- Remittance

- Exchange Rate

- Stock

- Events

- EasyCard

- More

- Download

After Cisco's stock price plummeted and weakened, will the stock price reach a turning point in the

Published on 2024-05-15 Updated on

2024-11-04

Introduction

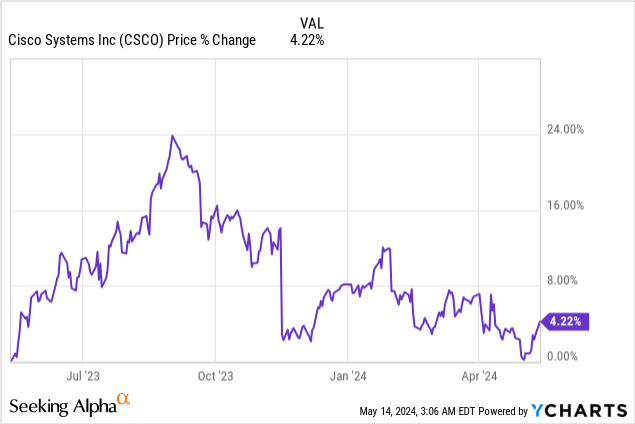

Cisco Systems, Inc. (NASDAQ:CSCO) is about to report its fiscal Q3 2024 earnings later this week.

The stock is now almost flat for the past year, as it fell sharply when Q1 2024 results were released in November of last year.

Although CSCO reported better-than-expected results during the fiscal Q1 2024 release in November of last year, it was the much weaker guidance for the whole fiscal year that spooked investors.

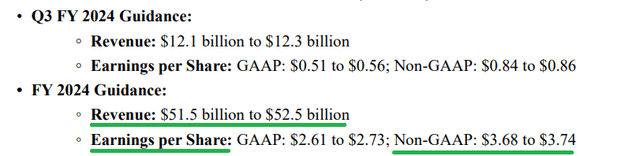

nitial revenue guidance for FY 2024 stood within the range of $57bn to $58.2bn, with Non-GAAP Earnings Per Share expected to be slightly above $4.

By the end of Q2 2024, the revenue outlook has come down massively to a range $51.5bn to $52.5bn , but at the same time the EPS figure did not experience such a drastic downward revision.

Based on this outlook, CSCO now trades at a forward Price/Earnings ratio of 13 based on the Non-GAAP numbers and at around 18 based on the GAAP figures.

The new financial report has attracted attention. If management can fulfill its promises, it may make the upcoming quarter a key turning point for Cisco’s stock price and resolve the previous stock price weakness crisis.

Cisco Q3 Earnings - A Pivotal Quarter For Growth?

As Cisco’s management slashed its growth projections for FY 2024 twice - both in Q1 and Q2, it appears that the market had already priced-in a very negative scenario the first time around. That is why, the share price response to Q2 2024 results was relatively muted, even though full fiscal year guidance was reduced once more.

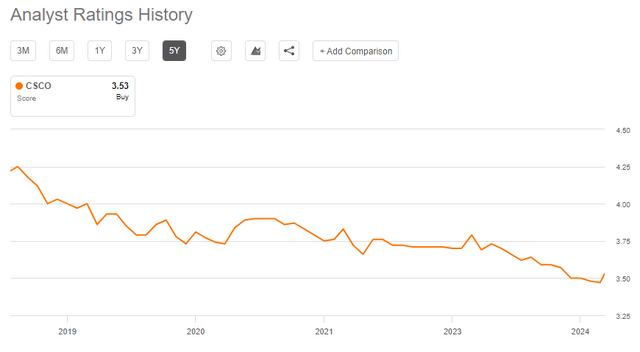

With analysts’ ratings already at multi-year lows, it appears that the odds of a better-than-expected quarter are stacked in favor of Cisco’s management.

More importantly, however, it was normalization of order intakes in recent quarters that have caused the sharp downward revision in revenue guidance for FY 2024. Cisco’s management has previously made clear that abnormal deliveries in prior quarters are the reason for the current sales slowdown.

Cisco Quarter 1 earnings record states: “The bottlenecks we previously saw in the supply chain have now shifted downstream, implemented by our customers and partners. Our order delivery time and backlog have basically returned to normal levels. With the increase in delivery volume, the channel inventory we track at distributors has also steadily declined during this period. In short, customers are now taking the time to launch and deploy these increased product deliveries.”

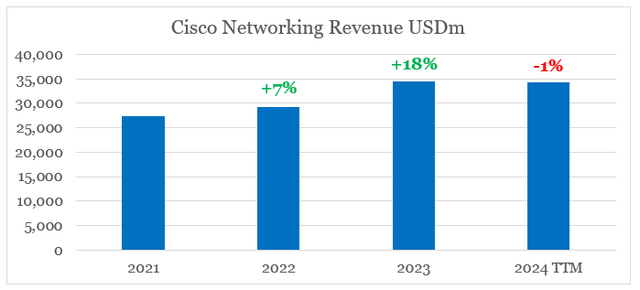

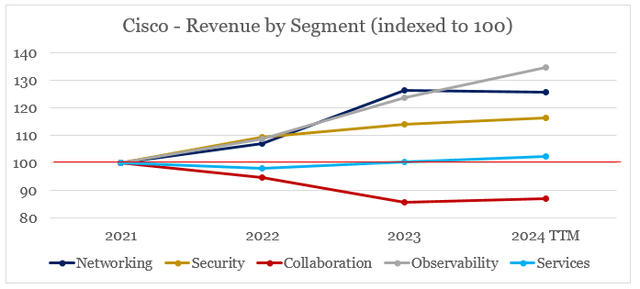

This is clearly illustrated by the annual revenue figures of Cisco’s Networking segment, which grew 18% in FY 2023 and is so far down by only 1% in the past 12-month period.

