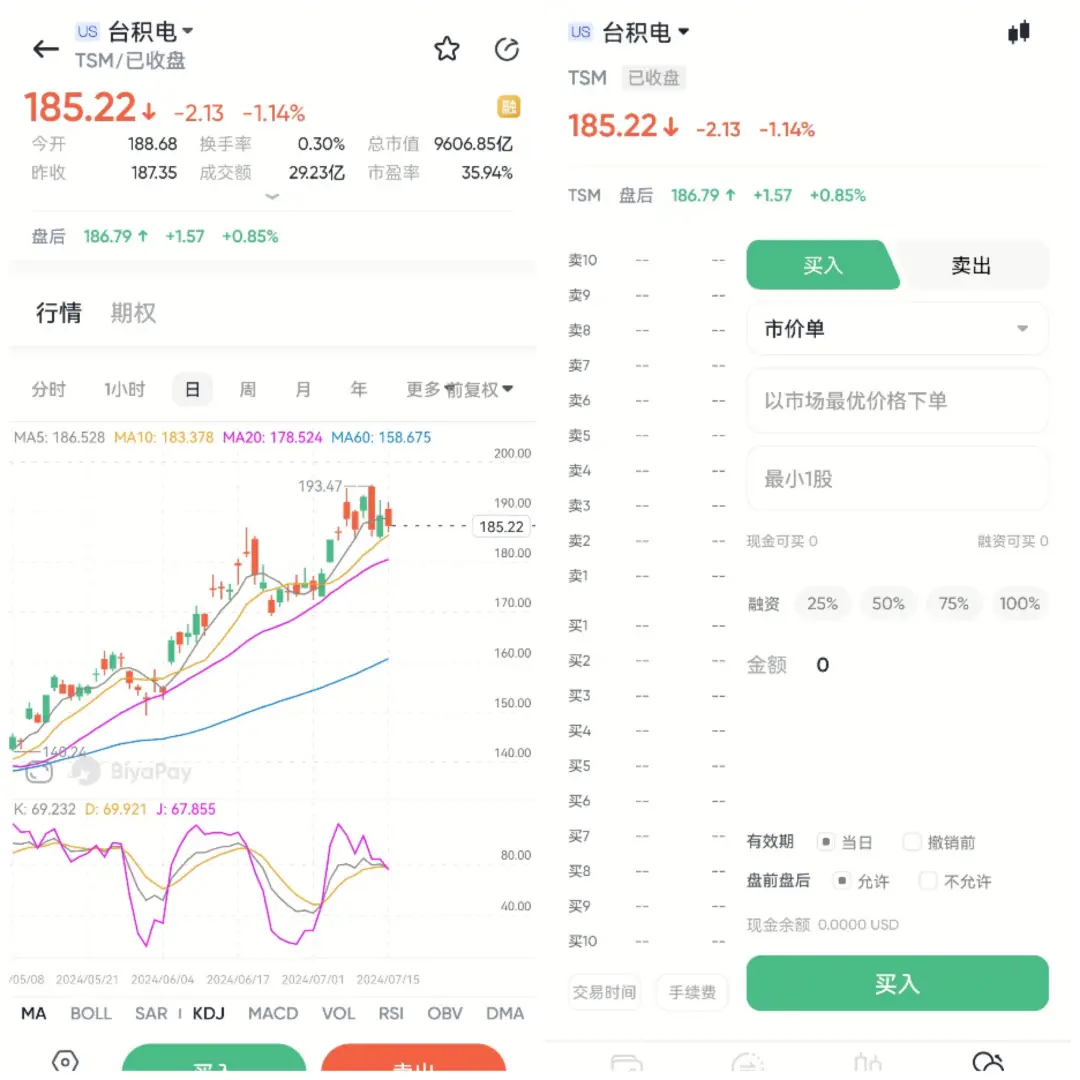

- Stock

- Events

- EasyCard

- More

- Download

TSMC: Crushing Sales Targets Ahead Of Q2 Earnings

Published on 2024-07-16 Updated on

2024-11-05

Last week, Taiwan Semiconductor Manufacturing Company (New York Stock Exchange code: TSM ) (also known as TSMC) released its June revenue report. However, TSMC has not yet released official dollar data for the month, but according to the company’s report, combined with exchange rates, the revenue for the month reached nearly $6.50 billion. We now have three monthly revenue reports, which means we can predict with high accuracy how much full-quarter revenue the company may receive.

