- Remittance

- Exchange Rate

- Stock

- Events

- EasyCard

- More

- Download

After Micron's stock price skyrocketed by 60%, it was suddenly lowered. Is there a buying opportunit

Published on 2024-07-11 Updated on

2024-11-05

It’s no secret that chip stocks, including and especially NVIDIA (NVDA), have been among the best performers in the stock market all year. Memory hardware vendors like Micron (NASDAQ:MU) have benefited tremendously as well from the surge in investment into AI applications and datacenters, turning around a highly cyclical industry that has recently dealt with a glut of oversupply.

Year to date, Micron is up nearly 60%, though a recent dip has taken the stock into a technical correction from YTD highs above $150. For those who missed out on the earlier Micron upsurge, I believe this is an opportunity to buy in.

I’m putting a buy rating on Micron, despite its strong YTD rally. The main crux of my bull case for this stock is the fact that, though the major memory suppliers (Micron, Western Digital (WDC), and Korean rival SK Hynix) have typically gone through short boom-and-bust cycles in the memory industry governed by periods of tight supply and oversupply, the AI investment cycle is expected to be a multi-year investment cycle that will benefit memory prices for a sustained period of time.

But it’s not just enterprise investment into AI-ready datacenters that is fueling demand, either. As we’ll discuss in the next section, other end-markets are also benefiting from secular demand tailwinds that will benefit Micron’s trajectory.

All in all, while many AI-type plays may be speculative buys after this year’s rapid run-up, Micron still has plenty of steam left in its rally to go.

I suggest you seize this buying opportunity. You can go to BiyaPay, search for stock codes on the platform, monitor market trends, and get on board at the right time. You can also use the platform as a professional tool for depositing and depositing US and Hong Kong stocks, recharge digital currency to exchange for US dollars or Hong Kong dollars, withdraw to your bank account, and then deposit to other securities firms to buy stocks. The arrival speed is fast and there is no limit.

End markets are looking favorable for a number of reasons

We don’t need to reiterate the number-one reason that customers are snapping up memory and other chips to invest in AI datacenters:

But there are several smaller key points to emphasize here:

- AI will drive a multi-year investment cycle, especially as applications and use cases are still being figured out and customers continue to invest to meet adapting needs

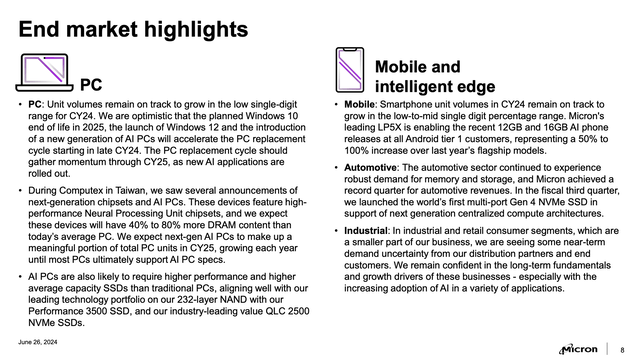

- The impact of AI will be across devices, not just enterprise datacenters. Expected upgrades to PCs and mobile devices will also spur consumer upgrade cycles

However, it’s also key to realize that AI is not the only factor driving strong memory demand at the moment. In particular, note that Windows 10 is reaching its end of life at the end of calendar 2025, which will render a lot of PCs useless and necessitate upgrades. Coinciding with the Windows 12 launch later this year, Micron is expecting significant PC upgraders between this year and next:

There are also secular tailwinds in the mobile and automotive spaces as well. In mobile, one of the biggest drivers to point out is that as cameras on phones continue to improve, and applications become more and more sophisticated and complex, file sizes will continue to swell: necessitating more NAND storage. And in automotive, as more cars roll out connected features and in-car displays and control centers, memory will also continue to be a core input.

Industry dynamics are pushing up prices and bolstering margins

The view that the memory markets are in a multi-year upsurge isn’t just Micron’s house view, but rather an industry consensus.