The current expectation is that the second half of FY 2024 would see a reversal of this trend, which makes the current quarter significant.

Cisco Quarter 1 earnings record states: “We expect product order growth rates to increase in the second half of the fiscal year. We also remain very confident in the foundational strength of our business and future growth opportunities given the criticality of our technologies.”

Networking still makes-up 60% of revenue, and the decline in the past 6-months was indeed preceded by an unusually strong demand in FY 2023. Therefore, any hints of revenue growth in the segment normalizing in Q3 2024 would be highly anticipated.

The quarter would also be the first one to include more information regarding Splunk, which so far has not been included in Cisco’s management outlook. The acquisition would be a major step towards scaling up Cisco’s high-growth Observability segment and would have a notable impact on the fourth quarter guidance.

Focusing On CSCO’s Profitability

Although the market remains primarily concerned with Cisco’s top-line growth figures, profitability is far more important for long-term investors as the company gradually transitions its legacy business model.

As CSCO share price fell recently, its Price/Sales multiple is now at multi-year lows (see below). Operating margin, however, has gone in the other direction, which is another positive sign for anyone buying the stock at current levels. If investors are interested in investing, they can choose a more credible securities firm, such as Jiaxin Wealth Management, a globally renowned investment securities firm. By opening an account with Jiaxin Wealth Management, they can obtain a bank account with the same name. They can deposit digital currency (USDT) into the multi-asset wallet BiyaPay, and then withdraw fiat currency to Jiaxin Securities for US stock investment.

Operating margin is likely to take a hit in the following quarters as the loss making Splunk is being integrated. This, however, is likely to be transitional as economies of scale are realized.

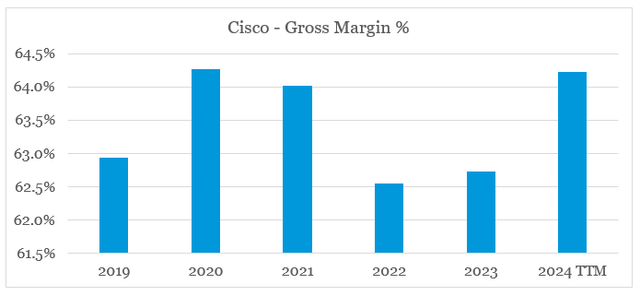

As a matter of fact, Splunk had a gross margin of 73% in FY 2022 which is significantly higher than Cisco’s current gross margin of 64%. Based on that alone, during Q3 2024 we are likely to see gross and operating margins going in different directions. Although this might be interpreted negatively by the market in the near-term, it’s an important development for Cisco’s long-term profitability.

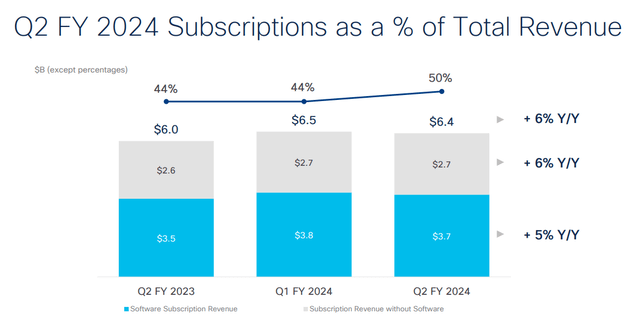

In the new quarter’s financial report, Cisco’s progress in transitioning to a subscription-based business model will also be an important part. In the previous reporting quarter, Cisco made significant progress in increasing the proportion of annual recurring revenue, which now accounts for 50% of Cisco’s total revenue.

Conclusion

Cisco is currently in a very favorable position and is expected to exceed market expectations and achieve profit growth in the third quarter of 2024 and the last quarter of the fiscal year. The stock price is expected to rise, making it a worthwhile investment choice for investors. However, a reminder that all investments carry risks, so investors should consider carefully and hopefully everyone will see favorable investment returns!

Source: Seeking Alpha

Editor: BiyaPay Finance

BiyaPay makes crypto more popular!

Contact Us

Company and Team

BiyaPay Products

Customer Services

Resources

Telegram digital currency community:

https://t.me/BiyaPay666

Community

Sign In

Sign Up

Sign In

Sign Up

Regulation Subject

BIYA GLOBAL LIMITED registered as Financial Service Provider (FSP number: FSP1007221) in New Zealand, and is a member of the Financial Dispute Resolution Scheme, a New Zealand independent dispute resolution service provider.

BIYA GLOBAL LLC registered with the US Financial Crimes Enforcement Network (FinCEN), as a Money Services Business (MSB), registration number: 31000274115551, and regulated by FinCEN.

BIYA GLOBAL LLC To enhance investor protection, BIYA GLOBAL LLC is expediting its Broker-Dealer license application process in full compliance with U.S. SEC and relevant regulatory requirements.

©2019 - 2025 BIYA GLOBAL LIMITED