These reports seem to indicate that TSMC is earning huge profits from the large-scale investment in generative artificial intelligence worldwide. The company has achieved double-digit sales growth in each of the past three months, which means that the revenue growth in the entire second quarter is high. We can already estimate the company’s revenue in the second quarter: the revenue for April, May, and June, calculated at today’s exchange rate, is equivalent to $20.69 billion. The figure for the same period last year was $15.40 billion. Therefore, it seems that TSMC’s revenue growth rate is close to 35% year-on-year.

TSMC’s success in AI chips is worth paying attention to, as not all companies involved in the AI field can profit from it. For example, Meta Platforms ( META) stated that its AI investment will take several years to pay off. Then there are companies like NVIDIA ( NVDA ) that are benefiting from AI, and their stock prices fully reflect this fact . Although TSMC is not cheap, its valuation is quite moderate by the standards of today’s large technology companies, with a Price-To-Earnings Ratio of 35.69 times . So it’s a relatively affordable way to add some investment in generative AI accelerator chips to your portfolio.

Previously, I thought this stock was relatively cheap and had high growth potential, which was worth investing in. Now, the released revenue report also confirms its growth potential and exceeds expectations. Although the current stock price has risen, I still believe that its growth prospects are worth investing in.

If you agree with my point of view but are still considering it, I suggest you go to BiyaPay, search for stock codes on the platform, monitor market trends, and get on board at the right time. Of course, you can also use the platform as a professional tool for depositing and depositing US and Hong Kong stocks. You can recharge digital currency and exchange it for US dollars or Hong Kong dollars, withdraw it to your bank account, and then deposit it to other securities firms to buy stocks. The deposit speed is fast and there is no limit.

BiyaPay App

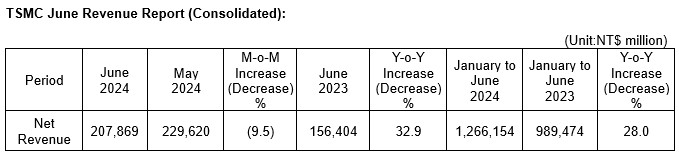

TSM’s June Revenue Report in Detail

When Taiwan Semiconductor Manufacturing released its June revenue report, it included a number of useful tidbits of information apart from the revenue figure itself. These included:

- 28% first half revenue growth.

- 32.9% year over year (y/y) June quarter revenue growth.

- -9.5% month over month (m/m) June quarter revenue growth.

TSMC revenue report (TSMC)

For the most part, the numbers TSMC put out were encouraging. On a year-over-year basis, revenue increased considerably. On the other hand, the -9.5% m/m growth was disappointing. The March quarter saw semiconductor sales growth well above the established seasonal trend. So, the June quarter sales slowdown may simply have been a return to the established trend. If that’s the case, and if demand for AI chips remains strong, then we should eventually see TSMC re-take and then surpass the May level, as the “established” trend is one of high long-term growth. For example, according to Seeking Alpha Quant, TSM has a 17.5% five-year CAGR revenue growth rate and a 20.69% five-year CAGR earnings growth rate. Though it has booked a bad quarter/month here and there, the company is growing long term.

Valuation

Having looked at TSMC’s revenue trends in detail, we can now begin to model its second quarter results. I already did some of this work in preceding paragraphs, where I wrote that I expected between $20.6B and $21B in revenue for the quarter. Let’s put our estimate at $20.8B (the average) to keep things simple.

The next step is the expenses. Reviewing TSM’s past earnings releases, I found that the company’s cost of goods sold (“COGS”) increased pretty reliably with revenue from year to year. COGS was 46% of revenue last quarter; therefore, if TSM hits my $20.8B revenue target, COGS will be about $9.56B.

TSM’s operating expenses do not rise in tandem with revenue in any predictable fashion. The company’s first quarter operating expenses were actually lower than its fourth quarter and third quarter 2023 operating expenses. TSM’s “expense” category includes a lot of R&D and other hard to predict categories. For this reason, I will assume that second quarter operating expenses remain unchanged from last quarter at $2.08 billion. So we get $9.16 billion in EBIT, which is $7.78 billion after subtracting a 15% tax (the company’s interest expenses are negligible, about 0.4% of revenue last quarter). TSM has 25.929 billion shares outstanding, so we get approximately $0.30 in earnings per share, or $1.50 in earnings per ADR. This represents approximately 36% growth from the year ago quarter when TSMC earned $0.22.