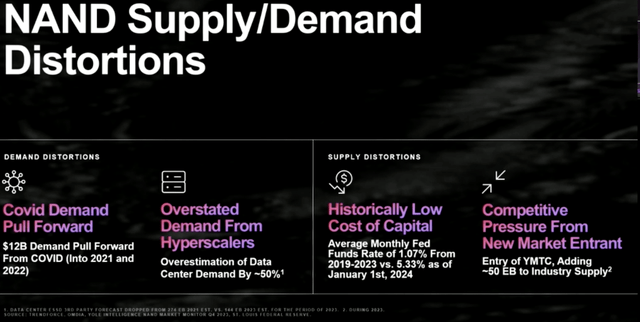

We note that Western Digital just hosted a special investor conference titled the “New Era of NAND,” in which it cited that COVID pulled a lot of datacenter and device investment forward (leaving 2023 a barren year for memory suppliers), coupled with oversupply from the various memory suppliers as interest rates were very low (stimulating investment into capex).

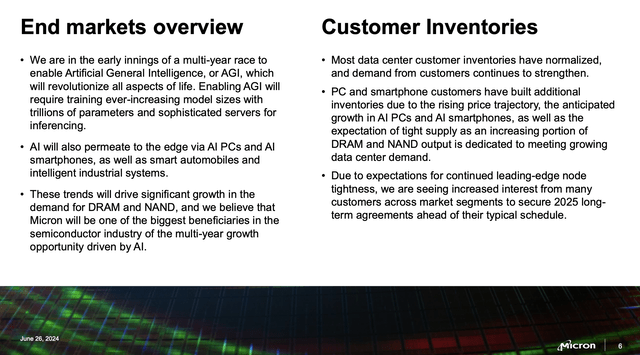

Now, however, the supply/demand equation has changed. On the supply side, Micron notes that data center inventories have normalized, and we’ve already discussed all the tremendous demand drivers, including and especially AI.

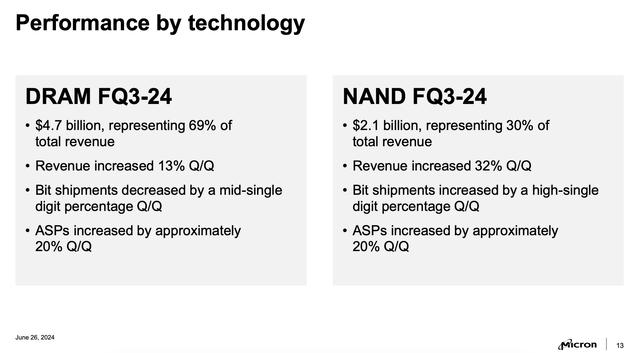

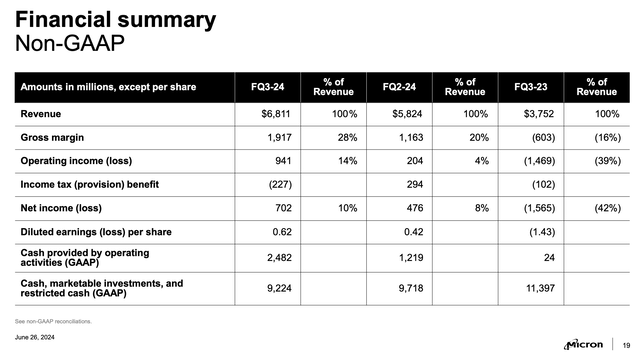

The net result of this is a sharp increase in memory pricing. As shown in Micron’s earnings summary by memory segment below from its most recent quarter (FQ3, which is the May-end quarter for Micron), ASPs for both DRAM and NAND jumped by “approximately 20%” sequentially versus FQ2:

What’s more, the increase in pricing is making many customers nervous and prompting advance purchases of memory to try to get ahead of spot rate increases.

Per CEO Sanjay Mehrotra’s remarks on the recent Q3 earnings call (key points highlighted):

Most data center customer inventories have normalized, and demand from customers continues to strengthen. PC and smartphone customers have built additional inventories due to the rising price trajectory, the anticipated growth in AI PCs and AI smartphones, as well as the expectation of tight supply as an increasing portion of DRAM and NAND output is dedicated to meeting growing data center demand. Due to expectations for continued leading-edge node tightness, we are seeing increased interest from many customers across market segments to secure 2025 long-term agreements ahead of their typical schedule.

