- Remittance

- Exchange Rate

- Stock

- Events

- EasyCard

- More

- Download

Micron Technology's AI chip was sold out, but the stock price unexpectedly fell? An investment oppor

Published on 2024-05-21 Updated on

2024-11-05

Summary

- Micron’s flagship chip for AI servers is already sold out for the next year, indicating strong demand and technological edge in the AI revolution.

- The company’s diverse segments and products help address revenue concentration risks and demonstrate impressive growth momentum.

- Micron’s expansion into the SSD market and its position to capture AI tailwinds make it an attractive investment with a low valuation.

- I believe such an AI powerhouse should trade at a premium to its fair value. However, MU stock currently trades at a double-digit discount.

Introduction

Micron (NASDAQ:MU) enjoys the wave of ramping up investments in cloud computing and artificial intelligence (‘AI’). Its flagship chip for AI servers is already sold out for the next calendar year’s demand, indicating technological edge. Other segments also demonstrate massive growth momentum, and I consider expansion to SSD to be promising as well. MU is very attractively valued for an AI stock with a 10% discount to the fair value, while I believe that such an AI powerhouse deserves a premium to the stock price. Therefore, Micron Technology is quite worthy of investors’ consideration.

Investors who have investment intentions can choose a more reliable securities firm for investment. For example, Jiaxin Wealth Management is a globally renowned investment securities firm. By opening an account with Jiaxin Wealth Management, you can obtain a bank account with the same name. You can deposit digital currency (USDT) into the multi-asset wallet BiyaPay, and then withdraw fiat currency to Jiaxin Securities for investment. Of course, investors can also search for the MU stock code on the platform first, monitor the stock price regularly according to their investment strategy, and choose the appropriate time to buy stocks.

MU Market Trend, Chart BiyaPay App

Fundamental analysis

Micron is one of the world’s leading suppliers of semiconductor memory products. In its latest annual report, the company ranks itself as the ‘fifth largest semiconductor company in the world’. To better understand the company’s business, please take a look at Micron’s segments below.

Micron’s FY 2023 annual report

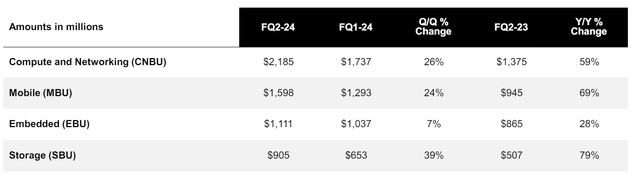

Wide diversity across various segments and products helps to address revenue concentration risks, which adds to any company’s fundamental strength. CNBU has historically been MU’s largest segment and generated 37% of the total revenue in FY 2023.

According to the last quarter’s (fiscal Q2) performance, the business experiences positive momentum across all four segments. The YoY growth is impressive across all four business units, and three out of them demonstrated above 50% increases. At the consolidated level, MU delivered a 58% YoY revenue growth. The EPS has improved YoY from -$1.91 to $0.42.

Micron’s FQ2 presentation

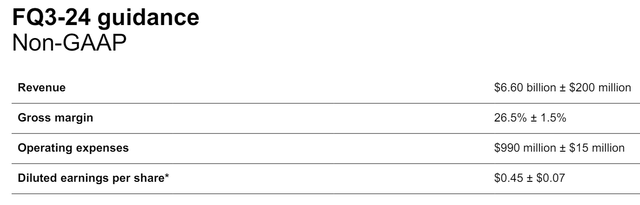

There was a notable guidance boost for fiscal Q3 as well. The management expects YoY revenue growth to accelerate to 76%. The EPS is also expected to demonstrate sequential growth, from $0.42 to $0.45. It is also crucial to mention that Mark Murphy, the CFO, said that the management expects record revenue in fiscal 2025. This means that the management considers the current growth momentum to be sustainable over the next several quarters.