If we assume that $1.50 reflects TSM’s average quarterly earnings per ADR over the next 12 months, then the stock will earn $6 and trade at 31.2 times forward earnings, which is cheaper than the multiple you’d get by using trailing earnings. Seeking Alpha Quant projects a 29 forward P/E ratio, lower than mine. This stock is certainly getting a bit pricey, but if it can continue growing at the pace it has been, then it will end up doing more than $1.50 in quarterly earnings. If it can achieve $2 in quarterly EPS, then the forward multiple (assuming the stock price doesn’t change) will come down to 23.5.

I think TSM stock will prove to have been well worth the investment at today’s prices if the scenario just mentioned plays out. It isn’t inconceivable either: TSM’s December 2022 EPS was $0.37, which is equivalent to $1.85 in earnings per ADR–just a stone’s throw away from $2. If Taiwan Semiconductor still has all the competitive advantages it had back then, and if companies keep spending big on AI chips, then $2 in quarterly EPS should be do-able.

Will Taiwan Semiconductor’s Moat Last?

It’s one thing to note that a company has very good financials and a fairly sensible valuation, but quite another thing to predict that the party will continue. In order to determine whether the party will continue, we need to look at the company’s competitive edge.

As of today, Taiwan Semiconductor is the biggest semiconductor manufacturing company in the world, with a 61% market share. It also has a 100% share of NVIDIA and Apple’s (AAPL) business–those are some of the most lucrative contracts in the world of semiconductor manufacturing.

We also know that the U.S. government is giving a lot of money to TSMC’s competitors. Intel (INTC), for example, has received over $8.5 billion in CHIPS Act grants, and a lot of that is for manufacturing. Intel is trying to make itself into the next semiconductor manufacturing giant, and it is getting considerable government support in this enterprise. However, as a company that both designs and manufactures chips, it has possible conflicts of interest (specifically, it has an interest in privileging its own orders over clients’ orders). The company’s executives evidently consider this a serious concern, as they spent some time touting how Intel Foundry charges Intel “fair market prices” for its services. It could be that Intel will succeed with this model, but for now, TSMC’s total lack of conflicts of interest is a major competitive edge.

Another competitive edge that Taiwan Semiconductor enjoys is its technological know-how. The company has been building chips for Apple and NVIDIA for so long now, that it is intimately familiar with their designs. This fact incentivizes those companies to stick with TSMC, as fulfilling their orders is a complex technical task involving the use of high-end EUV lithography machines that cost $380 million. New upstarts can’t just enter this industry on a whim, while established competitors lack TSMC’s massive manufacturing capacity (TSMC’s capacity is 16 million wafers per year, while Intel’s is only 2.5 million).

Conclusion

If Taiwan Semiconductor Manufacturing can continue growing at the pace it has been growing, then its stock is worth owning today. It just needs to hit $2 in quarterly earnings per ADR to be worth more than the price it trades for. Getting to that level will take some doing, but considering its competitive edge, TSMC will probably get there eventually.

BiyaPay makes crypto more popular!

Contact Us

Company and Team

BiyaPay Products

Customer Services

Resources

Telegram digital currency community:

https://t.me/BiyaPay666

Community

Sign In

Sign Up

Sign In

Sign Up

Regulation Subject

BIYA GLOBAL LIMITED registered as Financial Service Provider (FSP number: FSP1007221) in New Zealand, and is a member of the Financial Dispute Resolution Scheme, a New Zealand independent dispute resolution service provider.

BIYA GLOBAL LLC registered with the US Financial Crimes Enforcement Network (FinCEN), as a Money Services Business (MSB), registration number: 31000274115551, and regulated by FinCEN.

BIYA GLOBAL LLC To enhance investor protection, BIYA GLOBAL LLC is expediting its Broker-Dealer license application process in full compliance with U.S. SEC and relevant regulatory requirements.

©2019 - 2025 BIYA GLOBAL LIMITED