In data center, industry server unit shipments are expected to grow in the mid-to-high single digits in calendar 2024, driven by strong growth for AI servers and a return to modest growth for traditional servers. Micron is well positioned with our portfolio of HBM, D5, LP5, high-capacity DIMM, CXL, and data center SSD products.

Recently, our customers have announced their long-term AI server product roadmaps, with an annual cadence of new products with significantly improved capabilities for the next several years. Micron’s technology and product leadership puts us in an excellent position to support this growth."

We don’t need to wait quarters into the future to see the impact on Micron’s results. In Q3, Micron’s gross margin jumped from -16% in the year-ago Q3 (a particularly sharp down cycle for memory vendors) to positive 28% (also improving eight point q/q, alongside the 20% sequential jump in DRAM and NAND ASPs per bit).

What’s more, the increase in pricing is making many customers nervous and prompting advance purchases of memory to try to get ahead of spot rate increases.

Per CEO Sanjay Mehrotra’s remarks on the recent Q3 earnings call (key points highlighted):

Most data center customer inventories have normalized, and demand from customers continues to strengthen. PC and smartphone customers have built additional inventories due to the rising price trajectory, the anticipated growth in AI PCs and AI smartphones, as well as the expectation of tight supply as an increasing portion of DRAM and NAND output is dedicated to meeting growing data center demand. Due to expectations for continued leading-edge node tightness, we are seeing increased interest from many customers across market segments to secure 2025 long-term agreements ahead of their typical schedule.

In data center, industry server unit shipments are expected to grow in the mid-to-high single digits in calendar 2024, driven by strong growth for AI servers and a return to modest growth for traditional servers. Micron is well positioned with our portfolio of HBM, D5, LP5, high-capacity DIMM, CXL, and data center SSD products.

Recently, our customers have announced their long-term AI server product roadmaps, with an annual cadence of new products with significantly improved capabilities for the next several years. Micron’s technology and product leadership puts us in an excellent position to support this growth."

We don’t need to wait quarters into the future to see the impact on Micron’s results. In Q3, Micron’s gross margin jumped from -16% in the year-ago Q3 (a particularly sharp down cycle for memory vendors) to positive 28% (also improving eight point q/q, alongside the 20% sequential jump in DRAM and NAND ASPs per bit).

This, in turn, helped net income jump to $702 million, despite a loss twice that large in the year-ago quarter.

Valuation and key takeaways

Wall Street analysts are expecting Micron to generate pro forma EPS of $9.53 in FY25 (the year for Micron ending in August 2025), which is predicated on 54% y/y revenue growth to $38.6 billion (compared to 82% y/y growth in Micron’s most recent quarter, and consensus expectations for 91% growth in FQ4). This puts Micron’s valuation multiple at 13.7x FY25 P/E.

Micron and its peers have historically traded at valuation multiples that are at a discount to the broader market (in the low teens range) due to the short boom-and-bust nature of memory pricing: but as outlined above, there are a number of reasons to believe the benefits of AI and other end-market drivers may provoke a multi-year upcycle.

It is worth noting that Micron is trading at a premium to rival Western Digital at a ~10x forward P/E, but that premium is justified as Western Digital investors are waiting for clarity on an upcoming flash division spin-off to be finalized later this year.

Summary

In summary, based on the previous analysis, I believe that Micron is a stock worth buying with a Price-To-Earnings Ratio of about 15 times. Please seize this opportunity to buy during the decline.

BiyaPay makes crypto more popular!

Contact Us

Company and Team

BiyaPay Products

Customer Services

Resources

Telegram digital currency community:

https://t.me/BiyaPay666

Community

Sign In

Sign Up

Sign In

Sign Up

Regulation Subject

BIYA GLOBAL LIMITED registered as Financial Service Provider (FSP number: FSP1007221) in New Zealand, and is a member of the Financial Dispute Resolution Scheme, a New Zealand independent dispute resolution service provider.

BIYA GLOBAL LLC registered with the US Financial Crimes Enforcement Network (FinCEN), as a Money Services Business (MSB), registration number: 31000274115551, and regulated by FinCEN.

BIYA GLOBAL LLC To enhance investor protection, BIYA GLOBAL LLC is expediting its Broker-Dealer license application process in full compliance with U.S. SEC and relevant regulatory requirements.

©2019 - 2025 BIYA GLOBAL LIMITED