Micron’s FQ2 presentation

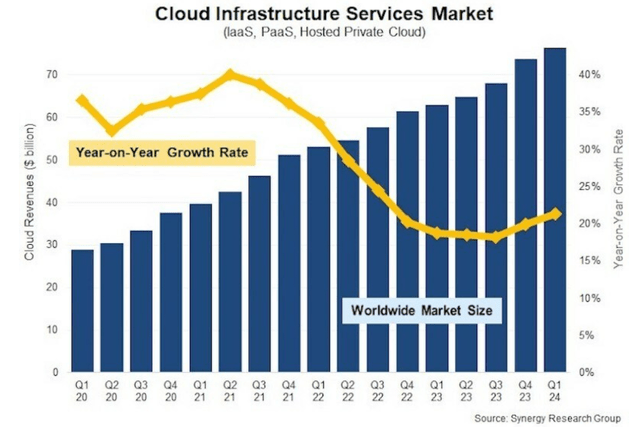

The management’s optimism appears to be reasonable. The company’s largest segment, CNBU, has strong exposure to cloud servers. Due to the AI race, the cloud industry gained robust momentum in recent quarters. According to Synergy Research Group, the cloud market’s growth rate has improved significantly in recent quarters compared to a 2022 dip. According to the presentation, strong AI server demand was one of the major positive catalysts for the company’s financial performance in fiscal Q2. Therefore, I expect MU to continue capturing the effect of positive developments around cloud and AI.

Synergy Research Group

It is also crucial that a rapid ramp up of investments in data centers, cloud and AI boosts the demand for Micron’s offerings. For example, Micron has already sold out the entire 2024 demand and most of the 2025 demand for its most technologically advanced solution for AI innovation, HMB3E. Having its most cutting-edge product sold out means that Micron indeed provides leading technologies in its niche. Moreover, strong demand allows Micron to exercise pricing power. This is another robust bullish catalyst for MU.

There is another massive positive catalyst for Micron’s solutions exposed to AI. Analysts of JPMorgan (JPM) expect the AI servers market to increase from $41 billion in 2023 to $283 billion in 2028, which is a 47% CAGR. Micron recently secured a $13 billion governmental support under Chips Act. This increases the probability that Micron will be able to meet the surging demand for its products.

Another promising trend is Micron’s recent aggressive expansion into the SSD market. As we saw in one of the above tables, Micron’s Storage business is the fastest growing segment at the moment. This segment includes SSD solutions, and the whole SSD industry is expected to deliver a 17.6% CAGR over the next five years. Diversification of the business mix is a strong strategic initiative which will help Micron to deliver smoother financial performance over the long term.

Valuation analysis

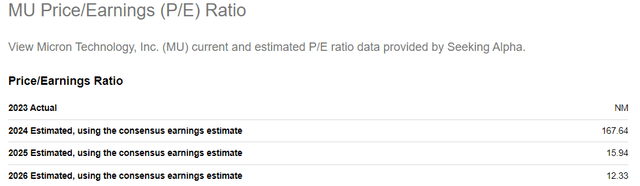

Micron’s above 100 forward non-GAAP P/E ratios should not mislead readers. Due to the robust EPS expansion, which is expected by consensus, the P/E ratio is expected to contract to just 12 in FY 2026. For a company that is positioned to capture massive AI tailwinds, a 12 P/E ratio is extremely low. For example, a highly defensive U.S. Utilities (XLU) sector which usually grows in low-single digits currently trades at an average 20.8 P/E ratio. Therefore, MU is cheap from the P/E perspective.

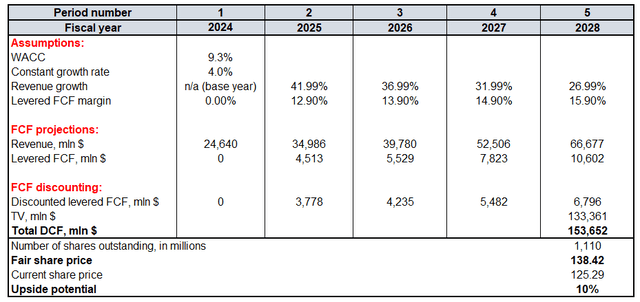

Running a discounted cash flow (‘DCF’) model will be useful in adding more conviction about Micron’s undervaluation. Future cash flows will be discounted with a 9.3% WACC. Revenue consensus estimates for 2024-2025 consists of opinions of more than 30 Wall Street analysts and I consider this sample to be representative enough to rely on. For years after 2025 I prefer to be conservative and incorporate a notable five percentage points revenue deceleration per year. Due to strong secular industry tailwinds, I think that Micron will be able to deliver a 4% constant growth rate, two times higher than historical inflation levels.

The same source, the consensus, expects the company’s EPS to be below one in FY 2024. That is the reason why I use zero FCF margin for the base year of my DCF. However, the adjusted EPS is expected by consensus to move closer to $8 per share. The last time MU delivered (fiscal year 2018) such an EPS, the company generated 12.9% in levered FCF margin. Therefore, I incorporate this FCF margin for FY 2025. Since my analysis suggests that MU is positioned well to benefit from AI tailwinds, I think that I have to incorporate FCF margin improvements. Since revenue growth assumptions are already aggressive, I think that for the FCF margin expansion I have to be more conservative and projecting a 100 basis points yearly expansion is reasonable. Relevant data shows that Micron Technology currently has 1.10 billion shares published outside.

The fair share price is $138. MU trades with a 10% discount, which is an attractive deal for one of the AI boom powerhouses. To sum up, I believe that Micron’s current valuation is quite attractive.

Mitigating factors

The rapid development of memory technology requires companies to continuously upgrade and innovate. Micron has a leading position in high-performance memory and storage technology, but also faces technical risks. If the company lags behind its competitors in technological innovation, it may lose market share. Therefore, Micron invests heavily in research and development every year to ensure continuous innovation in high-performance memory and storage technology, enabling it to launch high-performance and high-reliability products to meet market demand and ensure its leading position.

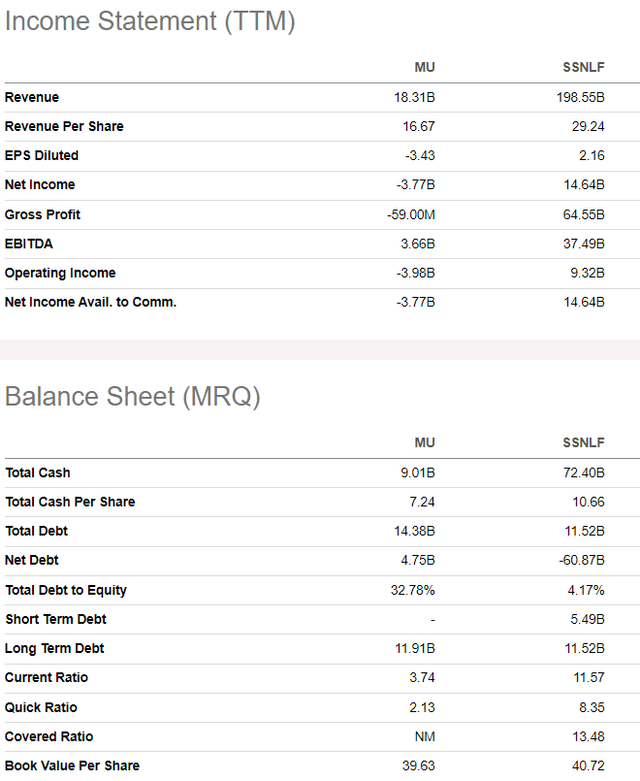

Micron is not alone in the industry. Direct competitors are formidable players, and Samsung Electronics (OTCPK:SSNLF) is one of the closest rivals. This giant is a by far larger player compared to Micron. Samsung contributes more than 20% to the South Korean GDP and possesses massive financial resources. Both companies are incomparable in terms of the income statement and balance sheet. That said, Micron faces substantial competition risks. On the other hand, memory solutions are not Samsung’s main business line, while Micron is laser-focused on one industry. This might give Micron a competitive advantage in terms of innovation where companies directly compete.

Conclusion

Overall, Micron Technology is clearly a powerful artificial intelligence (AI) giant. The company’s latest AI server chips have been sold out, meeting the demand for the whole year, which fully demonstrates the company’s potential in this emerging industry. The valuation is attractive, and all business departments of the company have shown strong strength, which is worth considering.

Source: Seeking Alpha

Editor: BiyaPay Finance

BiyaPay makes crypto more popular!

Contact Us

Company and Team

BiyaPay Products

Customer Services

Resources

Telegram digital currency community:

https://t.me/BiyaPay666

Community

Sign In

Sign Up

Sign In

Sign Up

Regulation Subject

BIYA GLOBAL LIMITED registered as Financial Service Provider (FSP number: FSP1007221) in New Zealand, and is a member of the Financial Dispute Resolution Scheme, a New Zealand independent dispute resolution service provider.

BIYA GLOBAL LLC registered with the US Financial Crimes Enforcement Network (FinCEN), as a Money Services Business (MSB), registration number: 31000274115551, and regulated by FinCEN.

BIYA GLOBAL LLC To enhance investor protection, BIYA GLOBAL LLC is expediting its Broker-Dealer license application process in full compliance with U.S. SEC and relevant regulatory requirements.

©2019 - 2025 BIYA GLOBAL LIMITED